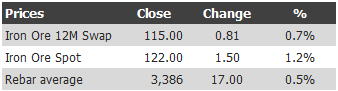

Find below the iron ore price table for July 4, 2103:

I’m doubtful that we can get to $130 here but on we go. Not sure why the 12 month is rallying. Nothing has changed in that time frame.

Find below the iron ore price table for July 4, 2103:

I’m doubtful that we can get to $130 here but on we go. Not sure why the 12 month is rallying. Nothing has changed in that time frame.