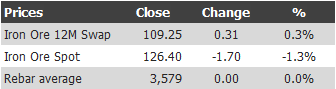

Find below the iron ore price table for May 15, 2013:

Rebar futures also sold off sharply.

Looks like we’re headed for a test of $120 “price floor” and charts would suggest $110 is the next support level.

Iron ore got some good news from analysts yesterday when Morgan Stanley argued that ore will remain strong throughput 2014. From Bloomberg:

Iron ore prices will remain strong into 2014 on sustained demand in China, the largest producer of steel, and as an increase in global supply takes longer than expected, according to Morgan Stanley.

While the price has averaged $135 a ton this quarter from $148 in the first three months, that’s more than the bank’s estimate of $130 for the April to June period, analysts Joel Crane andPeter Richardson wrote in a report dated yesterday. The bank maintained its forecasts of $120 in the first quarter of 2014 and $118 in the second.

…“It is increasingly clear that steel consumption in China remains strong,” Morgan Stanley’s Melbourne-based analysts wrote. “Our assessment of the global seaborne iron ore market is that price strength could continue well into next year.”

…“Market concerns over the sustainability of strong iron ore prices are focused on the prospect of an excess of supply coming to market in 2013 and 2014,” they said, referring to expansions such as Rio Tinto Group’s Pilbara operations. “While an increase in mine capacity is well understood in the market, the timetable of ramp-up into that capacity is not.”

Perhaps I’m missing something. But Rio’s Q3 release of 55 million tonnes of new capacity, FMG’s Q4 release of4 0 million tonne new capacity and BHP’s Q1/14 start date for 35 million tonne capacity seems pretty straight forward.

Bloomberg went on:

Another major cycle of stockpiles draw down is unlikely in the second half of 2013 because inventory levels across the value chain are too low, Goldman Sachs Group Inc. said in a report dated yesterday.

That’s certainly true. The big hoard has been used up. Though I suggest that if Chinese demand weakens again we might still find it can fall further. The GFC stockpile was much smaller but the inventory cycle still massive. Moreover, as China seeks to dampen the real estate cycle, Q4 is a candidate for another stall.

Finally, back to MS:

India’s role as major supplier in the seaborne market is in “terminal decline” after mining was suspended in the states of Karnataka and Goa and exports were capped, the report said.

Well, that’s supposition. It looks to me like Indian ore will come back to market. Maybe not by Q4 this year but certainly in the first half of next. Simply put, India has a surplus of iron ore. It’s not going to sit on it.

I will add, finally, that as sophisticated as MS’ supply and demand models are, they have consistently overestimated the iron ore price.

I could very well be wrong in all of my arguments but there is little here to persuade me of it.