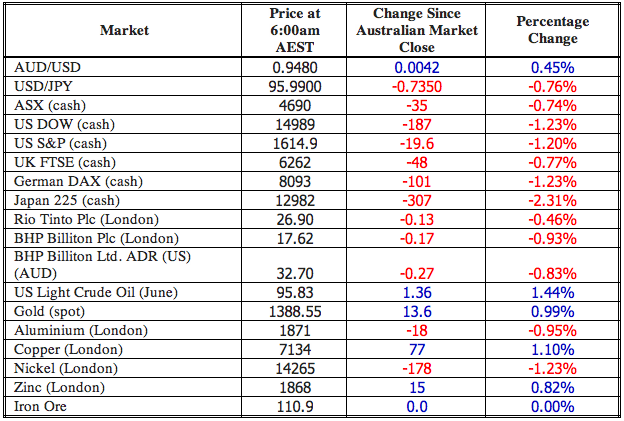

Having some technical issues today. Below is an IG table with iron ore at the bottom. Still no change on Chinese holidays.

ANZ is out suggesting a short term bounce may be in the offing. That’s a brave call given the deteriorating context but the overall assessment is useful:

Bulk markets look oversold, but face the headwinds of the passing in stronger seasonal demand. Chinese manufacturing activity tends to dip in June/July and destocking of bulk inventories starts to kick-in. That said, the downside risks may have already been factored-in, with heavy shorting of Chinese steel prices in late May. The supply-side looks mixed, with a tighter backdrop for iron ore (particularly inventories) contrasting with more ample supply in coal.

Iron ore is a trade off between weak China data flow and bottom fishing by Chinese consumers. The sharp 14% decline in April was a precautionary reaction to heavy shorting in Chinese steel prices over the same period – but the moves looks exaggerated. The risk is any positive Chinese data should squeeze steel shorts and trigger a relief rally in iron ore. A mild pick-up in Baltic Capesize rates since the start of June may also be suggesting that Chinese traders like the iron ore price entry level. That said, we think we import activity could be muted, with traders unable to access sufficient credit lines from overly cautious domestic banks.

Like iron ore, coking coal looks oversold, but needs stronger Chinese steel prices to get it out of its funk. The supply dynamic looks less favourable and is unlikely to improve while higher availability of Chinese coal output and inflated coal stockpiles prevail. The closure of high-cost Australian supply would help, although most producers appear hesitant to curtail output, while stringent (take-or-pay) access fees to port and rail infrastructure apply.

Seaborne thermal coal will continue to be dogged by weak Chinese coal prices. A combination of soft domestic demand and high domestic coal supply means Chinese coal consumers have become very price sensitive. The recent reports of a proposed Chinese ban on low quality thermal coal imports is unlikely to prop-up prices in the near term, with still low visibility on the actual ban and ample back-up supply. Like coking coal, an inelastic supply response from Australian coal producers is not helping a price recovery.

Advertisement

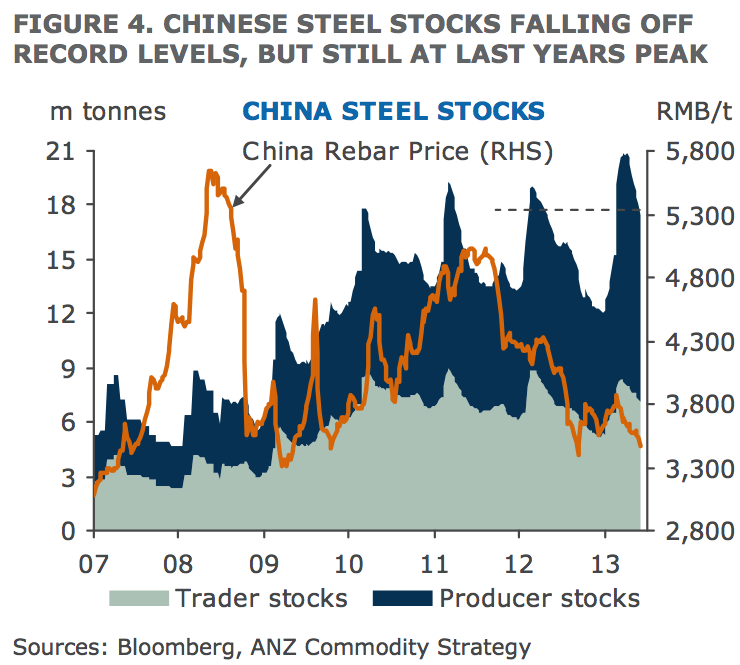

Those China steel stocks are still epic. Big production cuts ahead. Full report below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.