If there is one component of my iron ore forecasts I’ve gotten wrong in the past year it is that Chinese steel production was near a peak in 2012. So far this year, Chinese steel output growth is pouring it on. Morgan Stanley today breaks it down:

From an industrial commodities perspective, China’s July datapack surprised to the upside.

Trade data, FAI stabilized: Industrial production beatmarket expectations, rising to +9.7% YoY (vs. +8.9% in June). FAI growth held steady at +20.1% YoY (vs.+19.3% in June). Total export growth surprised, rising to +5.1% YoY (vs. -3.1% YoY in June). Meanwhile, total import growth rebounded to +10.9% YoY (vs. -0.7% YoY in June). As a result, the trade surplus narrowed to US$17.8 bn from US$27.1 bn in June.

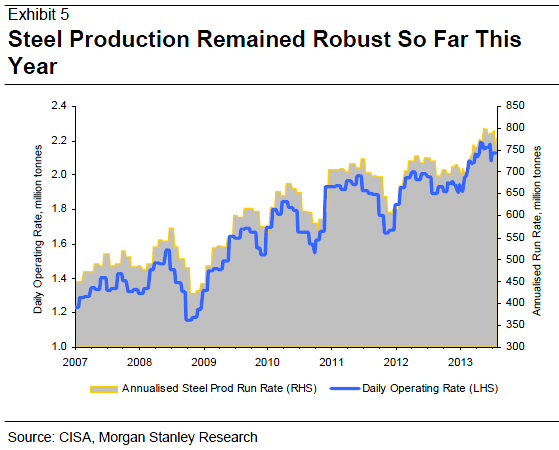

Steel: Production growth continued to accelerate, with crude steel output currently annualizing about 780Mt. This compares to the 2012 total of 709Mt and our 2013 forecast of 741Mt. Meanwhile, finished steel exports for July grew sharply vs the previous two months bringing the YTD net export figure to 27.8Mt, +19%. As a result, despite increasing exports, the combination of strong steel production and continued inventory destocking indicates apparent consumption growth is robust.

It sure is robust at 9-10% (and well ahead of my own forecasts of 2-3%) but there is one giveaway that some of this is excess production. That’s the price of steel products in China, which simply cannot get off the canvass. I still expect the seasonal drop to occur (you can see how reliable it is in the chart) so the final result for Chinese steel production will probably ease below 780 million tonnes (but still very strong).

Not surprisingly, iron ore has benefited from this steel output growth:

Advertisement

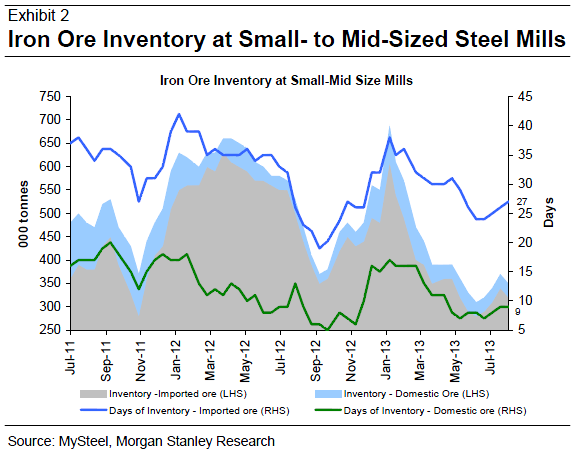

Iron Ore: Given the elevated steel production during July, imports of iron ore were unsurprisingly strong, posting a fresh all-time monthly record. In our view, high imports are not a function of stockpiling, nor does the available data suggest this (Exhibit 2). YTD import growth of 8% essentially tracks that of steel production growth over the period. Although we do expect steel production to moderate in the coming months amid the seasonal slowdown, we believe iron ore prices will continue to average US$125/t for the rest of the year, as the seaborne supply/demand balance remains tight.

That’s probably right. With the big iron ore port stockpile run down, and relatively low inventories at mills despite the recent restocking pulse, what we have now appears to be a market equilibrium. The more plentiful supply of iron ore, and the prospect of much more of it, is enough to convince iron ore hoarders and mills to run lower inventories for good. With oversupply and tight margins defining the market context and prospective slowing demand defining the economic context, why spend dough on forward purchases?

I still expect 0-3% growth for steel next year as China undergoes its growth shift and slowly succeeds in bringing over-production to heal. But it looks to me like iron ore is becoming a “real time” delivery market with fewer and less dramatic inventory swings and, as such, a steady drop in prices, rather than sudden collapse, looks more likely for next year as the great ore deluge flows.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.