Filling in for Jeremy Grantham in the new edition of the GMO quarterly, find Ben Inker’s take on tapering and the stock market. Excellent as usual.

To investors focused on U.S. equities, it may be easy to forget the investing excitement of this spring, but for others, particularly anyone running a portfolio predicated on asset class correlations being low, this has been a pretty shocking couple of months. From May 22 to June 24, the S&P 500 lost 5.6%, MSCI EAFE lost 10.1%, MSCI Emerging fell 15.3%, the Dow Jones/UBS Commodity index fell 4.5%, the U.S. 10-year T-Note fell 4.4%, and the Barclays U.S. TIPS index fell 7.1%. For good measure, the J.P. Morgan Emerging Debt Global index fell 10.8%, the German 10-year Bund fell 5.2%, the UK 10-year Gilt fell 3.4%, and the Australian 10-year bond fell 6.5%. Equity markets have made a fairly sharp recovery since then, with the S&P 500 actually hitting new highs, but lots of other asset classes are still licking their wounds. In light of the generally negative correlations between stocks and bonds of the last decade, the universality of the declines looks pretty weird. For those schooled in thinking that the only “risks” that matter for investors are growth shocks and inflation shocks, it’s significantly more than just weird. To anyone of that mind, it’s a bit of a soul-searching moment, and it forces you to either treat the episode as a one-off event that will hopefully not happen again anytime soon or as a challenge that requires you to rethink your risk model. Not surprisingly, at GMO we believe it to be the latter, and that most investor risk models are missing an important piece of the puzzle.

This is not to say that growth shocks and inflation shocks don’t matter. They do, as they are two of the basic ways investors can lose significant amounts of money in otherwise diversified portfolios. Risk assets generally lose money in depressions, and nominal assets generally lose money in unanticipated inflations. But there is a third way to lose money, and it was what bit the financial markets in May and June. We call it valuation risk at GMO, and it is the risk associated with the discount rate on an investment rising. It can impact a single asset class for idiosyncratic reasons, but it can also affect a wide array of asset classes for a systematic reason. This spring it affected a wide array for a systematic reason.

The proximate cause of the decline was a statement given by Fed Chairman Ben Bernanke to Congress that quantitative easing would taper down within the next few Federal Reserve meetings if economic data continued to improve. Bernanke clearly did not mean for the market to freak out over the statement, as can be seen in the frantic backpedalling offered by various Fed governors, including Bernanke himself, in the following weeks.But freak out the market did, and not just one market, but seemingly all of them. Why?

If he was of a mind to, Bernanke could choose to consider the whole thing a compliment. It is only because markets all around the world have been doing what he has asked them to that his words had the impact they did. Bernanke has been quite clear that a major purpose of easy monetary policy, and quantitative easing in particular, is to prod investors to bid up the prices of assets. In this, he has succeeded, even if it has not had the knock-on effects on the real economy that he might have hoped. To understand what has gone on, it is helpful to look at our 7-year forecasts in a way that we don’t normally show them.

