Yesterday’s RBA rate cut has fired off some better-late-than-never housing hand-wringing:

As the RBA’s move unleashed a political debate about the strength of the economy, UBS analyst Jonathan Mott said record-low mortgage rates meant the “ingredients are now in place for another bout of sustained house price inflation in Australia and Sydney in particular”.

…“Given Aussie housing is already expensive by most metrics we see this as undesirable and dangerous,” he said.

ANZ economist Warren Hogan predicted there would soon be a growing debate about “how much frothiness we’ve got in the property market over the next year or so”.

…“For the first time in this cycle there is now a material chance this is the last rates cut – I haven’t felt confident saying that before,” Mr Hogan said. “And if there’s more . . . there’s trouble on the horizon for Australia’s economy.”om a dependence on resources investment. The Reserve Bank is expected to downgrade its growth forecasts on Friday.

…Kieran Davies, a senior economist at Barclays, said the cut was a clear sign of economic weakness. “But it’s part of the RBA facilitating the adjustment to the end of the boom in mining investment,” he said. “They’d like the currency to play its role as well because it’s a way of getting the stimulus through the economy without putting upward pressure on house prices.”

Economists pointed to other developed economies that have been forced into dragging down their currencies by lowering interest rates, including New Zealand, Canada and Scandinavia, all of which are now experiencing unsettling property price booms.

Those examples “will give the RBA pause for thought because we never had the correction in house prices that other countries experienced, so we’re starting form a point where housing prices are already at very high level,” Mr Davies said.

Sigh. It’s hard to believe we’re back to this but there you have it. The bubble, of course, is not back, it never left. Whether it’s become any more dangerous is a moot point but I’m still skeptical that we are on the verge of a “sustained” round of housing inflation and, whether we are or not, the risk of a major shakeout has never been higher.

Advertisement

Interest rates are at these levels because the mining boom is going bust. It was no ordinary boom and it will be no ordinary bust, running for the next three years, as I explained earlier this week, via falling business investment and terms of trade:

At MB we think that the mining investment downdraft will withdraw 1.5-2% of GDP per year for three years. That will return mining investment to a long run average of about 2% of GDP per annum. This is based upon BREE’s current projects underway forecast plus a little more.

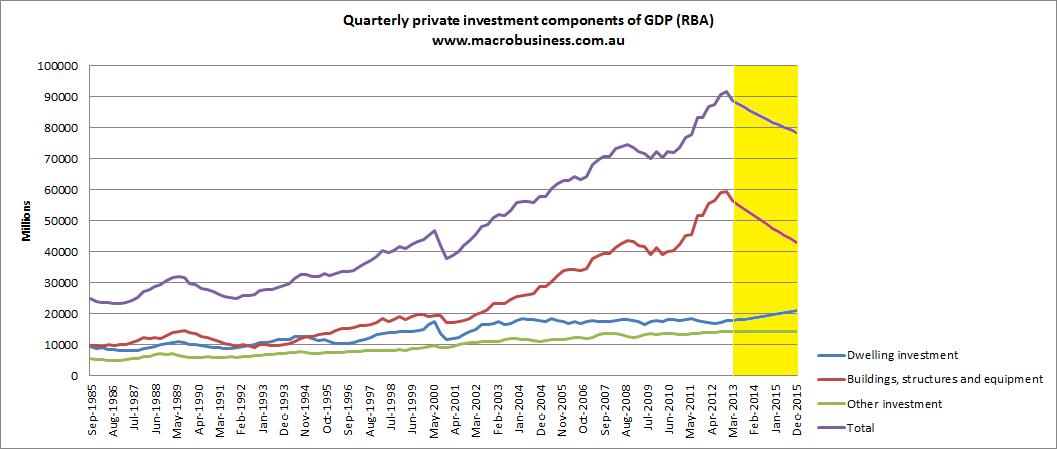

In chart form that looks like this:

I’ve averaged the mining investment decline over twelve quarters (it will likely be much more lumpy) and I’ve continued the dwelling investment recovery at an accelerated pace right through the next three years. I expect broader consumer prudence to persist so I do not expect a turnaround in other private investment until the dollar falls much further and then not for a while either. As such, I’ve added a broader slow business investment recovery from the beginning of 2015.

