UBS has an interesting note this morning comparing Australian share market EPS growth to global peers.

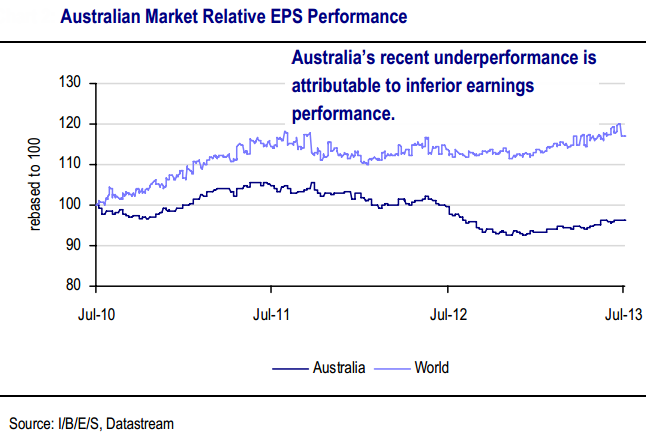

Australia Has Underperformed On Lacklustre Earnings Delivery

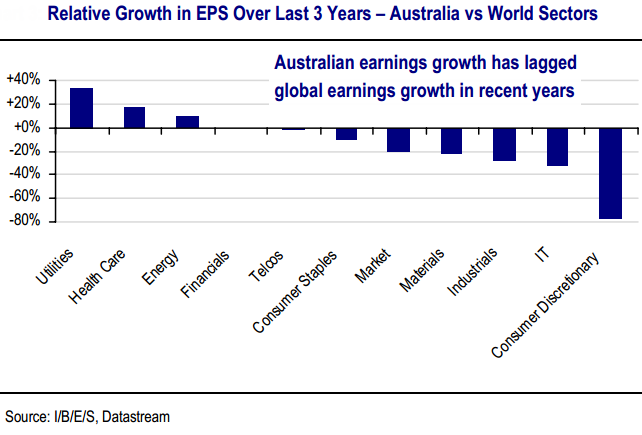

Despite improved performance over the past year, Australia has underperformed World and particularly US equities over the last three years. The blame for Australia’s underperformance rests with earnings. While sector composition has been a contributor, earnings underperformance has been broad based. Looked at in an absolute sense, 7 of 10 GICs sectors have delivered less than 4% per annum over the last 3 years.

Australia’s Poor Earnings Performance Goes Beyond A$

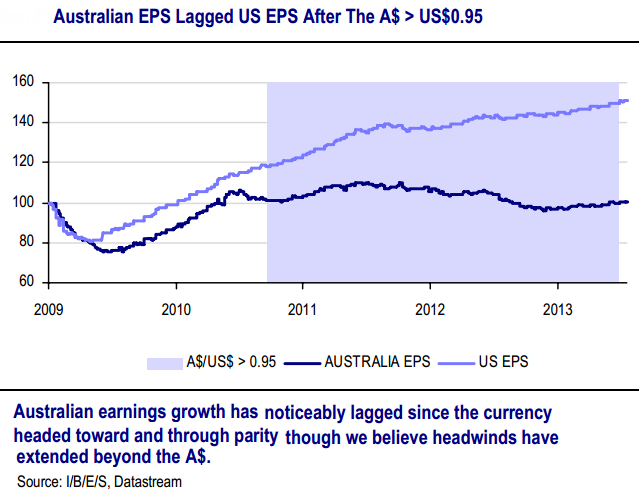

The relatively broad nature of sector underperformance suggests the A$ can’t be solely blamed. Beyond the strong currency, other contributing factors to earnings underperformance likely include 1) relatively anaemic cost reduction initiatives 2) a variety of structural headwinds hitting sectors such as consumer discretionary and 3) more recently falling commodity prices and easing capital spending.

Lower A$ Will Help But More (Self) Help Needed

Clearly the lower A$ (particularly if it continues) is a positive support for the corporate earnings cycle. From a sector perspective sectors that can benefit from a lower A$ remain attractive. Health Care has done very well but still looks well exposed to the lower A$ theme while Australia’s limited listed manufacturing sector (steel and building products) should do much better under a weaker currency regime. Companies that can deliver efficiency margin gains in a subdued top line environment should also continue to do well.

Correct and that’s the only place you want exposure. Dollar and efficiency plays. Poor EPS growth in sectors exposed to weak domestic demand is a direct result of Australia’s ongoing slow motion current account squeeze which will go for a long time to come.

We have ridden the globla P/E expansion with everyone else as tail risks assocaited with Europe diminish but but one wonders if the under-performance might not actually increase as our own problems deepen post mining boom. Alternatively, earnings everywhere may degrade if China slows too fast.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.