CBA’s Michael Blythe is out with a recession bunking note today that’s worth a look. Blythe reckons that recession arguments stem from two sources:

The income shock reflects a belief that the commodity supply-demand balance will favour lower prices as new projects come on stream. But extra supply is needed to keep up with the growth in demand. The Chinese urbanisation process, for example, has a long way to run. So just how the supply-demand balance plays out is not yet clear.

The bigger income risk may be the type of demand. As economies mature the marginal dollar of GDP is more likely to come from services than from (commodity intensive) infrastructure and manufacturing. But we shouldn’t be afraid of this growth transition. The Asian emergence offers some opportunities for Australia’s non-resources economy. These opportunities are there for the taking. A richer, older Asian population will want larger and better quality housing; better quality food; more consumer durables; more education; more holidays; more health services and more financial services.

The expenditure shock reflects the likely rapid wind down in mining capex once existing projects are completed. But the resources story needs to be looked at in its entirety. About half the impact will be offset by lower imports of capital goods. And the other half can be covered by rising resource exports.

Regular readers will know that I see the combination of these two shocks creating the recession risk. So too Goldman Sachs. Blythe’s defense on this front is weak. It’s all well and good to repeat the story of endless Chinese urbanisation and commodity demand but the fact is Australia is exposed very particularly to only two commodities – iron ore and coal – both of which are undergoing structural shifts in increased supply and lower demand than anticipated. Repeating the top down story without tackling the specific dynamics of these two markets (three if you split coal) in unpersuasive.

Blythe’s other argument, that the expenditure shock can be offset by rising net exports is stronger:

Advertisement

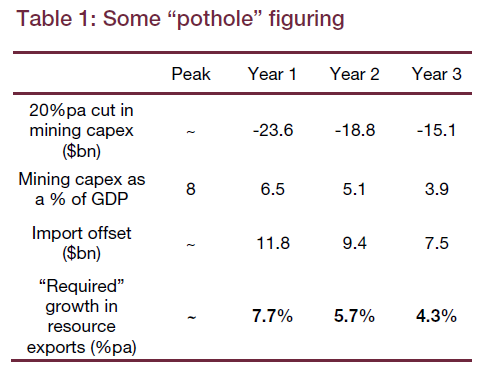

One commodity-related growth risk that is unavoidable is the end of the boom in mining construction activity. The stockpile of projects is now being worked through at a faster rate than new projects are being approved. We expect mining capex to peak at just under 8% of GDP in the second half of 2013.

So the economy is set to lose a significant growth driver. And the potential drag on the economy is quite large if this cycle follows the rapid retracement of previous episodes. But looking at the broader mining picture throws a question mark over just how threatening a more savage pull back in mining capex would be. Table 1 looks at the impact of a 20%pa fall in mining investment spending. Over three years that fall would halve the mining capex share of GDP to about 4%.

But recent RBA research concludes that about half that capex is met through imports. So in GDP growth terms there is an automatic 50% offset from lower imports. Half the pain will be “exported” to those countries that provide us with the capital goods!

The final line in Table 1 shows the required growth in resource exports to fully fill in the mining capex pothole. As the facing chart shows, these sorts of growth rates look easily achievable given the very rapid growth in the mining capital stock.

These outcomes would leave the level of GDP unchanged. Alternative sources of activity would still be needed to generate growth and absorb the potentially large labour market fallout that could follow from the winding down of mining construction capex.

Obviously some significant portion of mining capex went offshore. How much is a moot point. But remember, whatever the proportion, it has already detracted from growth on the way up via net exports as well as doing so on the way down as Blythe argues. Nonetheless, GDP growth growth was still held aloft by a mining investment boom contributing 2% plus to GDP per annum for the past three years. That is one reason why the RBA has also recently concluded that 18% of the economy enjoyed high added-value from the boom’s multiplier effects. They will all now disappear. The ramp up in mining investment was massive despite the portion that headed offshore – which is why the RBA embarked on the now infamous “structural adjustment” in the first place.

This is a good argument but not enough for me to conclude that falling mining investment wont still materially impact the level of GDP despite rising next exports, as well as offering a mix of growth that demands far less labour (as Blythe acknowledges).

Advertisement

As we argued in last month’s detailed Member’s report, whether we have a technical recession is really beside the point. It will feel like a recession owing to:

real GDP per capita, which has risen by only 3.5% in total since September 2008, likely to turn negative;

bigger falls likely for real per capita national disposable income as commodity prices and the terms-of-trade retrace; and

rising unemployment as the labour-intensive mining capex boom is replaced by the far less labour-intensive export boom.

Blythe also argues mischievously that markets are always forecasting a 25% chance of recession:

Advertisement

Perspective is important of course. A 20% recession risk implies an 80% chance of dodging any recession bullet. And, among economists, a 20% recession risk is the default forecast. Australia has experienced four major recessions over the last fifty-two years. So one recession every thirteen years on average – putting the average odds over the period at 25%. A more sophisticated calculation looks at what financial markets are pricing based on the slope of the yield curve. Our model implies markets currently place very low odds on a recession. More importantly, over the 1990-2006 (pre financial crisis period) Australian markets have on average priced a 25% chance of recession.

But this is clearly shifting the goal posts. Goldman Sachs and Saul Eslake, who have driven this debate (along with MB), do not always see a 20-25% chance of recession.

Worth a read but in the end I am no less convinced of the trials ahead.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.