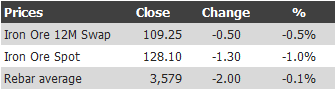

Find below the iron ore price table for May 14, 2013:

Looks like we’re going to test $120. I’m still not overly bearish. All of that Chinese credit growth has to support something!

In news today, the Australian Budget is slowly coming to terms with reality. From the AFR:

It may be this year’s single most important underlying budget assumption – that the price for Australian iron ore will average $110 a tonne in 2013-14 before falling 9 per cent the following year.

…According to the budget papers, iron ore prices – which are normally quoted on global markets in US dollars – will fall to $100 by June 2015 from about $120 tonne at the moment. Treasury’s forecasts are based on an Australian dollar of $US1.03.

…“Further increases in supply are expected to place downward pressure on prices over the forecast period,” the government said in the budget papers.

Prices for Australia’s second-most important bulk commodity exports – metallurgical and thermal coal – are expected to average about $180 a tonne and $75 a tonne respectively through the next two years.

Getting there and not too bad though still 10-20% too aggressive in my view. Thermal coal looks right but coking is currently trading at $145 for spot and there’s lots of new supply.

In other news, Rio’s Pilbara 360 project suddenly appears shaky:

Rio Tinto chief executive Sam Walsh has raised the prospect of slowing a $US5 billion Pilbara iron ore mine expansion following concerns from shareholders the miner was taking too aggressive an approach to expansion.

In a presentation at the Bank of America Merrill Lynch Global Metals, Mining & Steel conference in Barcelona on Tuesday, Mr Walsh appeared to soften his rhetoric when discussing long-held plans to boost iron ore production to 360 million tonnes a year by 2015.

“We have multiple pathways on the 360 mines,” Mr Walsh said. “The decisions will be made in late 2013 and in early 2014. Depending on the market, we could choose to develop new mines to quickly deliver tonnes. Or we could conserve cash and fill some capacity with incremental tonnes from existing mines at much lower capital intensity.”

It probably makes sense to delay even though Rio has already pissed way $10 billion on the associated rail and port infrastructure. This is good news for Fortescue too who will see its prospects lift a little with less supply planned.

Still, it’s all far too late. The combined $130 million tonnes of new Australian supply (without counting minnows), plus what looks like a return of Indian ore to 50 million tonnes in a similar time frame, is a glut coming into fading Chinese demand growth.

Massive aluminium and write downs and now iron ore over spend to weigh on return on equity. Seriously, if the commodity super cycle was a classroom paper you’d give Rio an “F”.