The Grattan Institute is all over the press today with its new report on the winners and losers on the mining boom. I’ll leave the overall report to UE but given the manufacturing section quotes me I’m going to fire back. Here it is:

The resources investment boom has put pressure on other industries. The high exchange rate linked to the mining boom has disadvantaged firms that export or compete with imports. The high dollar also provoked fears the boom has permanently damaged industries such as tourism and manufacturing. A trade unionist, a business group representative and a journalist express this view:

“We need to make sure that we keep this industry alive because if we don’t, the impact on manufacturing centres across Australia will be drastic, it’ll be severe and it’ll create a type of society that I don’t think most Australians want.” Paul Howes, Australian Workers’ Union

“We have grave concerns that there could be a hollowing out of the economy. And when the dollar depreciates, when th resources boom drops off in the future, we will not have the industry structure that we have today.”

Tony Webber, Federal Chamber of Automotive Industries

“When the commodity boom ends, manufacturing income will not rebound…. The death of manufacturing is the permanent loss of the skills and intellectual property that enables such a ramp up to occur.”

David Llewellyn Smith, Macrobusiness

In this chapter we ask:

How have the trade-exposed sectors fared through the boom?

Is the boom the main driver of change in these sectors?

Has the boom cause long-term damage to industries and capabilities that will be needed after the boom is over?

We find that the main trade-exposed sectors, notably manufacturing, tourism, education of overseas students, and agriculture, have survived the boom in reasonable shape. They are producing goods and services at or above their levels prior to the boom. Agriculture and education exports have grown strongly, reflecting strong demand from the same growing Asian economies that have driven the mining boom. Yet tourism and manufacturing output have hardly grown over the period, and their exports experienced outright declines after 2008.

Aside from agriculture, these trade-exposed sectors grew more slowly than the rest of the economy. With mining expanding

rapidly, and strong demand for non-traded goods and services, the GDP share of other trade-exposed sectors has declined. Yet the mining boom is not the prime cause of manufacturing’s declining share of GDP. Rather, the boom has temporarily accelerated a long-term decline. Manufacturing has declined as a proportion of the economy in Australia and most other high income economies for decades. As incomes have risen, households have spent more on services.

The shift to an open Australian economy with lower tariffs that began in the mid-1970s has also played a role. As well, the global manufacturing sector has relocated much of the manufacture of less complex goods to

China and other economies where costs are lower.

The boom has even helped parts of manufacturing industry.

Demand from the resource sector for Australian manufacturing sector output has risen by about 0.6 per cent of GDP through the decade, partly offsetting the pressure caused by the high exchange rate.

At the same time, Australian production and export of more sophisticated manufactures (including technical equipment and pharmaceuticals) and new services has continued to grow strongly during the boom.

The experience of other countries that have been through a big shift in exchange rates suggests that Australian manufacturing is unlikely to have suffered permanent damage. If exchange rates decline, manufacturing is likely to bounce back to trend within a few years. Services exports are likely to respond strongly, too.

Yet the experience of comparable countries may not be an entirely reliable guide. In those countries, exchange rates were typically elevated by about 20 per cent for five years. In Australia, the exchange rate has been elevated by more than 30 per cent above its pre-boom level for almost a decade.

What should governments do? The risk of permanent damage to the trade-exposed sectors is low and does not warrant temporary intervention to protect affected industries. There is little evidence that intervention to protect or prop up any industry is cost effective. Policy to lower the real exchange rate can help, but as noted in Section 3.5 the only way to sustain a lower real exchange rate is to reduce domestic expenditure. The recent shift towards tighter fiscal policy and lower interest rates is helping to achieve this.

3.1 The mining boom has squeezed other tradable industries hard

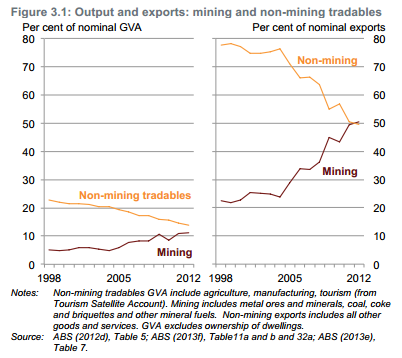

In dollar terms, the fortunes of the resources sector and other tradable industries have been starkly different through the boom, as Figure 3.1 shows. High resource commodity prices and the high real exchange rate have reduced the share of nominal GDP contributed by other trade-exposed sectors. Export shares have changed even more starkly. Non-mining exports plummeted from around 78 per cent of exports by value in the late 1990s to 50 per cent in 2012, while mining rose from around 22 to 50 per cent.

