FMG gets a break today with an S&P upgrade to stable:

Standard & Poor’s Ratings Services said today that it had revised the outlook on its ‘BB-‘ long-term rating on Australia-based mining company Fortescue Metals Group Ltd. to stable from negative. At the same time, we affirmed the ’BB-‘ corporate credit rating, ‘BB+’ senior secured debt rating, and ‘B+’ senior unsecured debt ratings. The recovery rating on the senior secured debt rating is affirmed at ‘1’ and senior unsecured debt ‘5’.

“The outlook revision reflects our expectation that Fortescue’s credit metrics (which are weak in the year ended June 30, 2013) will recover to levels commensurate with the ‘BB-‘ level in fiscal 2014,” Standard & Poor’s credit analyst May Zhong said. “This view is based on Fortescue’s improving production volume, reducing cash production costs, and expected low capital expenditure in fiscal 2014.”

Under our base-case assumption of US$110 per tonne for benchmark iron ore prices (cost and freight [CFR] 62% Fe), we expect Fortescue’s adjusted funds from operations (FFO) to be more than 20% and adjusted debt to EBITDA to be less than 4x in fiscal 2014. We also expect Fortescue’s volume of ore shipped to be higher than 100mt in fiscal 2014. Fortescue’s total shipments in fiscal 2013 were 80.9mt. In June 2013 alone, the company recorded a 120 million tonnes per annum (mtpa) shipping run rate.

We believe Fortescue is on track to complete its 155mtpa expansion and will continue to increase its production in 2014. The company’s reducing cash production costs also contribute to our expectation of a recovery in its financial performance. Fortescue reported a C1 cash cost of US$36.01 per wet metric tonne (wmt) in the June 2013 quarter, reflecting a permanent reduction in strip ratios, benefits from cost reduction initiatives, and a depreciating Australian dollar against the U.S. dollar. The company expects its C1 cost to be US$36-US$38 per wmt in fiscal 2014, assuming a foreign exchange rate of 0.95 Australian dollar to the U.S. dollar.

Our base case doesn’t factor in the potential sale of The Pilbara Infrastructure Pty Ltd. (TPI), which was announced by the company in December 2012. Should the transaction occur, we would need to review the terms and conditions of the transaction and its implication on Fortescue’s cash production costs and capital structure to assess the likely impact on the company’s overall credit quality.

We would consider raising the rating if:

• Fortescue successfully completes its 155mtpa expansion and develops an operational track record of shipping above a 120mtpa wmt run rate;

• FFO/debt sustains at about 25% and debt/EBITDA at about 3.0x, and the company generates positive free operating cash flows after capital expenditure; and

• The company maintains a disciplined approach toward capital management, dividend payments, and funding for expansion. The company’s growth aspiration and financial policy post the 155mtpa expansion will be key to any rating upside potential.Ms. Zhong added: “Downward rating pressure could be precipitated by a significant weakening in iron ore prices along with a major delay in production ramp-up, causing the company’s FFO-to-debt ratio to fall to less than 20%, and debt-to-EBITDA to go higher than 4x for a prolonged period. If the company’s growth aspirations or capital management were more aggressive than currently expected, it could also exert negative pressure on the rating.

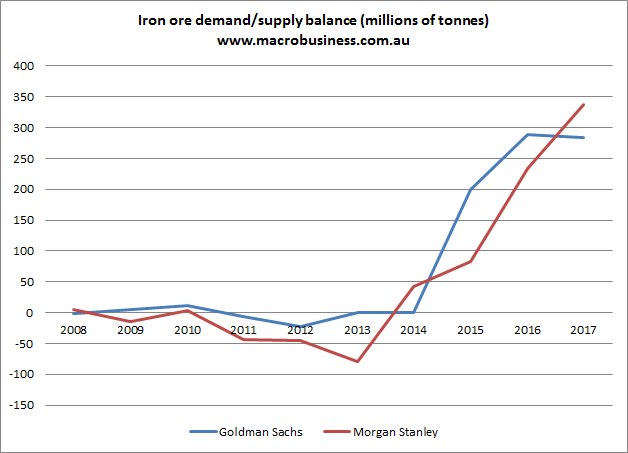

This is fair enough on the assumptions cited. The problem is if you look another few months past FY14 all you can see is supply. I’ve added Gina’s Vanity Hill to GS and MS forecasts and come up with this:

And all of it cheaper than FMG. But for now it’s all good!