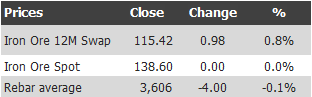

Find below the iron ore price table for August 26, 2013:

India’s leading business newspaper, Business Standard, today launches a stinging editorial aimed at resuming iron ore exports:

Domestic users of iron ore, like the steel industry – and, further downstream, the engineering industries – are seeking to dissuade the government from lowering the export duty on iron ore from 30 per cent to 20 per cent, one of the moves the government is considering to improve export performance and curb imports so as to rein in the runaway current account deficit. At a time when volatile global currency flows have induced the beginnings of a possible crisis in emerging economies, from Brazil to Indonesia, and have severely beaten down their currencies, it is important that such measures be seriously considered to mitigate the effects of crisis fears.

However, the arguments being trotted out against the decision by the user industries are hardly novel. They have over the years sought to restrain iron ore exports so that the steel industry can access a key raw material cheaply, and also share a part of the benefit from this with steel users. It is certainly true that an economic system that exports low-value-added iron ore and imports high-value-added steel is a recipe for disaster and continued economic stagnation. However, India’s steel industry should also answer what, in all the years since steel prices were decontrolled, has prevented it from becoming a powerful exporter? After all, many other countries with access to less domestic iron ore than what is available in India have managed to create powerhouse steel industries that export across the world. Why did that not happen in India? That Heavy Industries Minister Praful Patel has added his voice to the demand not to lower export duty is, frankly, poor timing on his part.

Severe restrictions that the Supreme Court placed on iron ore mining in Karnataka, Odisha and Goa cut exports sharply and were instrumental in creating current account worries. The Supreme Court intervened because regulation was lax. Besides, outdated mining methods were playing havoc with the environment and public health in the mining areas. Certainly, introducing transparent regulation and tightening the environment impact requirements for iron ore mining are essential steps forward – but they must be accompanied by efforts to repair the current account. The Union government should approach the Supreme Court and request it to ensure that the central empowered committee, entrusted with systematically reallowing mining to resume in an orderly way by following proper rules and safeguards, speeds up its work. The Supreme Court should be requested to send a message to the committee that there is a crisis at hand and so it should finish its task expeditiously.

It is urgently necessary to remove restrictions on mining where possible (except, of course, leaving out operations that are almost wholly illegal or harmful) and ease the path of exports – if Chinese steel manufacturing does indeed pick up, as some expect, global iron ore prices will rise. Restoring export volumes, which fell from 117 million tonnes in 2009-10 to a mere 18 million tonnes in 2012-13, is essential to stave off fear of an external account crisis that many in India fear is looming.

The logic is irresistible.