From ANZ:

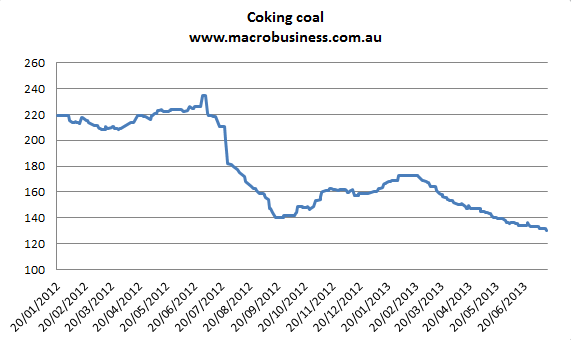

Iron ore prices rose to a 2-month high of USD126.9/t, but upward momentum appears to have waned. Market reports are mixed, with some suggesting steel mills are operating on low levels of iron ore inventories and are replenishing stocks on strong steel production – however, others suggest bids for cargoes remained low, with mills cautious due to higher prices. The third quarter tends to be a seasonally weak period for iron ore demand and domestic steel consumption, so we think the restocking phase is likely due to opportunistic buying, which will be short-lived. Coking coal prices continued to drop to USD130/t, due to global oversupply.

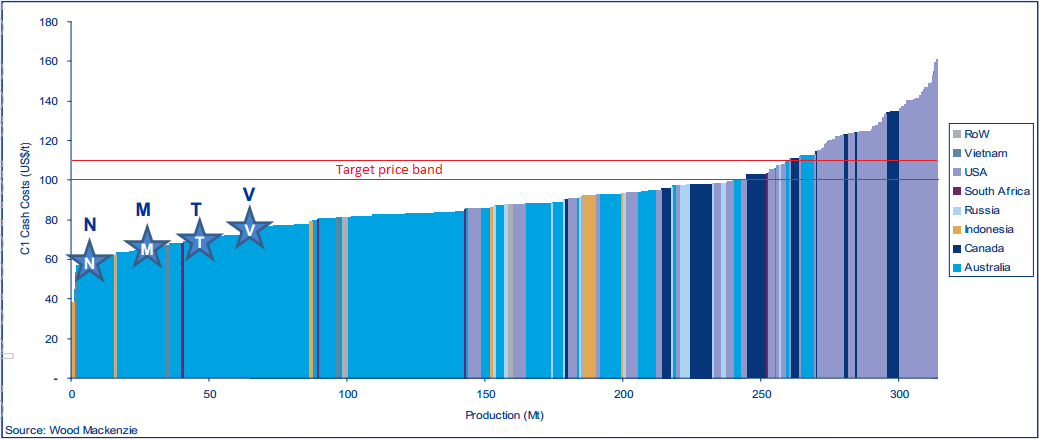

I’m still targeting $110 to get us further down the cost curve and take out production in earnest: