Chalk up another one for MB. For the past two years we’ve forecast that there will be no return to surplus for the Australian budget ever again. And now the world is waking up in a rush.

Over the weekend Tony Abbott ended the Coalition’s commitment to a public surplus for the its first year in office and probably for all time. From the AFR:

Opposition Leader Tony Abbott has declared “all bets are off” on whether the Coalition will deliver a surplus in what could be its first year in office, prompting warnings from a prominent economist that the budget may not be balanced for years.

The Gillard government seized on the shift to accuse the Coalition of “crab walking” away from a promise to deliver a surplus in its first year in office after pummelling the government for never posting a surplus.

“This is despite the Coalition telling Australians repeatedly that they will deliver a surplus, even after the government had flagged that doing so would risk jobs and growth,” Assistant Treasurer David Bradbury said.

“The hypocrisy from Tony Abbott about the surplus is extraordinary.”

Asked at a public meeting in Melbourne when the Coalition would deliver its surplus, Mr Abbott said he had previously been confident about the timing based on government figures as they stood just before Christmas. He indicated he had changed position because the government wouldn’t reveal the budget’s true state.

“But all bets are off given that the government won’t tell us what the deficit will be,” he said.

…Mr Abbott said: “We are confident that we will, at all times, deliver more prudent and responsible financial management than the current government because it’s in our DNA to deliver surpluses and pay back debt. Just look at what the Howard government did.”

Advertisement

Sensible choice from Abbott, economically and politically. Politics 101 at work here. Break your promise, blame the other guys. Not that it matters given Wayne Swan’s impeccably bad timing has led him to declare today:

…that the budget will not return to surplus until tax collections recover from a strong dollar “sledgehammer” that he said pushed revenues $7.5 billion below official forecasts for this financial year.

Mr Swan said the revenue write-down would occur across the four-year budget forecasts, putting at risk the $6.4 billion surplus which the government’s mid-year budget update in October projected for 2015-16.

But he suggested the government would not seek to offset the revenue write-down with spending cuts, instead allowing the so-called “automatic stabilisers” to work and weaker revenue to flow through to the bottom line.

The government would be “taking the responsible course in fiscal policy that when revenue returns then we come back to surplus,” Mr Swan said.

“If you’ve got this hit to revenue we shouldn’t be seeking to make up for it by savage cuts across the budget.”

No, you shouldn’t. Not when you’re headed off an investment cliff. And Swan’s solution is good news. At least we now know that when we fall off the mining investment cliff later this year that fiscal policy won’t be pro-cyclical. But it does not look like it will be very anti-cyclical either, which is what what will actually be needed for any decent growth outcome. So both parties have now committed themselves to an at best outcome of a low growth economy for the foreseeable future.

Advertisement

Meanwhile, the Grattan Institute is now forecasting deficits to eternity, From The Conversation:

Structural changes in the economy are likely to leave Governments across Australia facing budget deficits of around 4% of GDP for at least the next decade, according to research released today.

The Grattan Institute paper, Budget Pressures on Australian Governments, suggests it could be a long time before Australian governments post a collective surplus.

While the budgets of the Commonwealth and the states are forecast to be close to balanced within the next few years, our research shows flagging revenues and continued spending pressures have put them on track to post annual deficits of around 4% of GDP within a decade.

