Mac Bank has an interesting not out this morning that helps explain the current unseasonable strength in iron ore prices.

Growth may temporarily stabilize…

After a slump of growth for a few months, July may have seen some signs of stabilization. The official PMI came in at 50.3, up slightly from 50.1 in June, and the pick-up was against the seasonality of a drop from June to July. Admittedly, the HSBC/Markit PMI fell again (to 47.7 from 48.2 in June), but the divergence of two PMIs is at least better than if both had fallen again.

Another sign is the stabilization of industrial product prices in recent weeks – our Ministry of Commerce Producer Goods price index has been hovering around 136 since the end of June, ending a downtrend for 4-5 months (Fig 1). With the MoC price index being a very good predictor of PPI inflation, it seems PPI inflation could rise noticeably in July (to perhaps -2% from -2.7% in June).

The stabilization though isn‟t really surprising to us. As we illustrated with the simple extrapolation in Macro Monday – A thought experiment, given a stable base in 3Q12, as long as sequential growth stops falling, the YoY growth of Industrial Production would come out flat in this quarter (although this may not prevent YoY GDP growth from falling further). However, beyond this 2-3 month period, even if the sequential momentum is maintained, a high base in 4Q12 would again pull down YoY growth figures in 4Q13.

… due to decent construction activity…

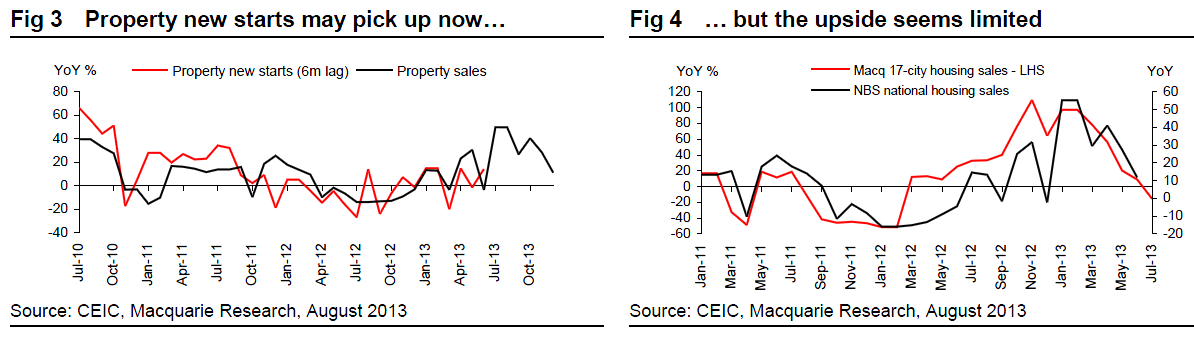

In order to have a better growth projection into the future, we still need to understand the reasons for the stabilization and assess their sustainability. In our opinion, a major factor at play may be decent property construction activity in July. As the growth of new starts lags behind sales growth for about 6 months, the sharp rise of sales growth at the beginning of this year suggests stronger construction activities should be coming around this moment.

To verify this idea though, we‟ll have to wait for the NBS construction figures to come out this Friday. The growth of excavator sales in July is another data point to substantiate (or falsify) the pick-up of property construction (after rising for two months in April-May, excavator sales growth again contracted in June).

As property sales growth started to come down in March-April, the potential strength of construction activity could begin to wane into 4Q13. This thus fits well with our assumption that YoY growth figures may soften again in 4Q13.

In the meantime, as captured by the daily sales of our 17-city sample, the base for YoY growth of property sales will be gradually raised in 2H13 as the housing market has steadily warmed up through 2H12; meanwhile, the sequential momentum of sales seems to have stopped improving at the moment (Fig 5). As a result, the YoY growth of sales in our 17-city sample fell below zero in July, indicating the NBS national sales growth would probably drop too (Fig 4). Therefore, the potential weakening of construction activities in 4Q13 may last into early 2014.

…and possibly less sharp destocking…

Another message that we could read from the stabilizing prices of industrial products is that destocking may be slowing down. Indeed, this seems the case for steel, according to our steel analyst Graeme Train. It‟s hard to quantify this point across all industries, due to a lack of good overall inventory data; moreover, the Materials Inventory and Finished

Goods Inventory under the official PMI remained weak in July.

So, the most we can say for now is if destocking does lessen in 3Q13, that would be another positive factor for growth. However, even if this turns out true, we are not sure that restocking would begin visibly in 4Q13 – companies don‟t add inventories purely for the sake of restocking; without an improved economic outlook, restocking is unlikely to be very strong. This is also why we don‟t tend to pay too much attention to the so-called inventory cycle.

… and faster investment in government projects

In the meantime, the government also seems to be pushing some investment projects. A State Council meeting held on July 31st identified 6 areas of urban infrastructures to be improved, including sewage systems, urban railways, and central heating system. The railway FAI target for 2013 was also reportedly raised to Rmb690bn from previously Rmb650bn, compared with the completion of Rmb606bn last year, and the number of railway projects to be started this year went up to 47 from 38.

There are though two uncertainties about the impacts of these initiatives. The first is the scale and the timing of the impacts. For example, after the railway FAI target was raised, the completion ratio of 1H13 was still slightly higher than that of 1H12 (26% vs. 24.2%), suggesting the YoY growth of railway FAI could still come down in 2H13. It‟s also not clear when these projects could be implemented and we may have to wait until 4Q13 to see the impacts come through. There‟s thus the risk that the newly-added projects are neither impactful nor timely enough to set growth on an uptrend.

Secondly, for these projects to be really started, bigger funding support is necessary and constraints on local government financing have to be alleviated. The picture though is blurred in this aspect. For instance, there seems to be a sincere attempt by Beijing to control local government debt, as reflected in the new round of auditing on local debt, but this may run against the need for local governments to provide money for some railway projects.

… but the monetary policy may not be accommodative enough

Meanwhile, interest rates can‟t be too high for these projects. So, a relatively loose monetary policy is also required. In our opinion, the major barrier here isn‟t the ideological opposition against liquidity loosening, but is that the central bank may fall behind-the-curve on offsetting the weakening forex inflows (we‟ve repeatedly highlighted this issue in recent weeks).

Therefore, the two reverse repos (one for 1 week and the other for 14 days) the PBC did last week were encouraging (as we believed the PBC should be doing), with total Rmb51bn offered to banks. However, that the reverse repo rates were as high as 4.4-4.5% (compared with 1w SHIBOR at 3.5-3.6%) suggests the central bank is still not that ready to loosen. And the impact on the real economy was already somewhat seen – it was reported new loans might come in at less than Rmb700bn in July, down significantly from Rmb861bn in June.

The PBC‟s hesitation appears reasonable given its concern over potential inflation pressure – in its 2Q monetary policy report, the monetary authority again pledged to stabilize inflation expectations. A potential stabilization of growth in 3Q13 could further add validity to this view. However, the structural downtrend of growth that we are worried about may prove that the central bank‟s concern over inflation is overdone in a longer timeframe.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.