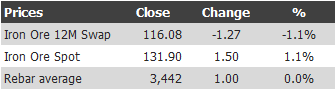

Find below the iron ore price table for July 18, 2013:

So, iron ore spot powers on despite caution entering the swaps market and the rebar rally stalling. As we all know by now, iron ore can do this on restock dynamics so I won’t say it can’t continue but not very far this time. With soft growth, abundant steel and strong rebalancing rhetoric from authorities there is little incentive for a big restock.

Meanwhile, Reuters did a better job of assessing the major producers dig and dump strategies than did Gina’s AFR yesterday:

Record iron ore output from BHP Billiton (BHP.AX) and other mining giants appears to defy logic, with demand for the steel-making raw material cooling in top customer China and a price-eroding supply glut looming.

But the sector’s heavy guns are digging more for less to tighten their stranglehold on the world’s second-biggest commodity market, as competitors struggle.

In mining parlance, this is known as a “rebalancing” strategy, designed to improve the operating margins of the majors to such an extent that smaller competitors or new projects may be all but squeezed out.

“The majors want to maximise those economies of scale,” said MineLife sector analyst Gavin Wendt. “As long as they keep margins well ahead of a declining iron ore price

, they are winning.”

…The strategy of all-out expansion portends a bleak future for projects in early stages of development.

These include the $10 billion South Korean steel group Posco (005490.KS)-backed Roy Hill mine in Australia and Sundance Resources Ltd’s (SDL.AX) $4 billion Mbalam project in Cameroon and Republic of Congo.

A small army of smaller projects peppering Australia’s iron ore rich Pilbara and mid western iron belts and the Brazilian interior are also at risk.