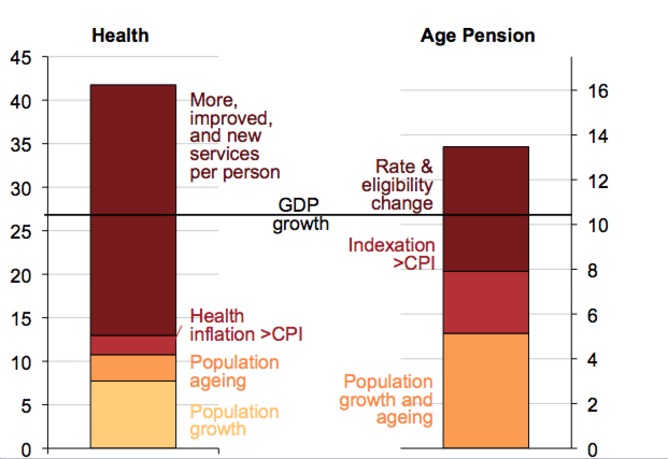

The greatest pressure comes from sustained increases in health spending. Over the past decade, in real terms, governments spent an additional $43 billion on health. At this rate, government spending on health will rise by 2% of GDP over the next decade. Contrary to popular belief, this is not primarily because of the ageing population but is driven by changes to the practice of medicine. Australians of all ages are seeing doctors more often, having more tests and operations, and taking more prescription drugs. They are living longer, better lives, but someone has to pay for it.

Spending on school education also rose substantially in real terms, although to date it has done little to improve student performance. Welfare expenditure grew more slowly, but only because of low unemployment and slow growth in benefits for Newstart, Youth Allowance and parenting payments. The other three large categories of welfare spending – aged and disability pensions and family support – all grew by around 50% in real terms over the last decade.

As with health, demography is not the major driver of increased aged pension spending. Most of the growth above GDP resulted from government policy choices to increase pension benefits.

Real increases in government spending 2003 to 2013 (2013 $ billions)

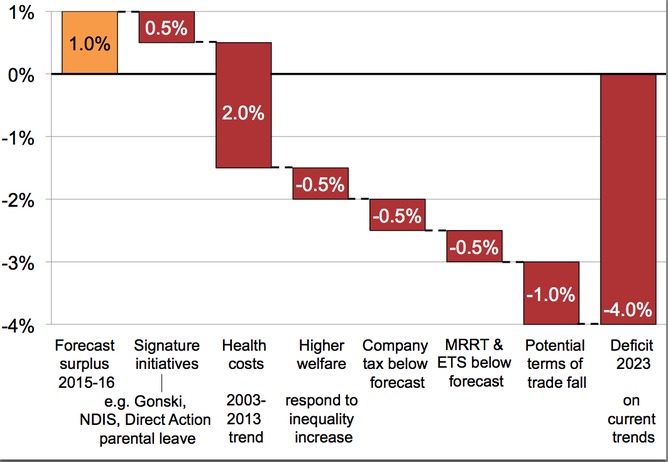

If these trends continue, they will increase welfare expenditures by another 0.5% of GDP. Welfare spending could also grow if the end of the mining boom brings an increase in inequality and an end to rising real incomes. Overseas these have led to increased pressure for welfare payments.

Increases in costs are not the only pressures on government budgets. Underlying revenues are weaker than they seem. Company and mining taxes, and carbon price revenues are likely to be 1% of GDP – or $15 billion a year – less than current forecasts. Current revenues are also inflated by the mining boom and Australia’s high terms of trade. If, as many predict, minerals prices fall, revenues will fall by another 1% of GDP.

Finally, the federal government and opposition have both raised expectations of substantial new expenditures on the National Disability Insurance Scheme, schools, additional paid parental leave, and carbon Direct Action, among other policies. Even a subset of these could well cost 0.5% of GDP.

Over the economic cycle of boom and bust, balanced budgets are much better than the alternative. Persistent government deficits incur interest payments, limit future borrowings and, as many European countries are learning, drastically reduce the capacity to fund services and programs. Deficits can make it hard for governments to spend to overcome an economic crisis, and can load a debt burden onto future generations. Given all the problems persistent deficits cause, why do they exist? Very often, the answer is politics.

Governments invariably find it hard to run a surplus, even in good times. The temptation to please voters and spend money is just too great. In Australia, voters have come to expect policies that leave no losers.

With these pressures, responsible leaders will need to find 4% of GDP in savings and tax increases to balance their books by 2023, That will require governments to make savings and increase taxes to the tune of $60 billion a year in today’s terms. How can they do this and is it likely?

