The RBA’s May Statement of Monetary Policy is out and those looking for concrete answers to this week’s rate cut will be disappointed. There is not much more to go on than that offered in the statement following the meeting:

Over 2012, the Board reduced the cash rate by 125 basis points, bringing it to 3 per cent and borrowing rates close to their previous lows. Since then, signs have emerged that the economy has been responding to the low level of interest rates. Savers have been changing their portfolios towards assets with higher expected returns, asset values have risen and some interest-sensitive areas of spending have increased. On the other hand, the exchange rate has been little changed at a historically high level over the past 18 months, which is unusual given the decline in export prices and interest rates during that time. Moreover, the demand for credit has thus far remained relatively subdued.

Over the earlier part of this year, the Board held the cash rate steady while carefully assessing economic developments and noting that the inflation outlook would afford scope to ease further, should that be necessary to support demand. At its May meeting, with inflation a little lower than had been expected, and growth of economic activity likely to remain below trend into next year, the Board judged that a further reduction in the cash rate would help to support sustainable growth in the economy, and would be consistent with achieving the inflation target. The Board will adjust the cash rate as appropriate to foster sustainable growth and low inflation.

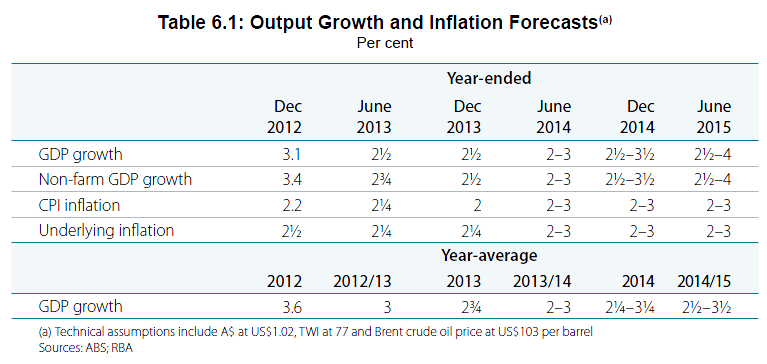

Below trend growth, dollar, supporting demand. If anything this is less vague than the statement following the meeting. The RBA did, however, cut its forecast for growth this year to 2.5% from 2-3% previously as well as rounding down all of its inflation figures. The bank slightly raised its 2015 growth forecast range for no apparent reason:

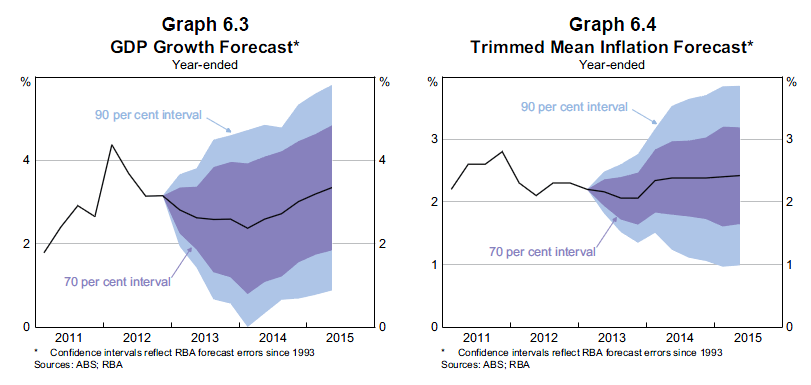

Here are its new paths for growth and inflation:

Oddly enough, I think the risks are tilted towards a growth blowoff in the March quarter on consumption and net exports, which will provide the usual suspects with an opportunity to dance on a pin head before growth weakens in the second half. Bit of a holding pattern this one. Dollar got a little lift.