Overnight, the Peterson Institute of International Economics (PIIE) released an interesting study exploring the hypothesis that high home ownership damages the labour market. The study, which is based on an examination of data from the US, found that rises in the rate of home ownership are a precursor to eventual sharp increases in unemployment in that state, due to:

- lower levels of labour mobility;

- greater commuting times; and

- fewer new businesses being formed.

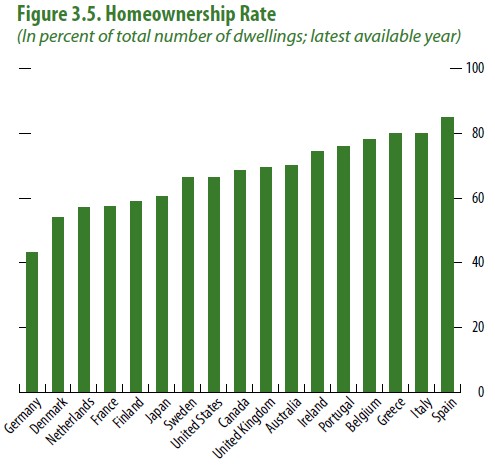

The study has potentially important implications for Australia, where home ownership rates are relatively high by international standards, according to the IMF (see next chart).

Current policy in Australia tends to favour home ownership over renting, possibly leading to ownership rates being higher than they otherwise would be. More importantly from an economic perspective, housing transaction costs – particularly stamp duties on property transfers – are high in Australia, which act as a road block to moving house, stifling labour mobility and increasing commuting times in the process.

Given these issues, there is merit in examining policies that strengthen the attractiveness of renting, such as instilling greater security of tenure, as well as shifting state government taxes away from inefficient and inequitable stamp duties towards broad-based land values taxes.