Euro traders in early Asia are at it again with the swearing in of the new Italian Government led by a bloke most Italian’s don’t even know, Enrico Letta. The team he has put together after being tapped on the shoulder last week by the aging Italian President is a grand coalition of his centre left party and Silvio Berlusconi’s centre right party. Strange bedfellows but then politics is about power and you can’t really do much without being in a position of exercising it.

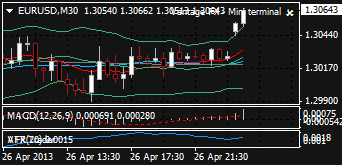

You can see this morning’s move in the chart above and whether or not it is a sustainable coalition or whether we are back to the bad old days of six month terms for Italian governments only time will tell but the euro’s little rally on this when it didn’t care about the enduring political impasse for much of the past couple of months feel more like early Asian stop running than anything else particularly.

Perhaps it was also the weaker than expected US data which helped euro push a little higher Friday with the USD Q1 GDP missing by 0.5% annualised printing just 2.5% against expectations of a 3% run rate.

It is worth noting given the above that we are still running a discretionary – not systemised – short position in euro and will do for some time. I thought it might have broken down and headed lower by now but it hasn’t and consequently the box between 1.30/32 is reinforced for the moment.

For the Aussie the outlook is starting to turn on both a fundamental and technical outlook. We will address the Aussie in a separate piece later but for now while below 1.0338/41 the bias is back toward the recent lows at 1.0219 and then perhaps lower. Looking at the chart above, some might make the case that if the recent lows hold and the Aussie breaks up through the trendline then it is off to the races again for a run at 1.04 and above. So that 1.0338/41 level is worth watching.

For USDJPY there are signs that the work of the yen weakness is done with the BoJ saying they expect the inflation outlook to be 1.9% in 2015. That is not far off their target and suggests that the overnment and the BoJ think that the policies they have in place will work. I don’t think that USDJPY is going to rally back into the 80’s at the moment but perhaps some of the topside pressure has dissipated for the moment.

The daily chat is starting to look like it is topping but like the aborted sell off below 96 recently we’d argue that only a break of the slow moving average which comes in at 97.12 today and coincides with the 38.2% retracement of the recent rally is the key short term technical level and support.

Turning to equities and commodities, at the close of play the Dow was up 0.08% but the Nasdaq and the S&P 500 both fell 0.33% and 0.2% respectively which given the magnitude of the miss, 2.5% outcome versus 3.0% expected, is really a testament to the impact of the free money culture that the Fed has created.

In Europe markets were also down with the FTSE off 0.26%, the DAX down 0.23% and the CAC fell 0.79%. In Milan and Madrid stocks fell 0.51% and 0.81% respectively.

On commodity markets gold spiked into our sell zone hitting a high of 1482 on Friday night before dropping back to close down 0.53% at $1453 oz. A break of $1450 could open a move lower today. On the silver market prices were under pressure falling 1.58% to $23.95 after an early rally also but Dr Copper managed to rally more than 2%. Crude was also down a little falling 0.68% to $92.78 Bbl.

Data

Japan is out today for “Showa Day” which an increasingly belligerent Shinzo Abe is calling something national return of sovereignty day. Nothing in Australia but a raft of European consumer confidence and business climate data before personal consumption and spending data in the US along with the release of Dallas Fed manufacturing data and pending home sales.

Twitter: Greg McKenna

Disclaimer: The content on this blog should not be taken as investment advice. All site content, including advertisements, shall not be construed as a recommendation, no matter how much it seems to make sense, to buy or sell any security or financial instrument, or to participate in any particular trading or investment strategy. Any action that you take as a result of information, analysis, or advertisement on this site is ultimately your responsibility and you should consult your investment or financial adviser before making any investments.