The top line of total private investment is the one to observe. Note how long and steep it is versus 2008 and 1991. Less precipitous but far longer than in 2000. As well, I would argue we have largely exhausted the house price gains that saved the economy in 2000, have fewer options to boost productivity than we did in 1991, and mining is the problem this time not the solution as it was in 2009. We also have less effective interest rates and less capacity to fiscally stimulate.

That’s not to say the recovery won’t come from somewhere. It will. But in the mean time, as you can see, the mining investment cliff represents a pretty awesome headwind for growth.

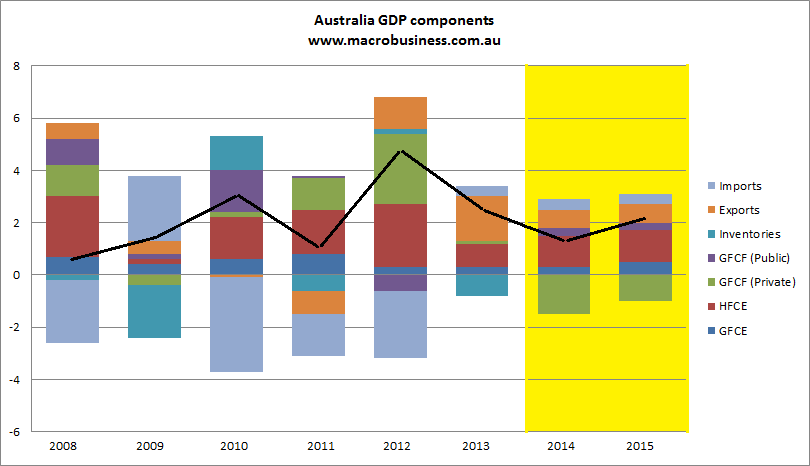

How awesome? Let’s look at it another way. Here are the same speculations charted as percentages of GDP that also includes the offset of growing commodity volumes in net exports:

Note the big subtracting green boxes. That’s private investment with moderate growth in dwelling investment included. It also includes a turnaround in government spending contributing to growth and a modest acceleration in household consumption from this year’s levels. I’ve slowed the contribution from net exports because Chinese demand will flat line this coming year and Indian iron ore volumes will not need to be displaced a second time. The results are GDP growth of 1.4% in 2013/14 and 2.1% in 2014/15.

…The point is it’s an economy operating at stall speed, with rising unemployment and falling business investment. Into this mix we must throw one more probable outcome.

There is a significant risk that the terms of trade will fall further and faster than Treasury forecasts. The iron ore deluge will reach full roar in the first half of next year. Iron ore could very easily spend much of 2014 under $100 and by year end be below $80. Iron ore represents some 25% of the ToT so by itself an $80 price would reduce the ToT by 10%, the same fall Treasury has forecast for the next four years. Coal has further to fall too, in my view, some 10%.

Rising house prices will do nothing to increase jobs or growth (beyond prompting dwelling construction which is already in the above rough figures). Only if households go and spend their equity will that happen. The signs right now are that they won’t and given the post-GFC context is it likely? If not, unemployment keeps trundling higher and contains this latest bout of housing hysteria.

Advertisement

Is it possible I’m wrong? Yep. It’s possible that a renewed round of housing and consumption growing materially above income could slingshot the economy across the mining investment gap. When it lands on the other side in the second half of 2015, and net exports growth accelerates, it will then have to jump another eighteen months to the next round of LNG export takeoff. That is what MUST happen if Australia is to keep growing enough to prevent unemployment from rising.

If this transpires, interest rates are at the bottom, the dollar will not fall past where it is and houses and holes must grow the economy beyond 2017 as we become the single most uncompetitive economy on earth in everything but resources and citizenship. It will require APRA, the RBA and credit rating agencies to ignore renewed offshore borrowing in the banking system and a resumption of growing household leverage ratios. And it will require global markets ignore a growing current account deficit. If the consumer is only half-committed, it will also require ongoing budget deficits. In short, everyone, everywhere will need to ignore everything they’ve learned in the past five years.

You can never say never in macroeconomics but I think it significantly more likely that falling income growth is a brick wall in the way of all of it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.