Mac Bank has neat summary of recent gold market trends today:

So what have we learnt about 2Q and what does this data tell us about the outlook for gold? After all that large institutional selling was met by strong jewellery demand or retail investment demand is not that newsworthy – the sold gold has to go somewhere and the gold price falls to make it happen. But we would highlight:

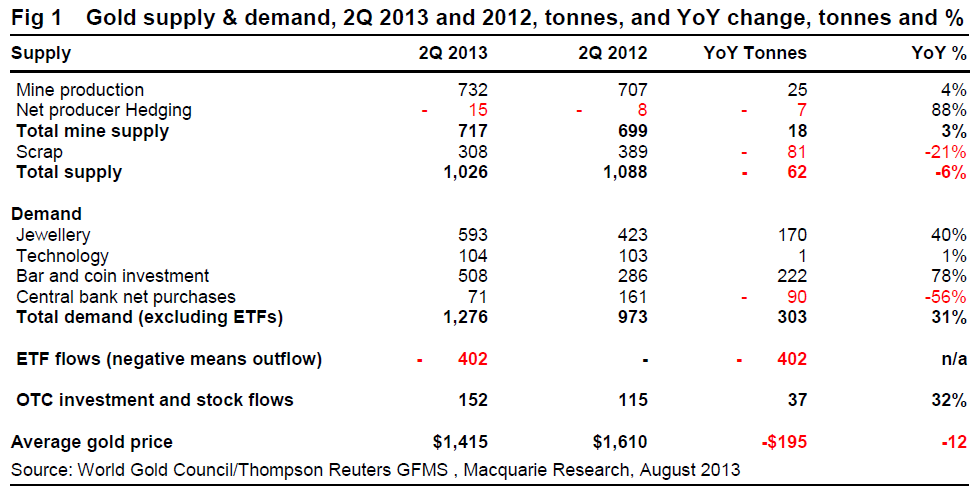

Mine supply continues to increase despite the low price. It was always unlikely that miners would react to the price collapse with cuts in production straight away; indeed some have increased production. However the WGC suggests that mine supply might start to fall from the end of 2013.

Jewellery demand seems very price elastic – a 12% fall in the YoY price saw a 40% increase in fabrication, 37% in consumption. This means the dollar spend on jewellery rose quite substantially. This might overstate the true price elasticity, however, given all gold jewellery has some investment component, and hence the quarterly change in price (a larger 25%) and future price expectations might have been more relevant.

Similarly retail investors in bars and coins appear to have a very different outlook for gold (or a different time horizon) than institutional investors in ETFs. Bar and coin demand rose 78%, ETFs saw outflows of over 400t. One explanation might be different local conditions (such as inflation or interest rates) means gold investment looks a better bet in some countries and currencies than it does for dollar-based investors (although US bar and coin investment doubled).

Central banks appear to have reacted negatively to the price fall, reducing purchase substantially. These transactions are lumpy and it is hard to draw conclusions from one quarter‟s data – but the WGC did reduce its forecast for full year purchases to 300-350t, down from an earlier forecast of 400t and an estimate of well over 500t in 2012.

The gold market is increasingly reliant on India and China. Together those countries accounted for 68% of the increase in jewellery and bar and coin demand YoY, and their share of demand rose from 46% of the world in 2Q 2012 to 54% in 2Q 2013. With the Indian government‟s efforts to reduce consumption only beginning to take effect in 2Q this must be a concern going forward.

Price outlook is still very much dependent on ETF flows. Given this it is a positive sign that the GLD ETF, responsible for 63% of the 671t of outflows seen in the first seven months of 2013, has seen consecutive inflows of metal in the last week (on 9 August and 14 August), the first time this has happened since December 2012.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.