Deutsche argue today we’ll see short term strength in iron ore:

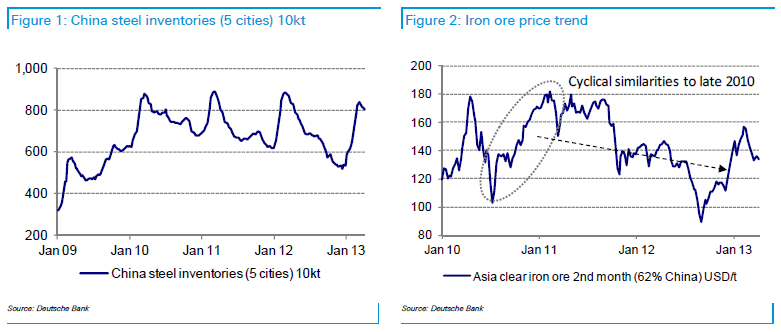

Iron ore markets continue to appear relatively buoyant with May contracts trading comfortably in the mid-130’s; the raw materials’ performance has mirrored that of spot steel prices in China which themselves have recovered by about 3% over the past week. While the broad inventory indicators for Chinese steel seem to indicate that stocks have peaked, we expect that at the local level, positive inventory adjustments are still taking place. Furthermore we also understand that some fabricator/manufacturing re-stocking is also taking place within the country and this may prolong the price support, possibly into May. While we anticipate that the iron ore market may be range-bound over the next month (between USD130-140/t) we would take advantage of pricing at the higher end of this range and sell into strength (the August contract may be an attractive short if it gets to USD130/t for instance). Given the expected increase in seaborne supply from the major suppliers in Q2, combined with some seasonal slowdown in orders heading into summer, spot iron prices could weaken towards USD110/t by mid-year.

Sounds plausible.

Meanwhile, ANZ see short term weakness in thermal coal and more cancelled projects:

Iron ore prices continued to rise, posting modest gains and consistent with the near 2% gain in Chinese rebar futures so far this week. Capesize freight rates are also showing better signs, up 2% in the last week after a 6% decline in the last month. China’s March 2013 iron ore imports were strong at 65 million tonnes, up 3% y/y. However across the quarter, China’s iron ore imports were flat at 186 million tonnes. In Australia, the reassessment of projects from depressed thermal coal prices continues. Port Waratah Coal Services has been planning to build a fourth Newcastle coal terminal, but announced yesterday it may not proceed or at best be delayed another two years (to 2018) from previous guidance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.