The signs aren’t good. At a forum organised by the Australian Financial Review late last week, shadow treasurer Joe Hockey — who pledged in January that a Coalition government would deliver a first-term surplus — acknowledged that such an outcome would be unlikely. Instead Hockey emphasised the importance of being prudent. “We’re not going to go down the path of austerity simply to bring the budget back to surplus because it would end up being a temporary surplus depending on how big the deficit is that we inherit,“ he said.

Potential deficit of Australian governments (percent of GDP)

Smaller government is not necessarily the answer. Australian government spending as a proportion of GDP – 34% – is low by OECD standards. Globally, there are big governments that run surpluses and small ones that are persistently in deficit. While increasing productivity and participation are good ideas, they are also unlikely to solve the problem.

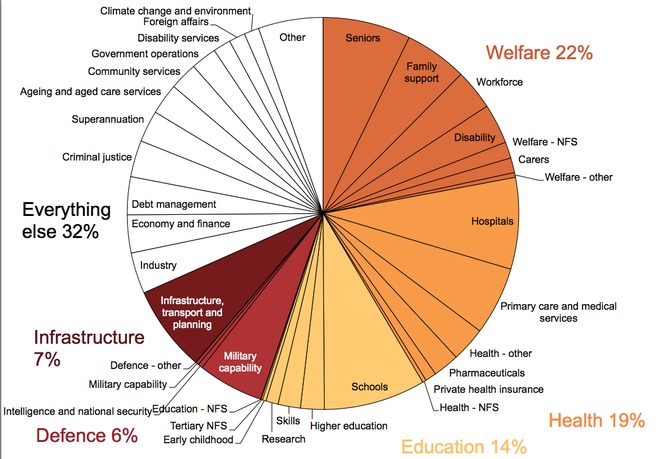

We will have to leave more options on the table. Health, education, welfare, defence and transport account for more than two thirds of government revenue.

Commonwealth, state and territory governments expenditure by policy area, 2012-13

To retrieve a budget deficit equivalent to 12% of government spending, cuts to some (or all) of these areas are inevitable. We cannot afford – as the Gonski reforms are suggesting – to guarantee continued growth in education spending without searching for efficiencies. Similarly, we will need to look harder at how health services can be delivered at lower cost.

History suggests that the only way to improve budgets is through tough policy choices. That does not mean politicians have to slash and burn. But they do have to change political culture.

Over the last decade, governments have tended to “buy” reform, accompanying any budget pain with a budget gain. The GST, the carbon pricing reforms, and school funding all came with promises that all but the wealthiest would be “no worse off”. In a decade of rising government revenue, exceptional economic growth, and rising prices for Australian minerals, governments could afford this approach.

The future will be more difficult. Clawing back a budget deficit of 4% of GDP requires that everyone bears some budget pain. Governments will have to sell this message. This will be politically difficult, but the alternative is unsustainable: budget deficits that will be even more painful to reverse in the future.

Australia’s strong economy gives our governments more options than many of their overseas counterparts. But they need to explain to the public why balanced budgets matter, for our current prosperity and that of future generations. Everyone will need to give up something. Which brave leaders will step forward?

“Australia’s strong economy” is a cliche undermined by the article itself. The economy’s strength was based upon a cyclical chimera of temporary income born high commodity prices. That we saw it as anything else was a big mistake.

Advertisement

On Friday Moody’s also said:

Global ratings agency Moody’s Investors Service said on Friday its outlook for Australia’s AAA credit rating was stable and the risk of a downgrade was “relatively low” despite the budget remaining in deficit for longer than targeted.

Moody’s senior vice-president Steven Hess told Weekend AFR the high dollar threatened the budget.

“If the exchange rate does not adjust, the end of the investment boom in mining and lower commodity prices – if they materialise – could mean that growth will be below its recent pace in the coming few years,” he said.

“This is only a risk at this point, and not a forecast. Nonetheless, such a scenario would mean the government’s achieving a budget surplus would be more difficult.”

I am prepared to bet that the dollar will adjust but growth will still be poor and the incoming Coalition government will lose the AAA rating in its first two years of office. Prepare accordingly, banks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.