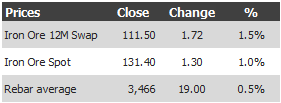

Find below the iron ore price table for July 6, 2013:

Another good day fired up by a solid jump in rebar. The miracle commodity continues on its merry way, ignoring rebar weakness then climbing on strength. I still say down from here but another day of up and we’ll have a new high for the move, setting the traders loose.

Meanwhile, from CBA, which seems to be a media outlet now, the little miners are talking it up:

Mid-tier iron ore miners have used an industry event in Kalgoorlie to talk up current margins, adding that new supply may be lower than expected, which would be good news for the price of the steel-making commodity.

Atlas Iron (AGO) managing director, Ken Brinsden, told the annual Diggers & Dealers forum that the company’s all-in cash cost for the 2013 financial year was $75 per tonne delivered to China, while the current realised price in Australian dollar terms is $120 per tonne giving a “very, very healthy margin”.

In this context the company said it “makes sense” to continue to look toward Pilbara resources.

“Today’s margins are amazing,” Brinsden said. “There’s a lot of people down in the dumps but we actually consider ourselves pretty lucky. It’s an amazing business and we are growing our cash flows – we are still expanding.”

Atlas is currently producing at 10 million tonnes per annum (mtpa), up from 6mtpa six months ago and is due to reach 12mtpa by the end of the current financial year.

…Speaking at the same event, Mount Gibson Iron (MGX) chief, Jim Beyer, put the company’s all-in cash costs for the year in the “mid $70s” and described margins as “very strong”.

Miners speaking at the event have been united in their opinion that analysts may be over-estimating new supply due to come onto the market, which has been an element in some of the more bearish forecasts on the iron ore price.

“There are challenges sitting on the supply side. I think at best it’s naïve to line up all the iron ore projects believed to be out there, put them on a spread sheet and believe they’re all going to come online, on time without an issue. That just has never happened.

“I think the reality is we need to be clear that the supply side is not going to run as smoothly as planned … as some sectors of reporting and analysts suggest,” Beyer said.

In summary, for the little guys it’s all fat margins and expanding volumes. Yet, for the big guys, it’s all supply-side delays and over-estimation. Of course it is!