ANZ is one of the more bullish commodity houses but today it turns bearish in a new note and downgrades its price forecasts. It sees the big picture this way:

Although liquidity tightness in China has started to ease, funding costs are unlikely to return to normal levels any time soon. If China’s central bank continues to tighten market liquidity despite a softer growth and inflation outlook, growth risks could be to the downside in Q3 and Q4. We’re already seeing this play out in commodity markets like coal, with rising expectations of defaults as a series of contracts are renegotiated lower. Banks appear to be taking a particularly hard line on commodity trading activity since the start of the year, following a rapid rise in non-participant commodity-based financing over 2012.

China’s property market is also vulnerable. Recent property investment curbs to control prices don’t appear to be working, with home prices and sales up in June. This could further induce property controls, but we feel this may accentuate the problem. Nearer-term, commodities continue to remain sensitive to China’s manufacturing outlook. The latest PMIs suggest momentum is slowing, which is also pressuring our proprietary ANZ global lead indicator (ANZ-GLI). However, this has been partially offset by modest improvements in the US and Japanese manufacturing sectors.

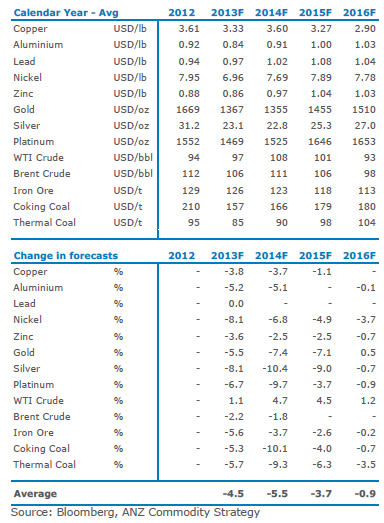

Here are the new market forecasts and note that ANZ is still defending the iron ore price floor of $120:

And on the markets themselves:

Bulk markets were mixed in June with stronger iron ore prices offsetting weaker coal prices. The diverging performance of iron ore and coking coal was an interesting dynamic – with iron ore gaining on the backdrop of flat to weaker steel and coking coal prices. Reports of shipment defaults in thermal coal are also a shot across the bow that all is not well, and with seasonal demand now declining, we expect bulk prices to consolidate or even weaken off already low bases in the months ahead.

Rallying Baltic Capesize rates propped up iron ore prices in the past month as traders bet the bottom in prices had passed. We think the bounce is just that, with prices likely to ease in the coming month as seasonal demand wanes. Freight rates are still high, but have lost their upward momentum suggesting traders have had enough for the time being. Chinese port stocks have also gained 7-8% in the past month suggesting the increased buying activity is going into opportunistic inventory rebuilding rather than better demand. In the absence of stronger steel prices (not apparent right now) spot iron ore prices should retrace back towards the USD110-115/t range in the short term.

Coking coal looks in worse shape decoupling from firmer iron ore prices over June. A flat steel market hasn’t helped, with ultra skinny steel mills margins making it very difficult to accept higher iron ore and coking coal prices at the same time. Higher coal export volumes out of Australia looks a little misleading, but shows the pricing leverage steel mills have at the moment – taking higher volumes at lower prices. In fact, rising supply in a weak market is fuelling further price declines. Although prices now look distressed (for producers), stronger steel prices will be needed to change the mood. This doesn’t look likely in the next few months.

Thermal coal is defying logic, with prices dipping heavily into the cost curve. We estimate 30% of the seaborne industry is losing money at current prices – most of it, Australian output. A falling Aussie dollar is not helping, with high cost Australian producers delaying closure decisions on the mild positive currency impact. Reports of shipment defaults highlight the negative tone of the market – and flags even lower prices in the short term. This could also create an overhang of supply into the fourth quarter blunting a price pick up from stronger winter demand. Mild support could come from reports Japan is increasing thermal power capacity, but better news has to come from the bigger “growing” markets of China and India to re-ignite stronger prices.

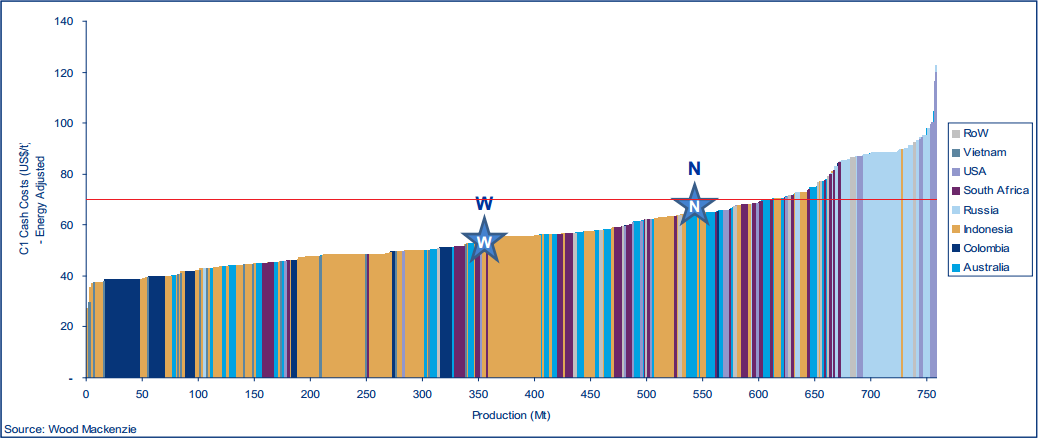

Interesting. According to Wood Mackenzie and the anecdotal evidence that I get, Australian coal is mostly not under water, at least the old mines are not. The job losses we’ve seen have been in the cancelling of expansion projects. Here is the Wood Mackenzie cost curve chart:

It’s more like 20% of global supply that is in the red and most of it is elsewhere.

Still, this is splitting hairs in terms how much supply is in the red. The most important point to note is that ANZ’s assessment that low thermal coal prices are “defying logic” as the price moves down curve. This is a problem with ANZ’s frame of reference not market pricing and it goes to why the iron ore price floor that ANZ still defends is illusory.

We all know commodity supply is inelastic on the way up because it takes along time to build new mines. But it is also somewhat inelastic on the way down. Supply will not simply disappear overnight. It can be supported by myriad forces in moves to improve productivity, an acceptance of margin compression, via subsidies or currency manipulation.

In the end supply and demand will win but only after substantial periods of oversupply and low prices. Low and lower thermal coal prices make perfect sense in this frame of reference and is the reason I see more downside for it and all of the bulks.

Commodity Call Jul13 (1).pdf by James Woods