A couple more global heavy-hitters join the China hard landing debate today. Stephen Roach repositions himself as a supporter of ‘manageable transition’:

China is most assuredly on the move. The debate over a strategic shift to a more balanced consumer-led growth model is over. The focus is on implementation. The 12th Five-Year Plan laid out the strategy – three pro-consumption building blocks of services-led job growth, urbanization-driven income leverage and a more robust social-safety net. But it was tough to get the ball rolling, especially in light of the inertia of China’s deeply entrenched power blocs at the local government and state-owned enterprise levels.

China’s new leadership under President Xi Jinping and Premier Li Keiqang has broken the gridlock. With a series of stunning moves in the early months of their administration, China’s fiscal and monetary authorities have been given new marching orders. The growth slowdown of early 2013 has not been countered by a typical Chinese proactive fiscal stimulus. Instead, the new leadership seems content with 7.5 to 8 percent growth in gross domestic product. Similarly, the central bank did not rush in to stem a liquidity crunch in June. Instead, it used the occasion to caution banks, especially “shadow banks,” against returning to an undisciplined and excessive expansion of credit.

This new mindset works only if China changes its growth model. A services-led growth dynamic, one of the pillars for a consumer-led Chinese economy, is consistent with a marked downshift in trend GDP growth. That’s because services generate about 30 percent more jobs per unit of Chinese output than do manufacturing and construction – allowing China to hit its all-important labor absorption and social stability goals with economic growth in the 7 to 8 percent range rather than 10 percent as before. Similarly, a more disciplined and market-based allocation of credit tempers the excesses of uneconomic investments, necessary if China is to begin absorbing its surplus saving to spur consumer demand.The message from this new approach to Chinese macroeconomic stabilization policy is clear: Gone are the days of open-ended hyper growth. Significantly, this message has been reinforced by an important political overlay. Xi’s rather cryptic emphasis on a “mass line” education campaign aimed at addressing problems arising from the “four winds” of formalism, bureaucracy, hedonism and extravagance underscores a new sense of political discipline directed at the Chinese Communist Party. The CCP is being urged to realign itself with the core interests of citizens and their need for fair and stable economic underpinnings.

Let’s recall that only one month ago, Roach was still defending the investment-led growth model so this is a shift. Having said that, I agree with all that he says. As Michael Pettis argues, to sustain its economic legitimacy the CCP needs to keep household incomes rising not growth rising. The playing field has tilted decisively towards achieving that via reform not more accelerated debt accumulation (Australia take note!) that risks Minksy dynamics and a shakeout.

Roach goes on to argue that the US needs a plan to embrace the rise of Chinese services. He might as well be addressing Australia as well. For the most part, services aren’t tradable so what you’re really talking bout here is investment on the ground in China. Given Australian business currently invests more in The Netherlands than China, the kind of people-to-people links that the Government appears to trying to generate through its Asian Century tours may be quite a good idea. Not much point leaving China to a market that doesn’t know what it is. It also suggests that integral to any FTA should be liberalising investment regimes as well as trade.

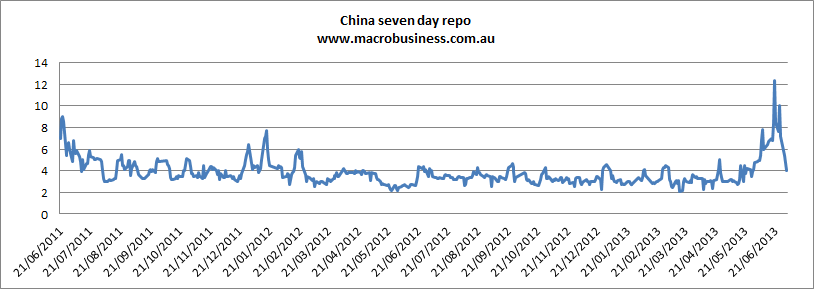

Back to Roach’s plan, it does seem to me likely that the reforms will force Chinese growth down in the short run, materially lower than the 7% goal. As more and more analysts are observing, if reform and not stimulus is the new spur to growth – a broadening of the welfare net, liberalised finance to prompt a greater focus on capital return and many other changes to lift services consumption – then it will take time for the new growth drivers to kick in. In the mean time, as finance is withdrawn from the old economy of heavy industry attached to fixed asset development, loans will go bad, more than a few local governments and banks will go bust and growth will slow.

We can already see this happening in China’s now perpetually weak PMIs and producer prices. The recent spike in interbank rates (which have now returned to the normal range) is another example:

The early indications are that the episode has hit credit growth pretty hard. From the FT:

Local Chinese media have reported that the country’s biggest banks issued Rmb270bn ($44bn) of new loans in June, about 25 per cent less than in previous months, after the cash squeeze forced them to rein in their lending in the second half of the month.

Though the real guide will be total social financing, released next week, which will show to what extent shadow banking growth has been harnessed.

