Two opposing views on the iron ore price are offered today by Credit Suisse and Goldman Sachs. CS remains bearish:

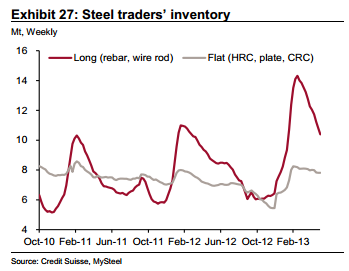

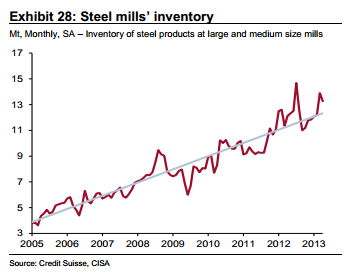

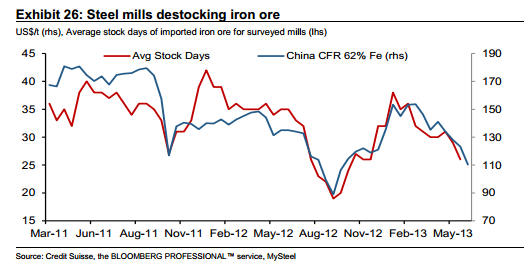

Much of the recent decline appears linked to a reduction in mills’ iron ore inventories (Exhibit 26), albeit port stocks are now rising. Given the apparent overhang of steel stocks in both the hands of traders (Exhibit 27) and mills themselves (Exhibit 28), we see little reason for them to bid the market higher to replenish these volumes.

Indeed, we hold to the view that raw steel production run rates will slow through the remainder of the year (see, for example, Iron Ore Under Pressure). Consequently, mills will need to hold fewer tonnes of iron ore in order to meet the same inventory cover for pig iron production. Prices, in our view, therefore have a lot more downside before the inventory cycle can come into play as a bullish argument.

Moreover, as forecast in April (The Setting of the Sun), we believe the market will move into seaborne surplus over the course of Q3, led by Rio beginning to ramp up from nameplate capacity of 237 Mt/y to 290 Mt/y for its Pilbara operations.

This changing dynamic should further enable mills to maintain comfortable levels of inventory without tightening the market.

Could not have put that better myself. Meanwhile, Goldman Sachs is still working on the presumption that mills have not yet changed their inventory management for good:

Advertisement

The current cycle of falling iron ore prices is unfolding against a backdrop of weak steel prices and deteriorating margins in the Chinese steel sector; this has forced mills to reduce costs further and triggered another round of destocking. In terms of the price trajectory to date, the current downturn is similar to the price correction in 2H 2012 which saw a ~$30/t drop over a 7 week period and lasted 132 trading days below our US$140/t estimate of cost support. Both, in our view, are indicative of the shifting balance of power from iron ore producers to consumers.

However, inventories at Chinese ports and at small/medium mills are already at levels similar to those reached at the bottom of the previous destocking cycle. On that basis we believe that the downside risk from further destocking is somewhat limited.

Seaborne iron ore prices have already overshot on the downside

Following the recent decline, seaborne iron ore prices (down 20% ytd) have overshot relative to domestic iron concentrate (down 6%) and to Chinese steel (down 6% and 12% for rebar and HRC respectively). As a result, the price differential is in favour of imports by a margin of ~US$18/t.

Meanwhile, lower iron ore and metallurgical coal costs will result in lower operating costs for steel mills, which would provide some temporary respite to loss-making mills.

In a market driven by buyer sentiment, we find it difficult to forecast short term moves. However, we do expect a shorter, less severe downturn relative to 2H 2012 and we maintain our positive outlook for 2H 2013 (GS forecast US$133/t CFR China) even as the period of oversupply draws ever closer.

Forget Chinese port stocks, they’re not going to rebound. Having said that, I’d be surprised if mills didn’t restock some as prices fell but nothing like what we experienced earlier this year, which was clearly an error. So I guess I’m somewhere between these two arguments, expecting an ongoing battle between destocking in steel and iron ore to push the price up and down for the next quarter probably between $100 and $120. Then a non-stop grind lower to $80 into next year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.