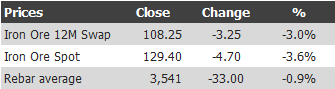

Find below the iron ore price table for May 2, 2013:

Here’s some texture from Reuters:

“Sentiment’s a bit bad. No one is looking to buy and there are plenty of offers in the spot market,” said a Singapore-based iron ore trader.

Two Australian cargoes are among those on offer — one is 165,000 tonnes of 61 percent grade Pilbara iron ore fines and the other is 70,000 tonnes of 57.7 percent grade Yandi fines, traders said.

Pilbara fines were last sold at around $138 per tonne and Yandi at about $124 before the Chinese went on a three-day holiday that ended on Wednesday, traders said. They expect the latest cargoes to fetch lower prices.

“Chinese mills are well stocked. They generally have over 20 days of (iron ore) inventory, so there’s no pressing need for them to buy spot now,” said the Singapore trader.

Benchmark 62 percent grade iron ore .IO62-CNI=SI was unchanged at 134.10 a tonne on Tuesday, according to data provider Steel Index. There was no price assessment on Wednesday due to a public holiday in Singapore.

There is some catch up here on the poor PMI data as Chinese markets were closed.

But I still think we’re going to march straight down to $120 here to retest the FMG price floor thesis. The spread between spot and the derivatives is far too wide for these price levels and demand conditions. It should $12-15 , not above twenty to the 12 month swap. On steel prices it’s even wider.

Of course, 12 month swaps are already signaling a major backwardation that is questioning the viability of FMG.

Following the recent credit surge, there is surely going to be a pick in Chinese growth in the second and third quarters. So I wouldn’t get too bearish yet for iron ore. But the Chinese steel mills massively overestimated their own cycle and now we have to give back as steel inventories fall.