The combination of the rising US dollar and slower Chinese growth, leading to a fall in Australia’s terms of trade – the iron ore spot price has already fallen 31 per cent since mid February – could see a rapid depreciation of the Australian dollar in the months ahead.

That would be great for the competitiveness of Australian manufacturing but a falling currency and terms of trade also leads to a decline in national income. Input prices rise and government revenue falls.

This is back-to-front. A falling dollar does not impact the terms-of-trade, which broadly measures the quantity of imports that can be purchased by a givenquantity of exports. Australia’s incomes surged from 2003 onwards because the price of the goods that we export – namely iron ore, coal, gold and LNG – surged relative to the cost of the things we import. As such, Australian’s real disposable incomes rose inexorably since, as a nation, our purchasing power rose.

A falling dollar, on its own, is independant from the terms-of-trade and does not change this equation. If, for example, the Australian dollar fell to say 60 cents, the cost of our imports in Australian dollars would rise dramatically. However, at the same time, the Australian dollar value of our exports (which are typically priced in US dollars) would also rise by the same amount, leaving the terms-of-trade and national incomes broadly unchanged.

Government revenue may also benefit from a falling dollar as profits to exporters rise, increasing company taxes, as well as via greater spending domestically (think increased domestic tourism).

Kohler goes on:

In 1986, when the Australian dollar fell below US50c, the nation was forced to embark on two decades of microeconomic reform to boost productivity, as well as deliberately cause a recession in 1991 to reduce inflation.

The main reason Australia has not had a recession for 20 years is not the direct impact China, but the fact that the rising dollar has kept inflation between 2 per cent and 3 per cent for most of the time, allowing the real cash rate to trend down since 1994.

A depreciation of the currency now would end Australia’s unbroken 22-year record of economic growth as night follows day.

It would also force a return to difficult microeconomic reforms to boot productivity. With rising terms of trade and exchange rates, the only source of rising national income would be productivity.

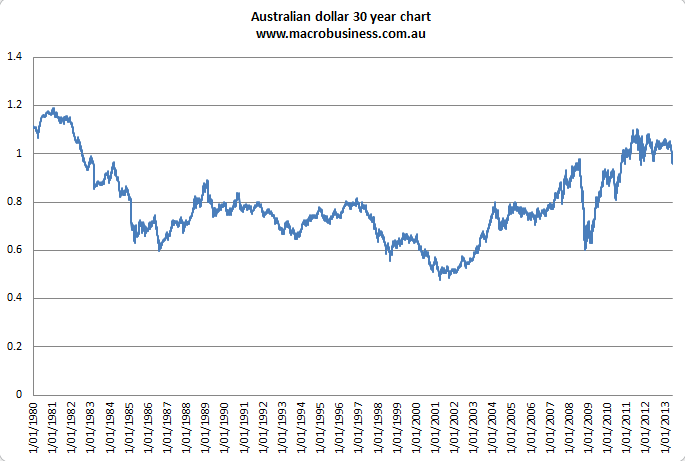

Errr, the dollar never fell below 50 cents in the 1980s. Or the 1990s for that matter. For one day in July 1986 it fell to 59.8 cents but through most of that year it was closer to 70 cents and by 1989 it was 90 cents:

That is not to say the dollar played no part in Australia’s late eighties inflationary surge, which was also the result of freshly privatised banks lending their butt’s off.

But to claim that a high dollar has enabled the cash rate to fall ever since ignores the nineties in which the dollar was below 80 cents the entire time, not to mention the four year period from 1998 to 2002 when the dollar was under 60 cents and as low as 45 cents.

While I agree that productivity reform is required, the falling dollar also helps to an extent. As for China playing no part in Australia’s unbroken run of growth, that doesn’t pass the laugh test.

The falling dollar will cause tradable inflation to rise (40% of the CPI basket) and if the RBA overreacts may presage recession. But it could just easily (should and will) look through the inflation surge (if it is not offset by declines in non-tradable inflation).

It will be up to government to prevent it spilling into wages and becoming self-fulfilling if it comes to that.