We joke, we joke. A little. Deutsche had of course already joined the commodities-supercycle-is-dead chorus, and this note is not from the commodities side but by Asia chief economists Taimur Baig and Jun Ma.

Ma, who covers China, wrote an interesting and widely-read note about China’s pollution constraints earlier this year. This one however has some key capitulation moments for some of us. For example:

Advertisement

It was tempting to look at China’s high-growth track record (with little variation) as a sure-fire indication of robust demand to persist for years to come. Emergence of India, which also saw accelerating economic growth, was seen as another source of persistently sizeable demand.

The underwhelming realities of those calls are just part of their explanation for why the supercycle is over. The other reasons are: structurally declining demand in OECD countries; the fruits of investment in new production bringing prices lower; and the increase in shale gas and oil production further adding to supply.

We won’t go into Deutsche’s whole rationale on energy and soft commodities. Their energy production outlooks are rely on the standard forward looking stuff (EIA forecasts and the like) which seem too early to call, especially on shale. Baig and Ma are particularly optimistic on Chinese shale gas, and say the potential for the country to beat its targets should not be discounted. But there are technology hurdles, not to mention a lack of usable water where it’s most needed.

On the other hand, there is evidence that oil demand is in structural decline in the OECD, and perhaps even in emerging countries — at least relative to GDP, in the latter group.

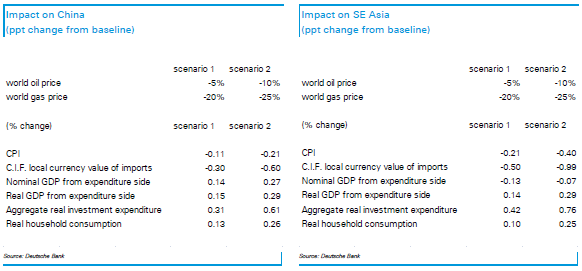

Anyway, here’s how Deutsche modeled some changes in gas and oil prices which they picked. The variation is from their standard ‘computable general equilibrium’ model:

Advertisement

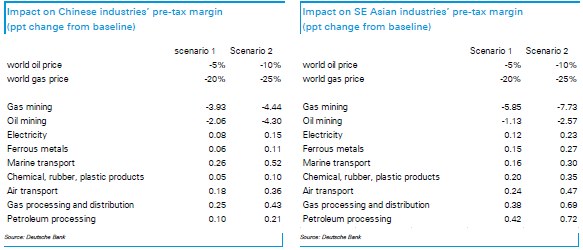

And corporations:

They haven’t modeled other commodities here, or Japan, which is a shame. Though not so much for soft commodities, because can we really be sure the supercycle really over in those markets? Baig and Ma are somewhat mocking of arguments made in the past “that the world’s farm lands were reaching their full potential, and that climate change was going to create more frequent weather-related volatility and associated crop failures” — but little of that seems disproven yet. The FAO thinks China’s “consumption growth will slightly outpace its production growth” and sees feeding the country over the next decade as a “daunting task” given its demand relative to internationally traded markets for food stuffs.

Advertisement

However changes in the supply/demand dynamics for metals, coal and iron ore are much better established and their effects on Asia certainly will be interesting. Inflation in the importing countries, which is most of them, would be significantly affected:

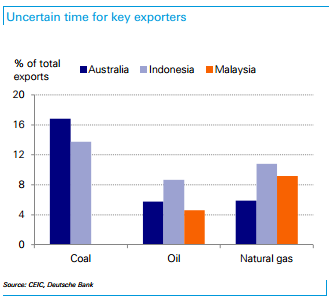

Most Asian economies are importers of energy, with Australia, Malaysia, and Indonesia three notable exceptions, but all are likely to be profoundly impacted by shale related developments. For a country like India, which spends nearly 40% of its total import bill on coal and oil, and runs a large current account deficit, energy price stability or decline would bring significant dividends in terms of external stability and domestic disinflationary dynamic. For Japan, lower energy pricing, combined with access to cheaper LNG imports from the US, could provide a significant boost for an economy that was left increasingly exposed to energy costs following the Fukushima disaster (as imported power fuel has been used to offset the loss of nuclear power).

On the other hand: for the exporters of coal in particular, perhaps not so much:

Advertisement

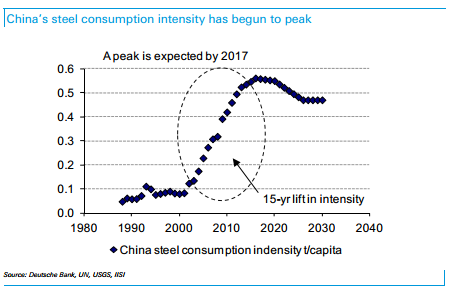

To finish up, here’s a cute bit on steel consumption demand:

Once a source of seemingly insatiable demand for iron ore, China’s demand has begun to wane, and will likely remain so as we believe the economy’s steel consumption intensity is beginning to peak, just as it had for Japan when it went through a 15-year cycle of industrialisation:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.