The AFR is happily pumping the Macquarie Bank view of equities today:

It had to happen some time. Or, that is, it had to keep happening. Tanya Branwhite continues to tweak Macquarie’s recommended Australian portfolio away from yield and toward growth.

And to underline the point, the broker has reduced its exposure to Telstra, and increased its weighting toward BHP Billiton. The portfolio still retains an overweight exposure to Telsta, while the increase in BHP trims the underweight position toward mining.

Tanya says there’s increasing “relative downside risk to the yield theme”. She’s been pointing towards this maturation in recent notes.

Macquarie has been underweight mining since mid-2012 on a view China’s “slowing demand growth would leave the commodity price complex closer to ‘equilibrium’ and that the stronger for longer cycle experienced over the last decade was over.”

The implications of that step-change are now priced in, Tanya says.

One key thing to note is the Macquarie’s call on BHP is primarily a bottom-up one. Management is now focused on both labour and capital productivity. If that is done well, it should drive significantly higher profit margins and free cash flow. And there’s also that deep-seated hope in the market that sales of non-core assets could mean rising income distributions to shareholders.

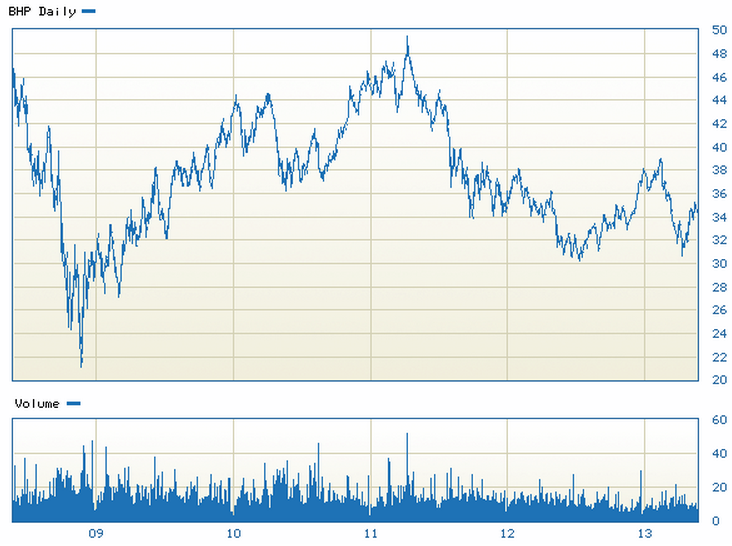

This is not a bad argument. And BHP is off its recent lows on this kind of thinking. The big miner now has a grossed up dividend around 5%:

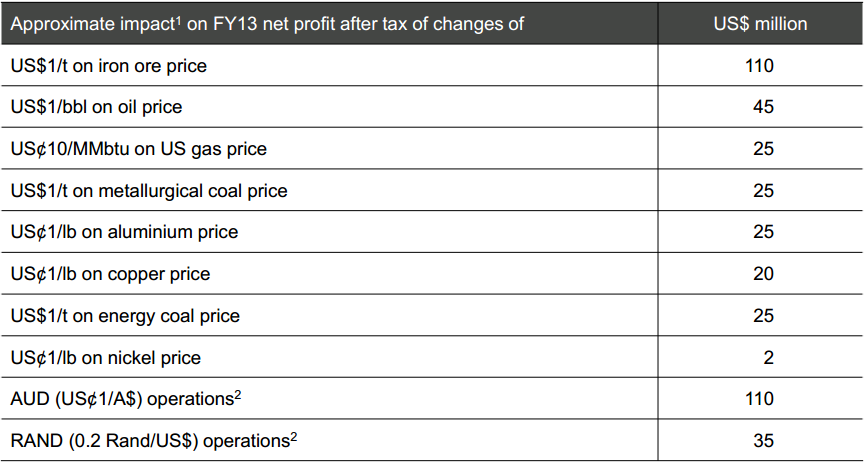

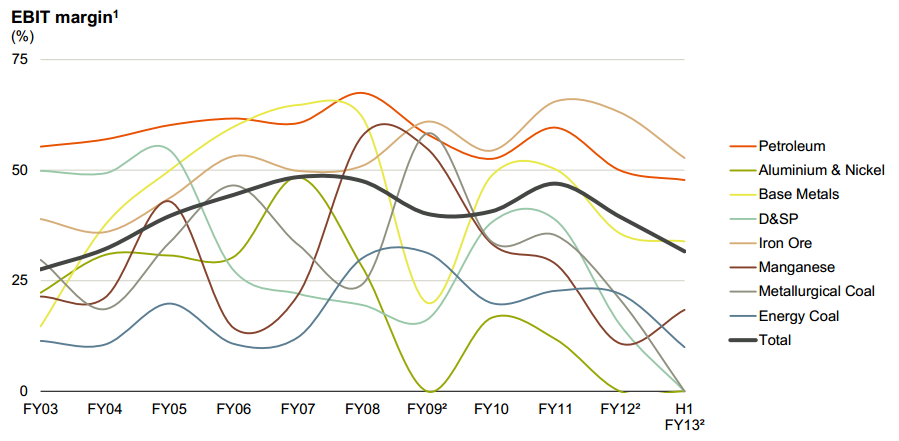

But the arguments are not persuasive enough. Look at these two charts from BHP’s last interim report:

Making our maths extraordinarily easy, take a look at lines one and nine. As you can see, every $1 move in the iron ore price reduces BHP’s profit by an impressive $110 million. At the same time, every 1 cent fall in the Australian dollar versus the US dollar increases BHP total earnings by $110. (As a quick aside, marvel at the margins here and explain how no rent tax was ever applied!).

So, if you’re looking at BHP right now, you need to ask, will the dollar fall faster than iron ore?

My view is that iron ore will level out somewhere near $80 next year so from here that’s a fall of 35%. Clearly the dollar will need to be at 60 cents to offset that drag. That’s possible but not as fast as the iron ore price falls is my bet. At best, BHP’s mix of assets is not dollar hedged owing to its iron ore exposure.

There are better ways to play the coming shift in economic circumstances.