All of this change rather raises the question of is China turning Japanese? Has its catch-up growth story run afoul of the same debt-trap requiring many years of slow growth to eat through the souring old economy? I don’t think so – China is a continental economy with a dynamic populace, Japan is a mercantilist state dominated by economic egalitarianism – and I expect that after a few years China’s growth will re-accelerate. The economics are sound.

But the question remains, how low do we go first? Kyle Bass of Hayman Capital argues very low:

We have become significantly more cautious regarding global growth and the potential for asset price appreciation in the second half of this year. China’s growth appears to be stumbling dramatically. This has significant ramifications for individual markets and the world economy.

The scale and pace of credit expansion in China over the last 5 years is truly staggering. The compounded annual growth of bank assets as measured by the China Banking Regulatory Commission has been 30.8%. More recently, the Chinese authorities started publishing data that includes non?bank credit growth to capture the way in which the credit creation machine has moved beyond traditional methods. “Total Social Financing” is now growing at 21.7% year over year as of April. The total size of the Chinese credit system is now approximately 256% of total Chinese GDP. To give some perspective, a 30.8% compounded annual growth of credit in the U.S. equivalent over 5 years would be an expansion of $33 trillion. This rate of credit growth is 3 times the total credit system growth experienced in the U.S. at the peak of the bubble in 2006.

This massive credit growth has been the irresistible force that has driven growth and asset pricing in China throughout the global financial crisis and maintained robust (and by world standards, incredible) GDP growth during a period of global economic crisis and anemic recovery. The Chinese authorities share the faith of Bernanke and the Fed that liquidity and credit expansion are the ultimate cure?alls and that sufficient expansion is the tide that will lift all boats above the threatening rocks of structural inefficiencies and accumulated macroeconomic imbalances. They have relied time and time again on using reserve requirements and their influence over the major banks to encourage lending and then to slow it down as they deem necessary to avoid overheating. The resilience in the Chinese economy for the last 5 years is a testament to this model.

The story, however, is never that simple and eventually, as we have seen in major economies around the world, the inescapable law of diminishing marginal returns presents itself. As in the U.S. in the lead up to the credit crisis, the marginal utility of an extra unit of credit dropped dramatically. Initially small increases in nominal terms were enough to spur real GDP growth, but then ever increasing amounts were required to generate slowly shrinking amounts of growth. Eventually massive levels of credit expansion were required just to keep the economy on track. We believe an important limit has been reached in the capacity of Chinese credit expansion to deliver real economic activity growth and wealth creation.

From the beginning of the year to March, it took almost 18 trillion RMB to generate 5 trillion RMB of GDP growth. This ratio is the lowest it has been since the depth of the global crisis. So where has all the new money gone? The data available from the Chinese corporate sector indicates that a huge proportion has been used to fill operational shortfalls and to supply working capital. The debt-to-equity ratios of Chinese companies are exploding as they funnel new capital, not into yield returning investments, but into the black holes on their balance sheets that have been created by a slowing growth environment. In the industrial sector, there is even outright deflation as overcapacity finally takes its toll.

The speed and depth of the Chinese policy response will help determine the severity and duration of this crisis. If the Chinese address the issue quickly and move decisively to rein in credit expansion and accept a period of much lower growth, they may be able to use the government and People’s Bank of China’s balance sheet to cushion the adjustment in the economy. If, however, they continue on the current path and allow this deterioration to reach its natural and logical limit, we will likely see a full-scale recession as well as a collapse in asset and real estate prices sometime next year.

The speed and depth of the Chinese policy response will help determine the severity and duration of this crisis. If the Chinese address the issue quickly and move decisively to rein in credit expansion and accept a period of much lower growth, they may be able to use the government and People’s Bank of China’s balance sheet to cushion the adjustment in the economy. If, however, they continue on the current path and allow this deterioration to reach its natural and logical limit, we will likely see a full?scale recession as well as a collapse in asset and real estate prices sometime next year.

China’s direct contribution to global growth is enormous, but perhaps equally as important is its role in generating growth in developed and emerging economies. A slowdown, whether significant or extreme, in the Chinese economy heralds very bad news for asset prices around the world. A growth crisis centered in Asia will further exacerbate the instability and volatility in Japan and have a devastating impact on second derivative marketplaces such as Australia, Brazil and developing markets in South East Asia. The combination of rich valuations and further threats to growth has led us to dramatically reduce risk in the portfolio and actively position ourselves to withstand the uncertainty and instability ahead.

I still see this as a tail risk. Even during the years following Tienanmen Square, when the Chinese economy entered semi-paralysis, it still grew at 4-5%. During the SARS scare of 2002 when again the economy was virtually shut down for a time it still grew at 7%. It bottomed at 6% during the GFC. Granted, it’s a different economy now and the very mechanisms that saw it through those crises are now the problem. But I find it difficult to believe that the latent productivity gains embedded in all of those poor and under-utilised folks won’t keep the economy from stumbling too badly.

That said, two or three years of Chinese growth at 6%, held down by sharply falling investment in fixed assets, will not favour miners, iron ore or coal prices already headed into oversupply. Nor will it favour Australia’s richly price assets. Look to a falling Australian dollar as your greatest ally.