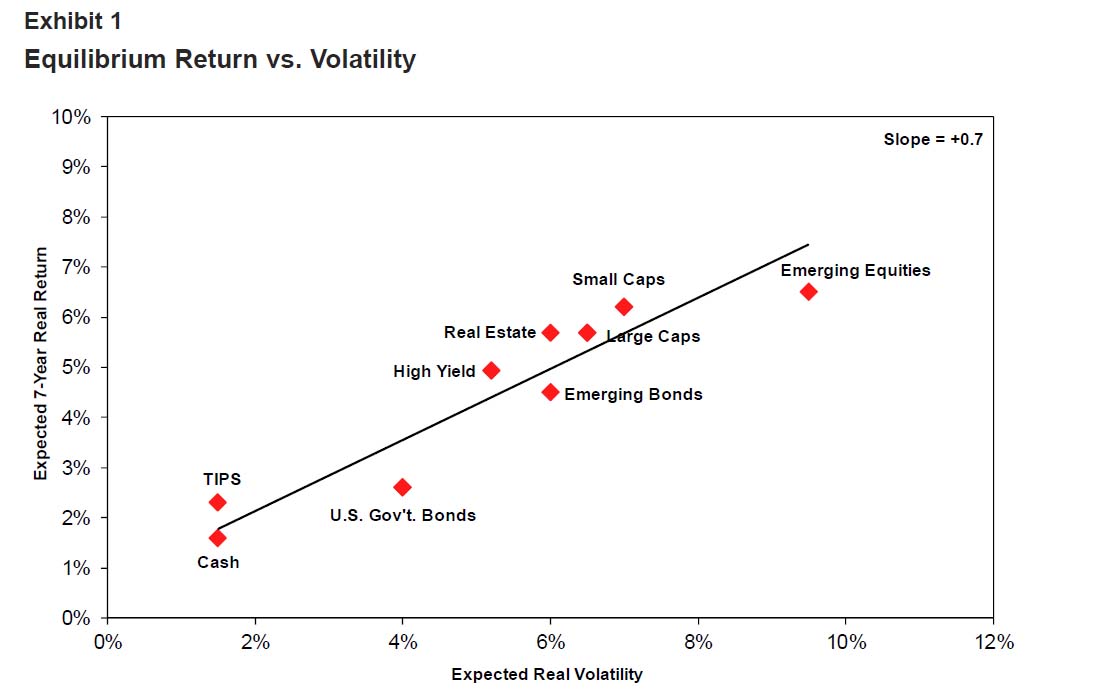

Exhibit 1 shows our estimated equilibrium returns for asset classes as a scatterplot with expected return on the vertical axis and expected volatility as the horizontal axis.

The various asset classes have significantly different expected returns, but the dots do have an associated pattern. This can be seen in the regression line, which has a notably positive slope. Before we get any further, I hear several colleagues’ voices in my head shouting at me that volatility is not risk. They are correct. At GMO, we do not believe that investors get paid for taking volatility, but for taking “risk,” and risk is a multifaceted concept for which volatility is a poor proxy at best.2 But for this purpose I’ve only got two axes to play with and I have to do something, so please bear with me, recognizing the blunt nature of the tool I’m using.

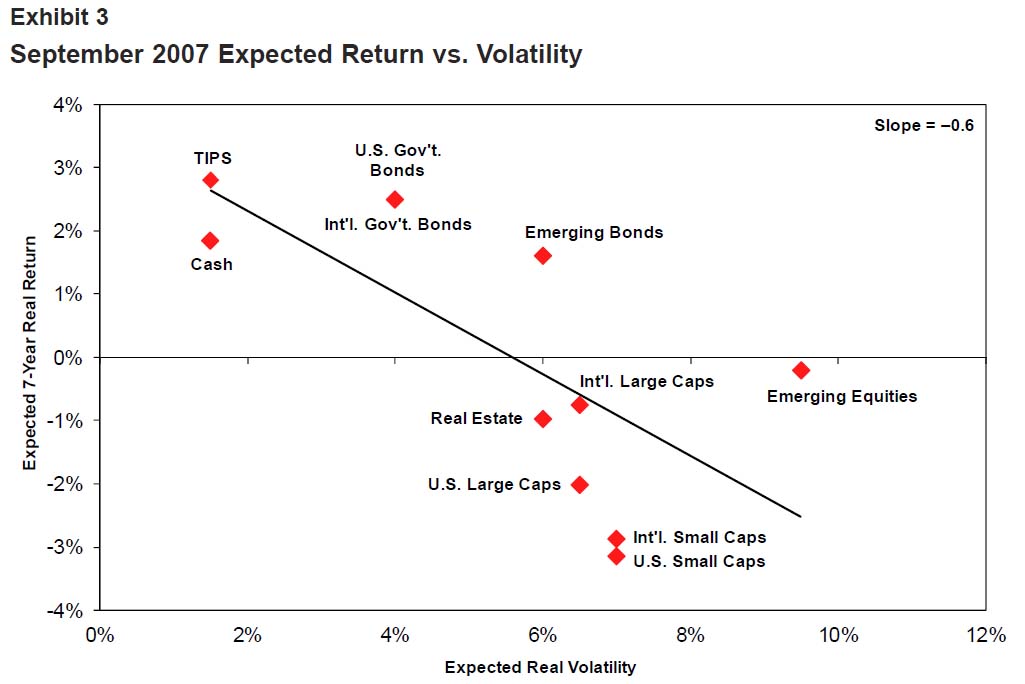

Exhibit 2 shows our current 7-year forecasts as a similar scatterplot.

