Before any of you accuse me of flip-flopping, let me say that the following does not change my outlook for house prices. My base case is unchanged, that prices will struggle to do much better than inflation this year and will be under pressure in the next several years as the economy falls off the mining investment cliff. In the longer term as well I remain of the view that we are in for a slow melt of Australian asset prices and that the returns on offer in no way justify the risk of a more serious shakeout.

But that does not mean that I am blind to bullish arguments for rising house prices. There are some worthy of consideration and a number of recent data points make examining them a worthwhile endeavour. I’ve listed them below in no apparent order.

1. Don’t fight the RBA

The RBA wants to see house price rises. After his recent speech, RBA governor Glenn Stevens answered this question directly:

Advertisement

That’s pretty straight forward. The RBA wants to see gently rising house prices to boost construction activity. The question of how much acceleration in price rises it would allow is not as straight forward as it appears. As the economy falls down the mining investment cliff for the next three years, it is quite unlikely that the current ramp up in dwelling construction will be enough to support growth and employment. For that, Australia will need a much lower dollar and the RBA is the only one who can deliver it. It will be loath to raise rates, therefore, even if house prices accelerate and it has failed to prepare for this outcome by ignoring macroprudential tools. It is a long shot but not impossible that Australia finds itself following New Zealand’s example but is even less prepared on the policy tools front. The RBA has one weapon, however. It could jawbone the housing market as it did in 2010.

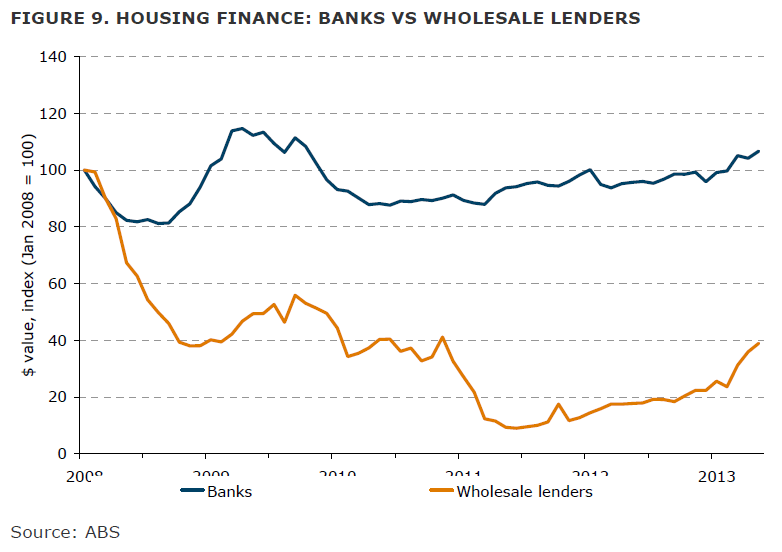

2. Non-banks are growing competition

Non-bank lending via securitisation markets has been asleep (or dead more like it) since 2008. But it has recently resuscitated as global credit spreads tightened over the past nine months on the “Draghi put”. This has re-opened the Australian securitisation market and suddenly boosted non-bank mortgage market shares:

Advertisement

The non-bank market faces a new challenge now as the US Federal Reserve prepares its exit from quantitative easing, which has already seen Australian credit spreads jump well above the floor that they held throughout the European crisis. One possible scenario, however, is that after a period of shock rises in global interest rates, bond markets will settle down and funding for securitisation remains competitive. In this scenario we could see falling Australian credit standards and a greater distribution of credit.

It could run for a few years through rating agency warnings as the current account deficit blows out.

3. Rising immigration and housing shortages

Advertisement

In my view, housing shortage arguments are largely poppycock. They always assume, wrongly, that both supply and demand are inelastic. Supply response is certainly constrained in Australia. But so too can demand be. If conditions deteriorate, folks just move in together to budget and demand for dwellings falls.

Nonetheless, Australia’s ponzinomics system is enjoying another little boom in short term migration. This does not support house purchases directly but does support rents and, in an environment defined by the search for yield, that will support investor purchases. This chart is a year old but you get the idea:

It is worth noting that despite this pressure rents have remained stagnant for the past few years (outside of the mining boom cities). Perth is now loosening fast too so this is not a slam dunk.

