Woodside has confirmed this morning that Browse LNG is off. Yes, it is mumbling about alternative paths for development but is in no hurry to do anything it seems:

Woodside will immediately engage with the Browse Joint Venture to recommend evaluation of other development concepts to commercialise the Browse resources, which could include floating technologies, a pipeline to existing LNG facilities in the Pilbara or a smaller onshore option at the proposed Browse LNG Precinct near James Price Point. Woodside will propose to the Joint Venture a work program and budget for the remaining 20 months of the Retention Leases with a commitment to the timely development of the Browse resources.

It is worth recalling an analysis by NAB about what this means economically. The $43 billion Browse project was biggest of the planned mega-projects by a long way. The remaining list includes: Arrow LNG trains 1 & 2 for Gladstone $24 billion, Gorgon train 4 Barrow Island $12 billion; Scarborough Gas Off Onslow $12 billion and Sunrise Gas Off Darwin $12 billion.

Of these, Browse is now shelved, Arrow is considered unlikely to proceed as anything other than a reduced and merged project. Scarborough is FLNG, so far as I know Sunrise is embroiled in disputes with East Timor. Gorgon train 4 may be the most likely to proceed.

Advertisement

In short, the boom is winding down, one way or another. Here’s how NAB described such an outcome:

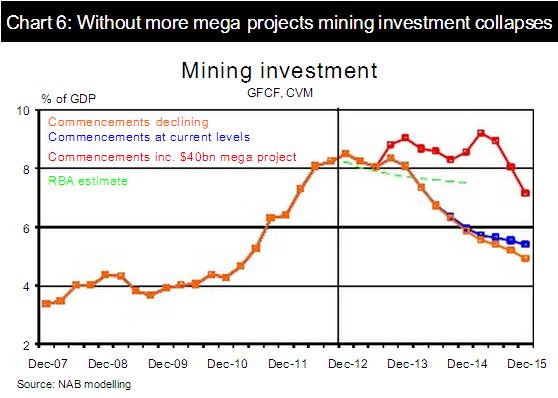

Translating these forecasts into financial year numbers implies a year-average increase of 20% in mining investment in 2012/13 (mostly reflecting the run-up thathas already occurred) but a decline of 6% in 2013/14 and a more serious fall of 21% in 2014/15. This is sufficient to reduce mininginvestment from an estimated peak of 8.5% of GDP in 2012Q4 to8.1% in 2013Q4 and then to 6.0% in 2014Q4. The decline through 2014 would be equivalent to removing more than 2 percentage points from GDP growth in that year.The commencement of another mega LNG project would alter these atmospheric: for example, a mega project arbitrarily commencing in 2013Q1 with an indicative construction cost of $40 billion, would be sufficient to maintain mining investment into 2014, possibly delaying the decline until late 2015, that is, by 18months. The RBA prediction for mining investment looks to besomewhere between these two scenarios.

What is interesting about this analysis is the potential for mining investment to decline precipitously once existing projects have been completed. This “mining cliff” could appear as early as the first quarter of 2014. The commencement of new mega projects could delay the cliff for 18 months or longer. On the other hand, a decline in commencements in response to declining commodity prices and rising costs is unlikely to affect mining investment until well into 2015 in view of the typical gestation period for projects. Any sharp decline in mining investment in 2014 would be highly detrimental to growth without an offset. Some of that will come from increased mining exports as new projects continue to come on stream. However, employment is likely to struggle unless non-mining investment fills the breach.

Even with some margin for error, that’s a big growth hole. And I still expect China to slow into the end of the year and the terms of trade to fall.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.