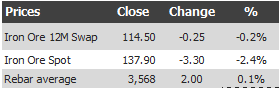

Find below the iron ore price table for August 16, 2103:

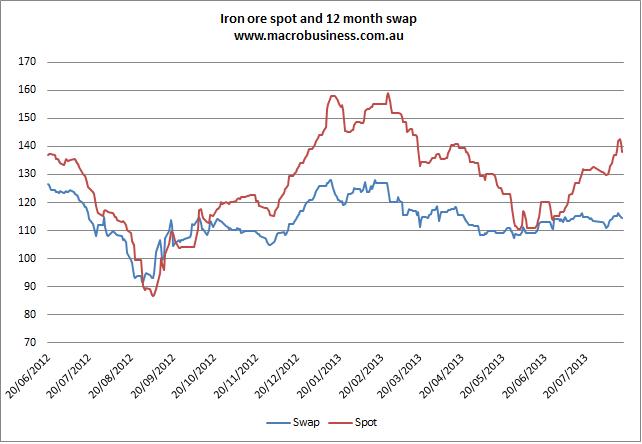

Rebar futures fell. Looks like the rally is done. Here are the charts, spot and swap:

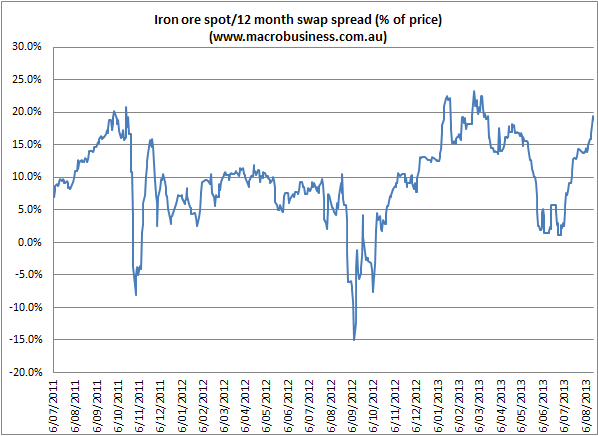

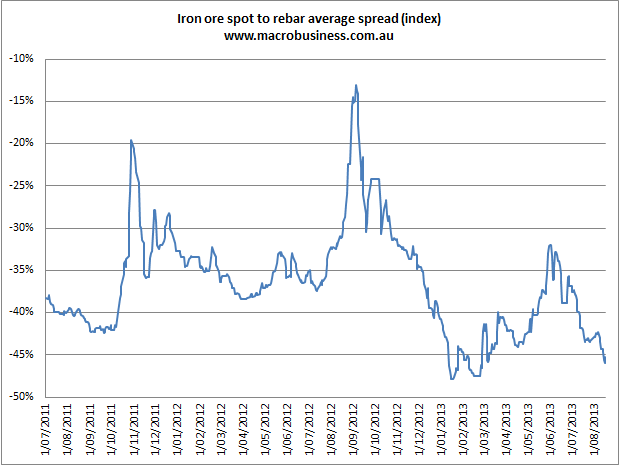

With a now ugly and vulnerable looking spread:

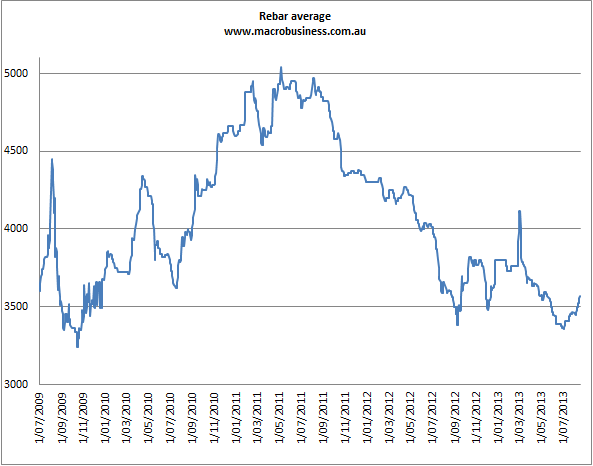

There’s 10% potential downside for spot in this chart alone. Meanwhile, the rebar appears to be running out of steam for now but certainly has more room topside:

The spread to iron ore spot is now epic once more and also vulnerable:

Whether it’s the next few weeks or longer term these charts are going to revert from here.

Meanwhile, in news, the FMG/Formosa deal has led to an MSM flourishing for Andrew Forrest over the weekend. Even FMG skeptics such as Mathew Stevens at the AFR were fulsome with praise:

Somehow, Team Fortescue has been able to monetise an asset that very few in the market valued at more than zero and, simultaneously, secure foundation investment and custom for a project that was categorised, most justifiably, as very distant blue sky.

Given it all goes to the running sheet Fortescue promoted on Friday, this is a deal that ticks every box imaginable, from the discretely financial to the regionally tectonic and the immediately political.

…Formosa will also pay $US500 million to Fortescue so that the project can export through Fortescue’s Herb Elliott port. For good measure, that cash will be paid up-front on completion of the deal, which will be triggered by foreign investment approvals here and in Taiwan. Those are expected by September’s end.

Needless to say, that is an awful lot of money to pay to ship 1.5 million tonnes of product. Fortescue agrees. It reckons the $US500 million should better be understood as part of the price tag rather than project investment. Which effectively means that Formosa has paid $623 million for its share of the project. And that implies a value of something like $US1.9 billion on the joint venture.

…The plan, as it stands, is that the JV will start pumping out a beneficiated 66 per cent product sometime in 2015. All things being equal, it would then seem a fair bet that the customer for that iron ore will be Formosa. Which means this deal marks the first geographic diversification of Fortescue’s customer base away from China.

…This is where things get interesting at a tectonic level. Its 22 million tonnes a year (mtpa) monster is being built at Ha Tinh in northern Vietnam and Formosa has signed up to feed it with up to 3mtpa of Iron Bridge product.

A few points. This is not tectonic for iron ore unless it adds to net demand and there is no saying it will given the over-production already apparent in China which will be exported. Second, this deal is tiny. $1 billion to produce 11 mpta. While FMG is clearly going to look to sell more stakes in it, it may as well have to contribute more capital. Most importantly, the iron ore market is going to reject new tonnage in 2015 unless it’s very low cost which iron bridge has never been represented as. Perhaps this is why Goldman Sachs rates the new deal at a value of zero.

FMG may have its challenges but not among them is quality salesmanship.