From ANZ today comes some hopium for coal miners:

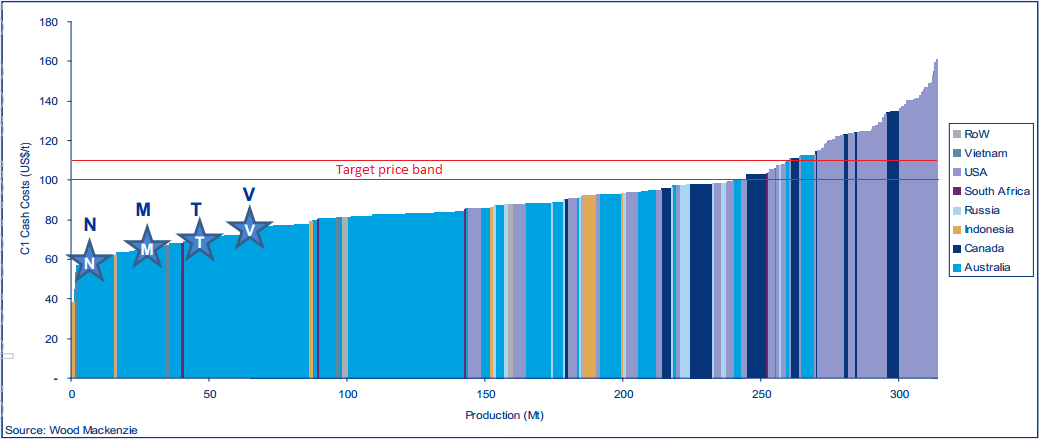

Iron ore prices fell for the first time in six days, while coking coal prices were unchanged. Coking coal may be showing signs of bottoming after a 20% decline since March. Spot prices have firmed 2.2% in the past two weeks to USD133/t FOB Australia. At current prices, 10% or 30mt of seaborne supply is losing money on a cash cost basis. Reports that high-cost swing supply from the US is starting to fall is a pretty clear sign that prices are hitting a floor. One thing to watch is the direction of iron ore, which has rallied 20% in the past 8 weeks. Rising iron ore prices are making it difficult to realise high coal prices – particularly when steel mill margins are so skinny. Slowing iron ore price gains are now in coal’s favour. Since iron ore prices are starting to fall, it could be easier for steel mills to accept higher coking coal prices – particularly if seaborne supply is starting to constrict.

That argument makes no sense to me at all. Q: Why would steel mills may more for coal because they’re paying less for iron ore? A: They wouldn’t.

Nah, we’re not at the bottom yet. And when iron ore rolls over, coking coal will likely take another leg down. 10% of supply underwater is not enough. In thermal coal it’s already double that and we are only starting to see some price stability as a result. Here’s the cost curve for coking coal:

More pain to come I reckon.