UBS has a fascinating note out on the new IMF data tracking Australian dollar reserve holdings:

On Friday the IMF released its Q1 2013 update for the composition of foreign exchange reserves (COFER), including for the first time the holdings of AUD and CAD within allocated reserves. Data for Q4 2012 for the two were also included. As my colleague Gareth Berry pointed out last Friday (see FX Morning Adviser – AUD Suspense Almost Over, June 27), aside from the AUD and CAD, the reserve status of the JPY was of particular interest, even though the numbers would not have factored in April’s QQE. In addition, reserve management was conducted when the word ‘taper’ was probably less relevant. Judging by recent moves in some currencies, reserve managers are unlikely to have held their Q1 flow trends.

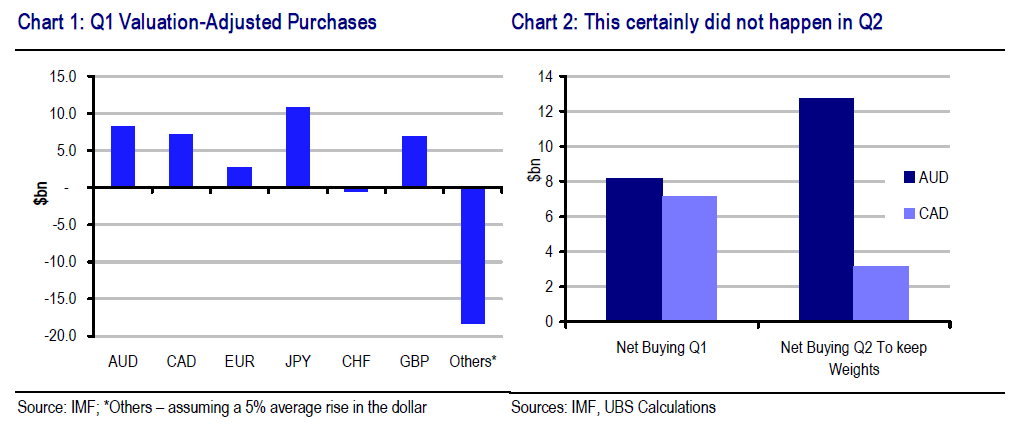

The IMF itself notes that COFER data are reported on a ‘voluntary’ basis so the end-holdings in dollar terms do not account for valuations changes. In Q1 2013, neither AUD nor CAD registered wide swings against the dollar, so the actual net purchases (within allocated reserves) are not too divergent from the raw figures reported. However, JPY and GBP amongst others did see large swings versus the dollar in Q1, while other non-traditional reserve currencies also fared poorly. Chart 1 shows reserve management flows adjusted for valuations and it’s clear that some

currencies were affected more than others by the dollar’s rise. The yen was still bought in size, perhaps reflecting the consensus view in the first quarter that the BoJ was not going to deliver any form of policy that would substantially change allocations and it was a good time to ‘sell the top’ in USDJPY. How yen holdings evolved in Q2 will be of far greater interest post-BoJ. The biggest casualty, however, was in the ‘others’ column. Ex-valuation changes, such holdings were down by 15%. If we assume that the dollar gained by these ‘other’ currencies by 5% in Q1, allocated managers still reduced holdings by over $18bn. We can debate the reasons behind the reductions, but one major consideration could be the lack of liquidity in this space, such as the Nordics. In addition, as Emerging Market Reserve Managers brace for some more difficult times, larger dollar buffers would be needed, at the expense of more ‘exotic’ investments.

We do not wish to pre-empt the Q2 COFER numbers, but some observations can also be made about reserve interest in AUD and CAD, and the prognosis is not great. Both currencies had around 1.60% weighting in Q1 allocated reserves. According to Bloomberg estimates, global reserves did not change significantly in Q2. However, AUD and CAD both fell against the dollar, especially the former. Based on quarter-end exchange rates, it would have taken $13bn in purchases merely to keep AUD at its current weight – a larger amount than Q1. Price action would suggest otherwise.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.