Ernst and Young has a new risk report out that is unsurprising but nicely summarises the state of mining:

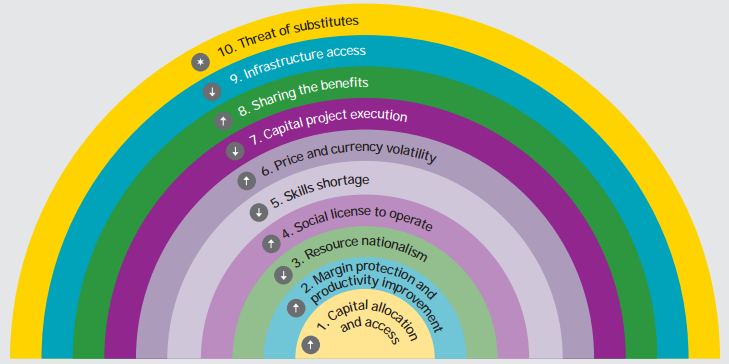

The twin capital dilemmas of capital allocation and access to capital have rocketed to the top of the business risk list for mining and metals companies globally, up from number eight in 2012. These capital dilemmas are strategic risks that threaten the long-term growth prospects of the larger miners at one end of the sector, and the short-term survival of cash strapped juniors at the other end.

Risk 1a — Majors learning to balance shareholder demands with long-term growth strategies

For larger miners, the rapid decline in commodity prices in 2012, rampant cost inflation and falling returns have created a mismatch between miners’ long-term investment horizons and the short-term return horizon of new yield-hungry shareholders in the sector.

Many years of high growth in earnings, cash flows and capital appreciation have attracted a different group of investors to mining. These investors have short-term investment horizons and are not as comfortable with the sector’s cyclical nature and its longer-term and often counter cyclical development, investment and return horizon. This raises the question of how to balance the demands of short-term shareholders with those investing for longer-term returns.

There is a profound risk that the decisions taken by mining and metals companies today could damage their growth prospects, destroying shareholder value over the longer term.

Risk 1b — Junior miners fight for survival

The dilemma for junior miners could not be more different. The dramatic and continuing sell-off in equity markets has starved the junior end of the market of capital at levels we have not seen in 10 years. Advanced juniors and mid-tier producers have been caught in the middle, exposed to a fragile balancing act between investors’ thirst for yield and low tolerance of risk.

The cash and working capital position of the industry’s smallest companies underlines the severity of the situation. Companies with a market value of less than US$2 million — about 20% of listed mining companies across the main junior exchanges — had on average less than US$1 million in cash and equivalents on their balance sheets at 31 December 2012.

Risk 2 — Margin protection and productivity improvement

A decade of higher prices has concealed the impact of rampant inflation, falling productivity and poor capital discipline in the sector. In 2012, the softening of commodity prices in an environment of escalating costs had a major impact on bottom lines, resulting in significant impairments and derating of company stock prices. A weak external environment and the lack of investor confi dence have heralded an industry-wide directional change from growth for growth’s sake towards long-term optimization of operating costs and capital allocation.

Some of the factors squeezing margins, such as scarcity premiums for inputs or high producer currencies, will ultimately

self-correct as mineral prices fall. However, high costs will continue to take a toll on company margins until companies address the longer-term optimization of operating costs and capital allocation. While the market has been rewarding any cost decreases, those that improve long-term value by being embedded and sustainable will prove the most valuable.

Alongside this, productivity in the sector has been on the decline for nearly a decade, across manpower, equipment, processes and logistics. This has significantly impacted the sector’s input to output ratio. Those who have tackled margin protection early are increasingly turning their focus towards optimizing productivity through their capital structure, and more judicious use of labor and equipment. These companies are also focused on using innovation as a means of enhancing productivity. The increased digitization of mines also means that firms can better monitor and analyze processes in order to understand why productivity is falling and to identify and employ better practices.

I profoundly disagree with only one statement. Big miners will not adversely affect their growth prospects by pulling projects. To understand why, consider the next few phases in this boom and bust cycle.

The first phase of the down cycle was falling prices. The second phase – that we are in now – is excuses, rationalisations, search for yield, productivity drives, capital starvation etc. The third phase (next year) will be price falls as oversupply outpaces productivity measures, wholesale shutdowns, junior bankruptcies, equity carnage and despair. The final phase will be the year after with accelerated consolidation, the appearance of vulture capital, mergers and takeovers of the weak by the strong. The year after that we might settle into some kind of long term price stability, decent yields and steady equity returns.

Advertisement

It’s not that the boom was a bubble even. This is just the way mining cycles work. It’s very difficult to match highly capital intensive long germ projects to the fluctuations in demand. We’ve overdone it this time as China slows and now prices must fall enough to take out some production.

I might have my timing wrong here but I’m sure you get the idea. The majors need only pump product, sit and wait. Their next round of expansions are already being built and will be available for purchase at steep discounts shortly. Full report below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.