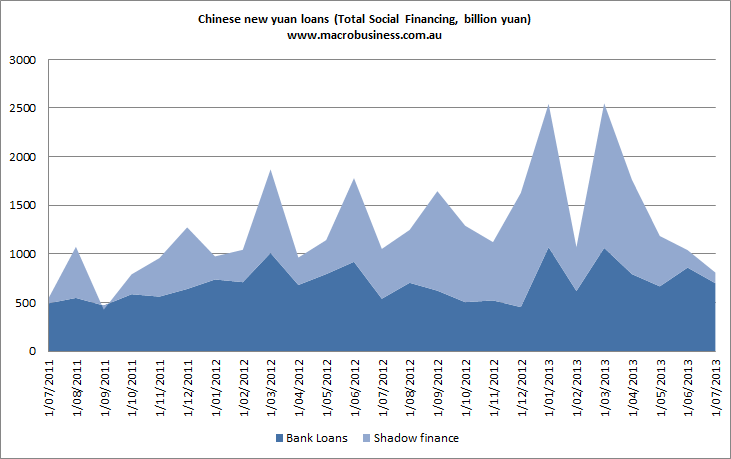

Last week illustrated some better numbers in China with the promise of a bottom in activity in the PMI and industrial production. However, over the weekend China’s July credit numbers were released and cast doubt over the longevity of the bounce, such as it is. Total social financing (banks and non banks) took another big hit, falling to its lowest level in almost two years at 808.8 billion yuan:

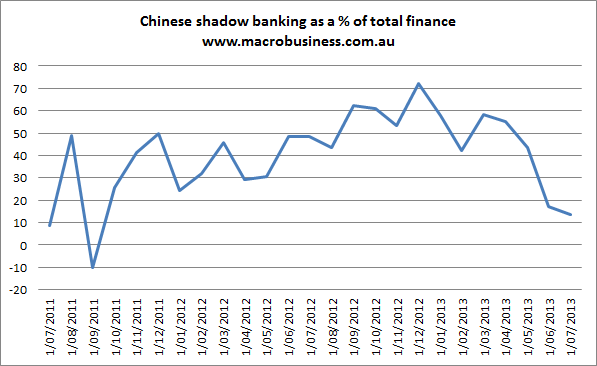

Bank loans held up but the shadow system was squeezed hard and only produced 14% of total credit, well past its prime following the credit squeezes of the past few months:

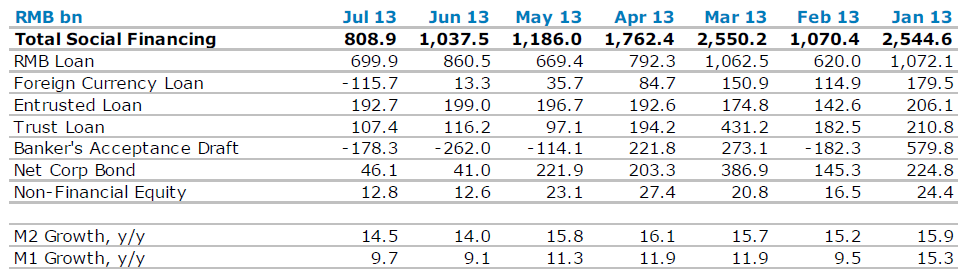

ANZ offers a breakdown of the shadow system falls:

It added:

The drop likely reflects that onshore banks have cut their foreign position or trade-related (arbitrage) activities in July. Chinese corporates that look for foreign currency loans may have been pushed to the offshore markets such as Hong Kong. The situation will not be relieved until onshore banks have recovered their foreign currency positions.

Fair enough but look at some of the other real economy items. Trust loans down 75% and corporate bonds down 90% from March levels.

While this is welcome in terms of heading off any future financial crisis, the risk is that growth will slow as we head into Q4 and next year. You might ask why that’s the case if the the big surge in shadow credit over the past twelve months didn’t add to growth?

The answer lies in the theory that China has reached some kind of Minsky moment in which much of its new credit issuance is being dedicated to funding older loans so that its credit multipliers have ceased working. If that proves true, when the firms that are reliant upon shadow financing to stay afloat – ponzi borrowers – begin to go bust, then the ripple effects will slow activity in the real economy anew as well as clogging the banking system with bad loans.

Since its credit crunch began, China has had two months of heavy falls in shadow lending and total social financing is now firmly in the range of the second half of 2011 when hard landing concerns were at their peak.

So, given wider improving data flow, is it boom or gloom? Reuters had a scoop on Friday that may offer a clue:

(Reuters) – China is developing a new trading platform to enable banks to sell off loans to a wider range of investors, in a move that could pave the way for a government bailout of lenders or distressed asset sales to private investors.

The trading platform, now in the testing phase, is designed to introduce banks to a new class of investors, including non-bank financial institutions and large companies.

Currently, the lack of well-established precedents for asset disposals effectively leaves banks only two options: sell non-performing loans in private deals, mostly with big state-backed asset management firms, or keep rolling them over indefinitely to avoid booking a loss.

Most analysts believe Beijing will eventually be forced to use some public funds to help peel off bad loans from state banks, but the ability to draw in at least some private capital could reduce the cost of that bailout. The new platform could aid the effort to draw in private investors by allowing for price discovery for loan transfers, creating benchmarks that could guide future deals. Greater transparency in pricing could thus lure even more investors.

So, China appears to preparing new mechanisms to shift non-performing loans from bank balance sheets and free them up to support the economy with fresh credit. FTAlphaville goes on to quote Simon Hunt, of Simon Hunt Strategic Services:

The speed with which government has acted in the wake of July’s credit repercussions is not just exemplary but illustrates how deep and serious is the debt issue especially in the private sector which has been the major driver of growth and employment.

The real question, of course, is who will be the buyer for the distressed loans. One favourite will be the four AMCs established in 1999 to take-over some of the banks’ non-performing loans. Government would like the private sector to participate but for that to take place they would need significant discounts to face value.

We will keep you abreast of new information as and when it is forthcoming. However, all the initiatives that government has introduced point towards a stronger recovery to the economy that we thought possible just a few weeks ago. It fits what we have also been saying that starting sometime this autumn exponential rises will be seen in global equity and commodity markets that should last for only 6-9 months after which serious declines will be experienced.

Given the potential scale of the problem I find it difficult to believe that this process can proceed without a hiccup. But it is China, which specialises in the extraordinary, and you can’t fault the forward-looking nature of this policy-making.