Since the last rate cut I have heard rumour from a couple of Sydney-based mortgage brokers that demand for loans has tipped from strong into boom conditions. This is slim evidence and we all know that Sydney is a far hotter housing market than any other in Australia right now so I would caution against extrapolating this to the entire country. However it does rather beg the question, what does it mean if the RBA’s slash and burn rates campaign aimed at getting us over the mining investment cliff fires off a renewed specufestor blowoff in housing?

Let me be clear that my base remains that house prices will not do so. Unemployment is going to keep rising. Perth is going to come under increasing pressure, Brisbane is stuck in the mire, Melbourne has dreadful economic and property fundamentals and the small capitals have hardly budged. Only Sydney is ripe for a push higher. Aside from that, APRA still stands in the way of an aggressive mortgage push and it would be completely mad of investors. But, hey, maybe Australia is just that bonkers.

So, if property prices do take off, like 2009/10 say, the only question that matters is what will the RBA do? That question comes down to a few simple calculations. At what point does the boom threaten either inflation or financial stability?

On the first, I have argued previously that the RBA will “look through” any tradable inflation that arises from a falling dollar. It will do so because to hike rates as the mining boom goes bust would be disastrous for the economy. It is a better course to let inflation run above the target band and allow a real depreciation in which wages don’t rise as tradable prices do (assuming this challenge is embraced by the government of the day).

Advertisement

But could the RBA ignore asset inflation? I don’t think so because it will threaten financial stability.

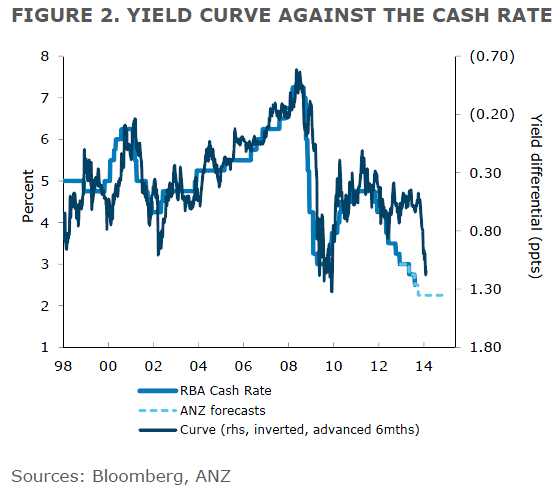

It may be a moot question anyway. Markets may not ignore asset inflation and force the banks to hike by themselves. As the AFR discusses today, Australian bonds appear to decoupling from rate cuts:

…bond yields have still edged higher despite the Reserve Bank cutting the official cash rate to an all-time low of 2.5 per cent.

The yield on the three-year government bond stands at about 2.63 per cent, very high if investors also think there is going to be one more rate cut in the cycle to 2.25 per cent. According to National Australia Bank the yield on the three-year bond can trade anywhere between 80 basis points and 120 basis points over the cash rate before the easing cycle is over and the first rate rise is announced.

…A positive yield curve is normal as the further out you go the risks are greater and interest rates should be higher.

But if the curve keeps steepening then business and mortgage loans will also rise, which won’t help the local economy.

Advertisement

Correct, but this is no ordinary economy. Asset inflation aside, there is no way interest rates should be rising in the medium or long term. The mining investment cliff is three years long, local inflation is at the lower end of the RBA’s range and that includes a half to three quarter point added through a carbon price that’s going to be scrapped. Tradable inflation will be ignored and the dollar remains far too high for the cost structure of the underlying economy. If anything rates should be going lower still.

So what’s with the decoupling? Either markets can’t see the RBA ignoring tradable inflation, can’t see them ignoring asset inflation or something else is going on. ANZ argues the latter:

The main contribution from these results is that they quantify the impact which the US 10-year bond yield has on Australian 10-year yields. It is a widely accepted phenomenon that developed economy bond yields can be priced off US yields and this note shows that this remains true for Australia. Incorporating the results of both of these models, the impact of another 1ppt increase in the US 10-year bond yield on Australia’s bond yield is in the order of 94-120bps (incorporating two stand errors around the point estimates from the results below).

Advertisement

In short the Fed taper is the culprit. Irrespective, the direct implication is higher cost of funds for the banks. The RBA is now fighting the Fed which may slowly choke off Australia’s low mortgage rates via rising wholesale funding costs.

But if not, for house prices to continue to accelerate, I expect credit growth will need to move decisively above 6% growth and probably towards 7% from its current levels of 4.8%. In 2010, mortgage growth rates went above 8% but this was offset by tumbling business credit holding aggregate growth to just 3%. That would not happen this time around.

By my calculations, these levels of credit growth will only be possible if the banks are extending their offshore borrowing at $10-20 billion per annum. So very quickly, perhaps within twelve months, we would have a situation where the underlying economy is struggling to grow as mining investment falls and the Australian dollar has not fallen much further, asset prices are out of control and financial stability is becoming a pressing question.

Advertisement

What does the RBA do? It has explicitly repudiated macroprudential tools and would need a long consultative process to install them so it is questionable it could do much on that front. The government of the day is unlikely to be helpful. The Bank could try the jawbone, in fact it already is, with Stevens warning households again to not increase their leverage in his recent speech. But that hasn’t worked for the RBNZ and does not appear to be working for Sydney-siders either.

In short, amid the greatest run down in Australian business investment anyone can remember and perhaps the most desperate need for a lower dollar in twenty years, the RBA will be forced to stomp on the specufestor outbreak by jacking the cash rate, with disastrous consequences for the economy.

The RBA is taking quite a punt by not insuring this cycle with a move to expand its policy tools.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.