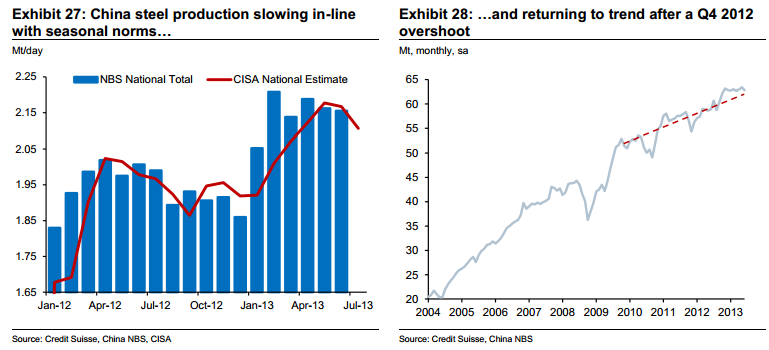

CISA’s estimate of China national crude steel output for the second 10 days of July came in at 2.13 Mt/day, up from 2.08 Mt/day over the first 10 days of the month but down from a June average of 2.17 Mt/day. The 2.08 Mt run in early July did appear slightly incongruous, so this uptick is likely a result of simple volatility as much as any structural change. Averaging the two sets of July data provides a month-to-date figure of 2.11 Mt/day, fitting the expected gradual seasonal slowdown in China steel production (Exhibit 27).

This downturn, if borne out in the NBS numbers for July, aligns well with the post-2009 steel production trend-line (Exhibit 30).

Further volatility is always possible, as is the possibility that raw demand is slightly ahead of earlier expectations.

We remain cautious on the latter, however, as mills have returned to profitability, helped in particular by lower costs of coke. This points to continued outpacing of real demand, although inventory levels have come down and are no longer seen as excessive. Indeed, some observers now believe stocks are verging on the slightly lean side.

Year-to-date crude steel production is running at 755.4 Mt/y (seasonally adjusted), in-line with our forecast for 755 Mt for CY2013 total output. A moderate seasonal slowdown would therefore generate a figure in-line with expectations.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.