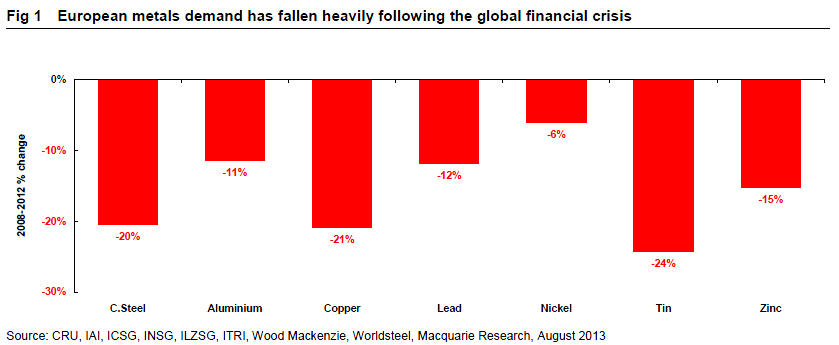

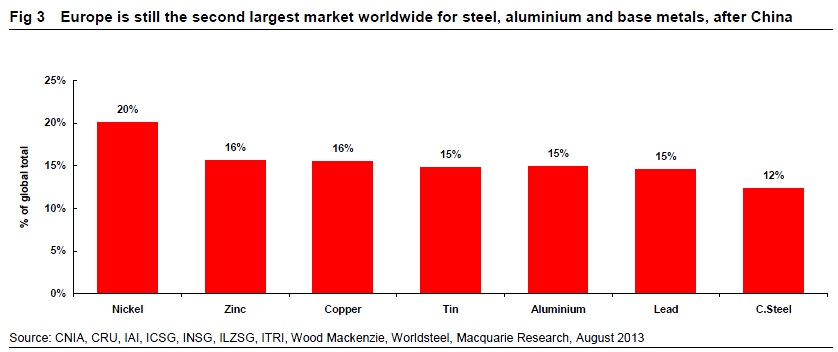

Discussion of European economic data has made for a mainly dismal dialogue in recent years. Lately, however, glimmers of hope have been gleaned on the horizon and this appears to have been the trigger for questions asking how European recovery – or at least an end to the downturn – might affect global metals market balances. Europe is the world‘s second largest consumer of most metals, after China, and taking account also of imports of manufactured goods, it is even more important in metals markets than it might appear at first glance. Europe has clearly been a drag on global metals demand in recent years and the size of the market is such that even modest swings in the rate of change in European demand can be significant relative to the size of global metals market imbalances.

In the case of lead and tin, already finely balanced markets, the average tonnage lost to declining demand in Europe over the last four years is more than any surplus expected in the global market next year. In the case of carbon steel, the numbers are approximately equal – in other words, the forecast surplus in the global steel market next year is much the same as the average decline in European demand over the last four years. In the case of aluminium, copper and zinc, the average tonnage lost to declining demand in Europe is equal to over one-third of forecast global surpluses in 2014.

This looks a bit like ‘glass half full’ analysis to me, at least in the case of steel. The EU is on track to produce about 160 million tonnes of steel this year, versus Asia’s one billion tonnes. China alone massively over-produces, driving down and is forcing more and more into export markets. It will take a very strong recovery to cause any kind of tightness in the global steel market. As well, it is likely that a considerable amount of fallen EU production is lost market share to China.

That said, obviously any European recovery is welcome and will have some marginal impact.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.