Yesterday Goldman Sachs downgraded its Australian growth and dollar targets on rising recession risk:

Australian economic growth forecast to be sub 2% in 2014

Following the release of 1Q13 economic growth data for Australia and some weaker more timely reads on economic activity in Australia we are lowering our 2013 economic growth forecasts from 2.4% to 2.0% and lowering our 2014 economic growth forecasts from 2.7% to 1.9%.

A$/US$ is now forecast to be 85c in 12 months time

We have also lowered our exchange rate forecast from a 12-month forecast of A$/US$0.90 to a 12-month target of A$/US$0.85. Our 3 and 6-month targets have also been lowered from 0.97 to 0.92 for the 3-month target and from 0.95 to 0.90 for the 6-month target.

Our probit model ascribes a 20% chance of recession

Australia’s high private investment share of GDP, its high real exchange rate, its falling terms of trade, its poor labour demand and slowing labour income dynamics, and a political environment that is unlikely to provide the cushioning role of fiscal policy into faltering private demand all suggest that the Australian economy remains at risk of tipping into a broader and deeper downturn.

Our base case remains that a recession will be avoided

While a recession in Australia is possible we believe there is still time for the economy to respond to the combination of better global growth, domestic policy stimulus, and a lower Australian dollar. Much will depend on the evolution of each of these forces over the coming months and importantly how quickly business and consumer sentiment responds.

And why are we at risk?

Advertisement

As we have stressed on numerous occasions over recent years, Australia is facing the dual forces of a sharp retracement in investment from historic highs and an external income shock via the deteriorating terms of trade trend…Policy makers have not been blind to these forces and have adjusted their policies, however, with the biggest adjustments in commodity prices and investment still yet to occur the concerning aspect is that policy makers are rapidly depleting their reserves with little discernible impact upon demand.

And the timing?

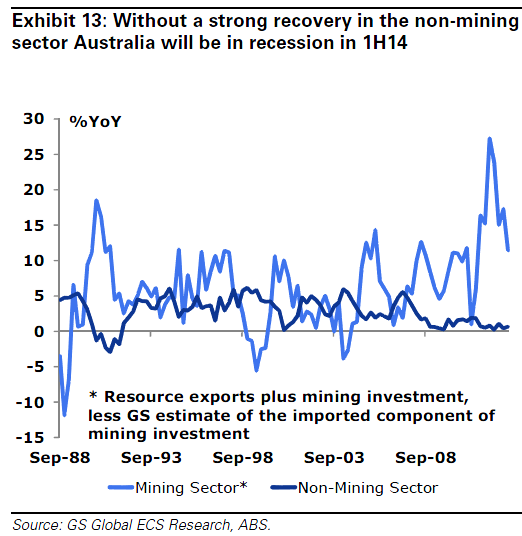

We continue to believe that the biggest risk period for the Australian economy is 1H14. This is where we estimate that the biggest declines in mining investment will occur, well before the forecast pick up in export volumes in 2H15. However, it is also where we forecast housing investment to be continuing to provide a positive catalyst for economic

growth.

Goldman has been macrobated. Yet it still sees the iron ore price averaging $115 in 2014. I see it between $80 and $90. If I’m right the recession risk is already much higher.

The bad news from Goldman did not stop there. From the Financial Times comes the above interview with Jim O’Neill, former chairman of Goldman Sachs Asset Management, discussing emerging markets and the outlook for the Chinese economy:

Advertisement

O’Neil is regarded as one of the world’s foremost experts on emerging markets, famously coining the term BRICs.

In the interview, O’Neil provides a fairly sober assessment of China’s growth prospects, describing lower growth as “a done deal” and arguing that big commodity exporters, particularly Australia, would be the biggest losers from the Chinese economy’s transition to both lower and consumption-based growth (away from investment-led growth).

By contrast, in a article published last month, O’Neill argued that China’s slowing economy would be a blessing for commodity importing countries, like the UK. As commodity prices fall, owing to both rising supplies and slowing Chinese demand, commodity importing nations would benefit greatly from improving terms-of-trade and higher disposable incomes.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.