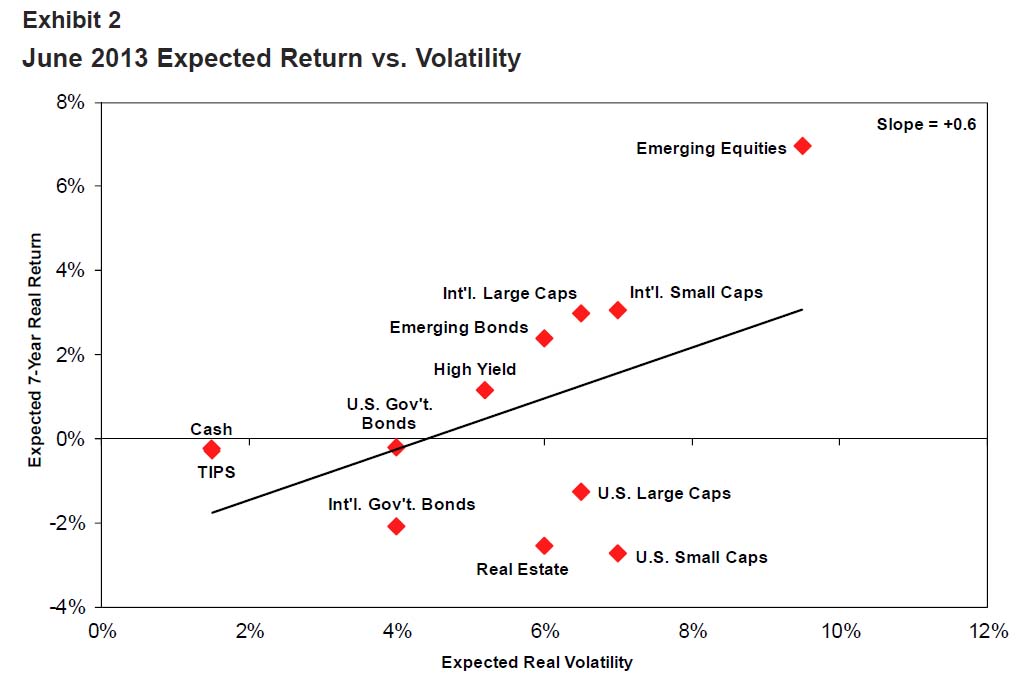

Two things jump out from Exhibit 2, or at least they do for me. The first is that the slope of the regression line is pretty close to normal. This is not always the case. Exhibit 3 shows the equivalent chart for September 2007, and you can see that the line at that time was actually downward sloping – investors were paying for the privilege of taking volatility, rather than getting paid.

The second point is that the whole line has been shifted down about three points relative to the equilibrium level. This combination is exactly what Bernanke has been trying to accomplish. By pulling down both today’s cash rate and the market expectation of future cash rates, the Fed has increased the relative attractiveness of pretty much all assets other than cash and, as a consequence, their prices have risen. Since 2009 it has been difficult to avoid making money in the financial markets. Nominal bonds, inflation linked bonds, commodities, credit, equities, real estate – everything – has been bid up as a consequence of the very low expected returns of cash. And this gives today’s markets a vulnerability that has not existed through most of history. Today’s valuations only make sense in light of low expected cash rates. Remove that expectation, and pretty much every asset across the board is vulnerable to a fall in price, as the rising real discount rate plays no favorites.

We have known this for a while, but the trouble is that there is no easy way to resolve this problem. There is no asset class you can hold that would be expected to do well if the real discount rate rises from here. Under normal circumstances, a rising real discount rate would probably come on the back of rising inflation or stronger than expected growth, which are diversifiable risks in a portfolio. But May’s shock to the real discount rate came not because inflation was unexpectedly high or because growth will be so strong as to lift earnings expectations for equities and other owners of real assets, but because the Fed signaled that there was likely to be an end to financial repression in the next few years. And because financial repression has pushed up the prices of assets across the board and around the world, there is unlikely to be a safe harbor from the fallout, other than cash itself.

I would like to say that having warned investors of this problem, we were able to spare our clients losses in this environment. But most of the reason we have been complaining about this issue as loudly and continuously as we have is that there is no good way out. During the market hiccup, we certainly did not do as badly as some other investors who have invested without regard to the risk of a shock to real discount rates. But to avoid taking any losses in a situation like this, you really need to know when it will occur. Avoiding losses as real discount rates rise requires sitting in cash, and we know cash offers no return today, while other asset classes are priced to give positive returns, even if lower than their historical averages. We have held more short-duration assets than normal for the last couple of years in asset allocation portfolios where that is appropriate, and that did help cushion the blow a bit, but did not save us entirely. The scatterplot in Exhibit 2 shows that investors are getting paid to move away from cash if things revert to normal over 7 years. If things are going to revert over 2 years instead, cash suddenly becomes a pretty appealing asset by comparison, but we don’t know that that will happen. As a result, we own assets that we know will get hit the next time markets are shocked by the prospect of discount rates normalizing.

In honor of the currently scorching temperatures, I’d like to put our current positioning in terms of a summer camp metaphor. We’re in a canoe race to the other side of the lake. We know all of the canoes are old and a bit leaky in the best of times, and there’s a storm coming. If we knew the storm were going to break now, we’d just stay in the cabin and laugh at everyone else as they were forced to turn around and trudge back to the cabin, sopping wet and half drowned. But we don’t know when the storm will break or even if it might miss us altogether, so we’ve stuck an extra guy in the middle of our boat with a bucket instead of a paddle. We know it will slow us down, but it will go a long way to help ensure we don’t sink along the way, even if we’re resigned to the likelihood of a long slow paddle in the rain, sitting in water up to our ankles.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

{kind=link}