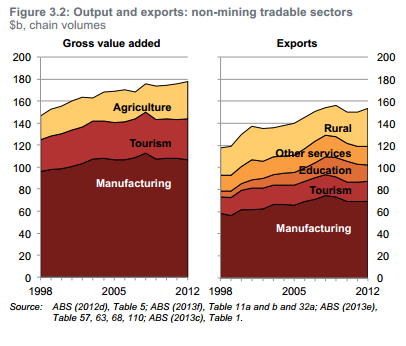

Nevertheless, the volume of goods and services produced in the trade-exposed, non-resource sectors did not fall (Figure 3.2). Exports of all broad export-oriented sectors remain above their 2002-03 levels, though below their levels of 2007-8 (with the exception of the rural sector). After resources, manufacturing remains the largest trade-exposed sector and the largest export sector.

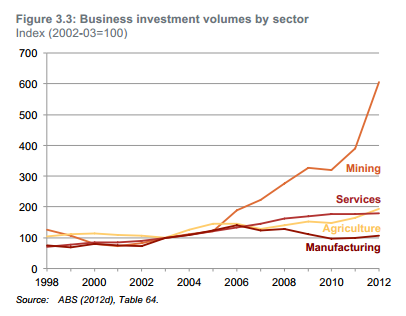

Investment levels indicate how the trade-exposed sectors regard their future prospects. Figure 3.3 shows that investment in manufacturing increased through the early 2000s, peaking in 2006 and then declining somewhat. Yet the fact that the volume of investment remains above its level in the late 1990s and early 2000s suggests that many manufacturing firms see a viable future.

I quick “thanks for nothing” for sticking me in with the quotes of vested interests. Anyone would think Dutch disease had never been examined by anyone else.

As for the case that manufacturing is hunky dory, there are obvious flaws. The first is that comparisons to other manufacturing rebounds is very weak. Other nations with 10% terms of trade rises and falls do not compare with Australia’s 60% rise. Moreover, without knowing who was looked at we can’t tell if the comparisons are viable, as the report itself admits, so why the strong conclusion that it’s all good?

Advertisement

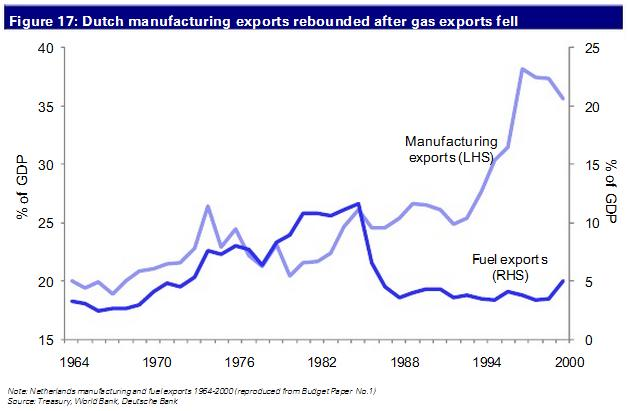

The case of the Dutch themselves bears this out. Their eponymous case of the ‘resources curse’ reduced manufacturing output from about 25% t0 20% before rebounding:

Not so hard to rebound from that fall. But what does it mean when you’re down to just 7% of the economy? It makes it much harder to rebound, obviously.

Advertisement

That leads to another point. The whole argument against allowing Dutch disease is that it leaves you vulnerable when the terms of trade fall. That’s an argument that only makes sense in terms of the relative contributions to growth made by sectors, not absolute levels. In the case of the manufacturing volumes being sustained at late 1990s levels, some fifteen years ago, how is that not serious and enduring harm in reference to pulling its weight on the rebound?

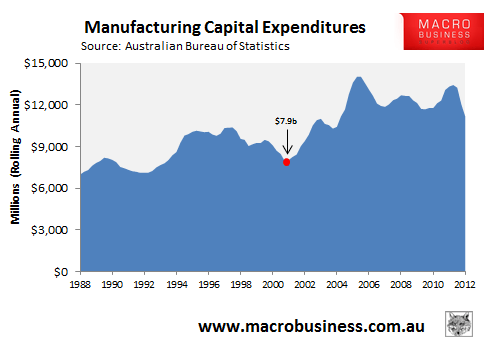

The same point can be made using Grattan’s use of capex data. I could just as easily point to the fact (and have) that manufacturing capex intentions are at levels first reached in the late 1980s. The red dot below represents manufacturing capex intentions for the year ahead):

Advertisement

So we have a manufacturing sector that’s down to 7% of economic output and investing at levels first reached 25 years ago but we’re supposed to conclude that its rebound is about to make a material contribution to rebalancing?

I’ll close by pointing out a couple of logical problems with the report. First, it goes on to argue that the government wasted much of the boom by giving away revenue as tax cuts. What is the counter-factual then? If the government saved much of the tax windfall it would have meant a different mix of growth including a lower dollar and higher tradables output. How come it’s a problem for one component in the alternative scenario but not for the others? Put another way, would government debt be a problem now if the economy were not so profoundly unbalanced? Nup.

Finally, can we please get past the fallacy of induction that dogs all of these the “manufacturing decline is inevitable” arguments. As the white swan loving European’s discovered as they sailed into Perth harbour hundreds of years ago, just because something has happened before does not mean it must happen again.

Advertisement

Such illogic is unbecoming of think tanks, media, central banks and governments.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.