From Africa to Australia, opportunities to develop small iron mines are fast disappearing, as cash dries up and miners are unable to compete with the crushingly low production costs of the sector’s heavyweights.

In Australia alone, a half a dozen or more projects pegged by prospectors in better times sit stranded in the outback with no timetable for development.

Most are running short on money and have stripped payrolls and equipment spending to a bare minimum, awaiting a turnaround that forecasters predict is a long way off at best.

Companies such as Aquila Resources Ltd, Flinders Mines Ltd and Iron Road Ltd, which a year ago were leading a wave of new investment in iron ore, have had their stocks gutted as investors turned cold on their prospects.

“This is not the time to be developing a new iron ore mine, the big boys are making sure of that,” said Keith Goode, an analyst for Eagle Mining Research.

Global miners Vale, BHP Billiton and Rio Tinto are increasing their supply dominance in the world’s second-biggest shipped commodity market after oil.

The three already control some 70 percent of seaborne trade and are spending billions of dollars on new mines to capture an even bigger share, just as the price outlook for the steel-making raw material deteriorates and a supply glut looms.

Iron ore prices are forecast to reach a four-year low in 2013, according to a Reuters poll. In a few years, some analysts see prices under $100 a tonne.

The majors are cornering the market with costs of $30-$50 a tonne, compared with estimates of up to $100 for new entrants.

Add to that, expenses around rail lines that can stretch hundreds of kilometers across deserts or through jungles, limited port allocations and lower grade ores and it’s little surprise new entrants are struggling.

Advertisement

Meanwhile The Australian sees it as all good for the juniors:

AUSTRALIA’S band of small iron ore miners has quietly amassed cash holdings of well over $1 billion, leaving them well placed to snap up cut-price acquisitions or ratchet up their returns to shareholders.

BC Iron yesterday became the latest junior iron ore producer to report a big uplift in cash holdings on the back of the June quarter, delivering a company record quarterly cashflow of $85 million.

In addition to paying down $48m of debt, BC Iron lifted its cash position over the three months from $99.8m to $138.5m.

The boost in BC Iron’s cash position came just days after fellow miner Mount Gibson Iron declared it had boosted its cash holdings by $34m to $376m, with the company debt-free.

Other smaller iron ore miners such as Atlas Iron ($404m in cash and $263m in debt at the end of March) and Grange Resources ($164.3m in cash at the end of March) are yet to update the market with their latest quarterly results, but are likely to have further strengthened their balance sheets during the period.

The balance sheet boosts being reported show the ongoing cash-generating ability among the smaller iron ore miners despite investor gloom around the outlook for resources and economic conditions in China, which has seen the share prices of many in the sector plunge from year highs.

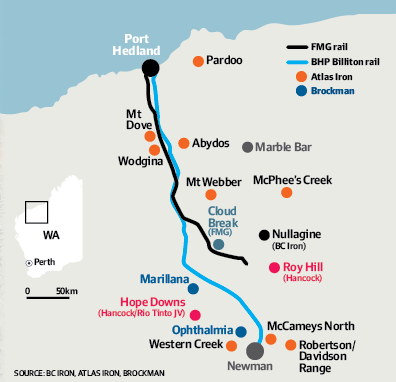

In the great game of market share dominance these are prey not predators. Meanwhile, Pilbara rail argy bargy goes on. From the AFR:

Advertisement

Atlas Iron is concerned that efforts by fellow iron ore junior Brockman Mining to gain access to Fortescue Metals Group’s Pilbara rail network may stymie its own attempts to clinch its own haulage deal.

Atlas’s opposition to the West Australian government granting Brockman access to Fortescue’s rail line was confirmed on Monday when its submission to the state’s Economic Regulation Authority was released.

“One of the key principles of access regulation is the primacy of commercially negotiated contracts,” Mr Hancock wrote. “Atlas Iron is concerned that the applications under the Access Code may lead to a situation where commercially negotiated access is compromised.”

I’m no haulage expert but I must say that two rail lines, plus the third being proposed by Roy Hill, and a fourth being explored by Aurizon, doesn’t look very efficient. In any normal universe, Gina and Andrew would surely be exploring a shared rail line. But then, given the Roy Hill vanity project would likely put Andrew out of business, that can’t happen.

We could swing very quickly from rail tension to an abundance of Pilbara rail white elephants. Which is no doubt why Andrew can’t give his rail assets away.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.