Advertisement

As well, permanent migration (the purple line) is well off its highs and is, in fact, now running around its long term average so you would not expect any great surge of demand from the owner-occupier segment:

4. Safe haven buying from Asia

This is obviously a hot topic and last week’s NAB quarterly property sentiment survey provided some new insight:

We have seen a big pick up in recent surveys in foreign buyer activity in the new property market to around 12-13%, from 5-6% seen in much of 2011. Queensland (20%) and Victoria (14.1%) remain the choice locations for foreign investors. Asian investors (mainly Chinese) have been driving this trend according to the latest data from FIRB. A number of factors are driving Chinese investment into Australian property, including initiatives to curb real estate speculation in China, diversification for Chinese property investors and immigration potential.

Advertisement

A few points. Notice that the activity is very strongly oriented towards new dwellings. Established dwelling demand is up marginally but this is probably a function simply of the base effect of having less first home buyers. With new foreign demand for new property booming, that will actually add supply and ease price pressure for existing dwellings. For example, Melbourne’s mini-Chinese ghost city in Docklands.

I also think that the falling dollar (with 25-30% to go) will deter this segment over time. Not much point seeking a safe haven at that price.

Still, demand is there and with liberalisation of the capital account in China a possibility in the next decade, it may grow as the Australian dollar settles.

Advertisement

5. The politico-housing complex

This is my favourite. Through words and actions, both Federal political parties have indicated that they want to see never-ending house prices rises. The combined commitment to surplus, in tandem with the current account deficit, by definition demands that the private sector borrow to keep growth going and we all know that that means mortgages.

Joe Hockey has said that he would like to see Australian households “deploy their balance sheets”. On innovative new businesses Joe? I think not! His commitment to a Son of Wallis banking inquiry makes sense in theory but could very easily be a smokescreen to reboot mortgage lending via the Canadian model of government support for securitisers. I don’t think the nation is that bonkers but you never know.

On the Labor side, the party of the worker has done as much to build in house price rises for all and sundry as the LNP has. The state-level demand stimulus and supply restrictions of the past decade and a half have both been awful ALP economics. At the Federal level, the 2009 FHB grant was integral to the great blow off in house prices and I have since seen Lyndsay Tanner defend the policy on the grounds that it is appropriate in circumstances where a big fall in aggregate demand is a risk (sorry, can’t find the quote) rather suggesting that it could be used again.

Advertisement

I have been told by reliable sources, however, that the original stimulus package proposed by Treasury did not contain the grant. That means Cabinet shoved it in and, contrary to popular opinion, that there are some folks in Canberra that think outside of the politco-housing complex.

The LNP has been more sensible with its demand side stimulus (excepting Costello’s late nineties capital gains cut). I am not aware of any LNP government (correct me if I’m wrong) that has put a grant on existing dwelling purchases. And as they’ve taken power in the states in the last two years, LNP governments have all shifted grants to new dwellings.

Finally, if the Federal FHB grant were to be repeated, I do not think it would be as effective. It would no doubt still work but would run out of puff at a lower level as well as reverse more quickly as the surrounding economy struggled with falling mining investment.

Advertisement

Conclusion

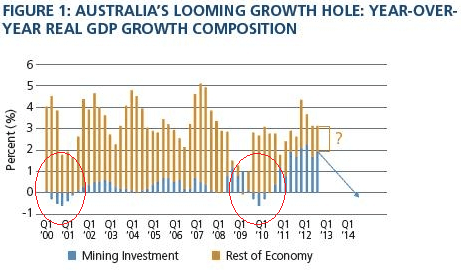

So there you have it, my best five arguments for why house prices may rise further. Are they convincing? I don’t think so given the magnitude of the challenge ahead. The following chart from Haver shows the contribution that mining investment has made to Australian growth over the past two years (the blue bars):

This argument could go either way. The two biggest surges in the great run up in Australian house prices transpired during mining growth recessions owing to monetary and fiscal stimulus. However, the current mining recession will run for four or five times longer than the last (with some offset from net exports). This time around, the fiscal stimulus can’t be be repeated, monetary policy is held back by post-GFC household prudence and the dollar is far higher than on both occasions (so far!). All of this will add up to stalled income growth, and probably falling at some point.

Advertisement

I continue to conclude that the five points above add up to enough firepower for house prices to partially offset but not overcome the Australian adjustment ahead.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.