Plenty of headlines around this morning after Moody’s declared the obvious: that Australian banks will get hit if house prices fall. This was Moody’s Analytics, BTW, a separate division to the credit ratings agency. Actually, the report was pretty sensible. It was more sanguine about Australian growth than I am but picked up all the right dynamics and foreshadowed a correction ahead for house prices. The money quote is below.

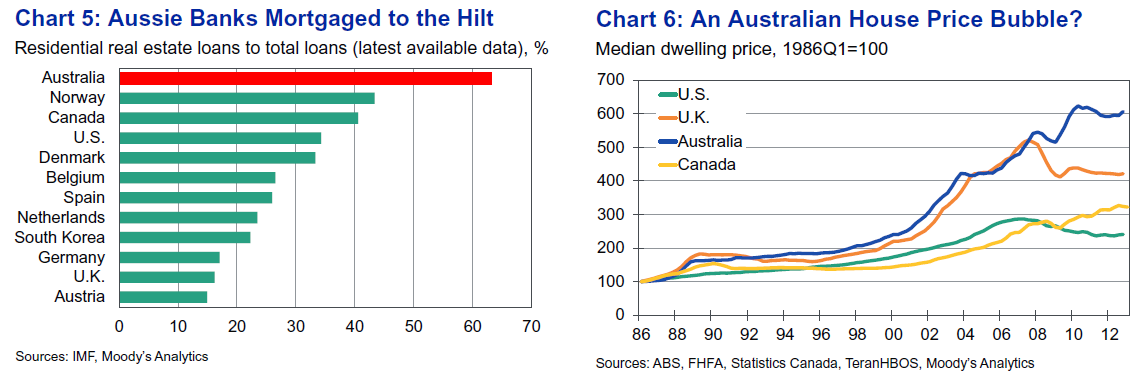

The continued strong expansion in real estate loans—at least relative to other lending segments—has raised some eyebrows. The Australian banking sector has the highest exposure to residential mortgages in the world, according to the International Monetary Fund (see Chart 5). With the absence of any publicly supported securitization market—such as that provided by Fannie Mae and Freddie Mac in the U.S.—and a currently weak private securitization market, any new mortgage originations have to stay on banks’ books. This trend has been exacerbated by recent changes to RBA rules in that the central bank will accept residential mortgage-backed securities, which may be internally securitized (that is, the loans may be securitized by the originating institution and held in their entirety by the same institution on their books), as collateral for loans.

The high degree of exposure to the domestic mortgage market raises many concerns. Recent experience has shown that house prices can fall significantly and trigger serious banking meltdowns. But what are the chances of a similar housing collapse in Australia? Many international analysts think the chances of an antipodean housing bust are quite high—it would take a bold economist who has been in a decade-long coma to declare that an Australian housing correction was impossible. When trends in Australian house prices are compared globally, the signs look worrying. House prices have increased for longer and faster than in many of the markets where prices cratered during the Great Recession.

Local analysts tend to be somewhat more sanguine. The “Lucky Country” has proven to be remarkably adept at sidestepping tackles over the past quarter-century. Moreover, many have argued that local tax rules that favor housing over other forms of investment tend to support more rapid house price growth than in other countries. Others suggest that city planning rules and poor transport infrastructure also are contributors to the elevated house prices in Australia. The problem with these arguments is that U.S. tax laws are more favorable to housing than Australian tax laws, yet house prices still crumbled stateside. Arguments about poor transport, natural barriers to city expansion, and troublesome local bureaucrats apply as much to Phoenix and New York as they do to Melbourne and Brisbane. Though price growth has exceeded international norms for a number of decades, this is more because of a combination of complacency and surprisingly robust economic performance than any special status enjoyed by Australian homeowners. Recent modeling work by Moody’s Analytics indicated that it does appear as if housing is modestly, but not excessively, overvalued relative to fundamentals.

…Overall, the picture of the Australian economy is a confusing one. On the face of it, it is one of resilience—the unemployment rate has been 4% to 6% since 2003, and annual employment growth has continued since the early 1990s. Below the surface, however, the labor market is shifting away from full-time work toward part-time and casual employment. This makes the total employment figures, which treat full- and part-time workers equally, overly rosy. If we examine growth in hours worked, which provides a more complete view of the state of the labor market, recent trends have actually been quite weak (see Chart 9).

This trend toward part-time employment has the potential to cause a major shift in median household income, as people are remunerated less for fewer hours worked. In terms of consumer credit, strong part-time job growth probably limits both the upside and the downside potential of the industry. On the one hand, people are employed, so they have some capacity to make payments on past debts. Their means and desire to increase their total debt levels, in the context of a country with bloated mortgages, are probably also limited, meaning that credit growth will likely be muted in coming years or quarters.

The Australian economy is in a state of transition: not, like much of the world, from a cyclical downturn to an upturn, but from one structural mode of growth to another. This is a well-worn path for Australia—resources and commodities booms have ended in the past, and Australia has remained a vibrant, prosperous place, where a lot of value is added and quality goods and services are produced. Rocks and crops generally provide the gravy that causes Australia to rise in the GDP per capita league tables, but the service-based consumer economy represents the meat and three vegetables. As Australia transitions from a mining-led resources boom back to a more traditional growth path focused on housing, retail and manufacturing, the performance of the economy may feel bad, but in reality, it will simply be a return to normal after a long journey through the countryside on the back of a Maglev super train. A crash will likely be avoided, provided the U.S. continues to recover and the Chinese economy does not implode.

Structural transition is also occurring in banking and credit. It has been 30 years since the Aussie was floated and the economy was opened up to the world; one could claim that adolescence is over and that the banking sector has reached some level of maturity. Credit growth seems to have stabilized, though there remains an unhealthy concentration in credit backed by the fickle values of houses in dusty but orderly suburbs.

Irrespective of the complacency of local analysts, who sound a lot like many U.S. housing cheerleaders circa 2006, this exposure represents a major concentration risk for banks and the Aussie economy. Houses appear to be overvalued. One merely hopes that the looming correction is a smooth one.

The credit card sector looks underserved at present, and that seems to us like a quixotic trend, given the high level of pre-existing mortgage-related finance. A modern credit scoring and reporting industry will undoubtedly assist the growth of the credit card sector. Currently, those with stellar credit histories pay basically the same rates as many with multiple delinquencies on their file. In a world where credit cannot be properly assessed, the only way for banks to operate is to assume that all clients are deadbeats. The adoption of modern credit reporting should prompt a surge in the sector, with most consumers paying lower interest rates without a large increase in overall riskiness.

Australia enjoys the best-hedged economy in the world. Part of the uncertainty about the outlook is because of the fact that analysts have a hard time comprehending how any country could have continued to grow during the Great Recession. Australia did grow and may well continue to outperform a struggling global economy. At worst, Australia might start to perform like a country living through the worst global downturn in more than a generation.

Uncertain growth is always superior to certain stagnation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.