Cross-posted from Kate Mackenzie at FTAlphaville.

As we noted a week ago, there was some recent anxiety that Chinese interbank markets were again freezing up, with Shibor rates jumping again as the end of month neared.

A couple of days later, several reports emerged that the People’s Bank of China was coming to the rescue by conducting reverse-repo operations for the first time since February, injecting a net Rmb17bn.

Then Chinascope Financial wrote on Tuesday that a pile of PBoC bills were due to mature during that week – they put the value at Rmb85bn — which would, if the PBoC allowed it to, constitute a net injection of liquidity.

Only, it seems like that didn’t happen:

According to the Oriental Morning News today, the People’s Bank of China (PBoC) “re-issued” RMB184bn of three-year central bank bills in July. These bills were supposed to expire in July, but instead of letting them expire and issuing new bills, the PBoC “re-issued” these bills to large financial institutions that had “good liquidity and strong market influence” (quote from the Q2 monetary policy report issued on 2 August). This is the first time the PBoC has conducted a “re-issuance” operation.

That’s Nomura’s Zhiwei Zhang.

So what gives? The PBoC has had a track record of changing its favoured tools, especially over the past few years. Some of these moves — such as the decision in January to introduce regular short-term repo and reverse-repo operations — appeared to be part of a shift towards more market-based and transparent liquidity management, and away from relying on reserve ratios and lending and deposit rates.

This latest move… not so much. Nomura again (our emphasis):

We think the major difference between this operation and standard open market operations is the disclosure of this operation by the PBoC did not have to be timely. The market mistakenly believed that the PBoC injected liquidity in July by letting central bank bills expire and through open market operations, which led to an overall net liquidity injection of RMB291bn. But if we properly include this covert “reissuance” of central bank bills, the net injection would total only RMB107bn. This partly explains why the 7-day repo rate shot up to above 5% in late July, and remains elevated at 4.5% today.

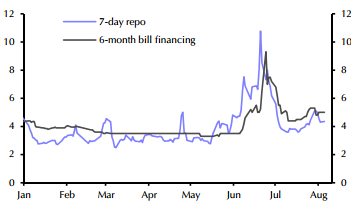

That last point, rates remaining relatively high, is illustrated this chart from Capital Economics:

Zhang has been saying for some time that the PBoC does not seem willing to ease, a view which he says was compounded by the PBoC’s Q2 monetary policy report published last week:

The top priorities for the PBoC changed from “stabilizing growth, containing inflation, managing risks” in the Q1 report to “stabilizing growth, rebalancing the economy, promoting reforms, and managing risks”.

Meanwhile, PBoC data released last week showing that in June, interbank market lending fell a total 60.2 per cent year-on-year, and almost the same amount month-on-month.