Over the past week, two separate reports have been released warning of an impending bursting of Hong Kong’s property bubble.

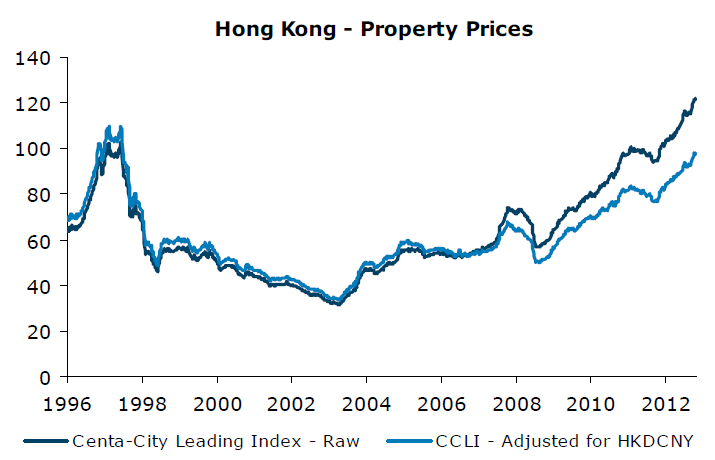

The first, by ANZ Bank (full report below), argues that Hong Kong housing is significantly overvalued following a 23% increase in prices over the past year, compared with economy-wide growth of only 1.4% (see below charts). And the growing divergence between actual and fair value places Hong Kong housing at risk of a severe price correction.

Advertisement

ANZ places much of the blame for Hong Kong’s bloated housing values on excessively low interest rates in the US (Hong Kong’s currency is pegged to the USD, hence, it must import US interest rates):

Undoubtedly, rising property prices since 2009 are largely driven by the negative real interest rate regime on the back of US monetary easing. At this stage, Hong Kong’s mortgage interest rates are priced at around 2%, and the low interest environment supports a large buy-rent gap for people who will need a property for self-occupancy as the interest portion of the monthly mortgage instalment is significantly below the monthly rental payment. This offers a solid and valid proposition for property buyers.

As is so often the case, the problems of excessive monetary stimulus have been exacerbated by tightened housing supply, with the number of new homes falling sharply since the mid-2000s despite the booming prices:

Advertisement

This low interest regime has been further exacerbated by the problem of below-average supply in recent years. On average, there have been 18,419 units of new flats available for sale over the last 15 years. However, there were just 14,000 new flats available for sale in 2012. This is also a level below the average turnover of 19,000 a year. Since 2007, we have seen a shortage in some years alongside the rise of property prices.

ANZ believes that Hong Kong housing could be facing a “perfect storm”, as recently introduced macro-prudential measures aimed at cooling housing demand collide with policies aimed at boosting housing supply and, potentially, rising US interest rates:

Over the past 12 months, the government and Hong Kong Monetary Authority (HKMA) have repeatedly heightened the intensity of their demand-side and supply-side measures:

Stamp duties: In October 2012, the Government raised Special Stamp Duties (SSD) by another 5 ppts and introduced a new Buyer’s Stamp Duty (BSD) of 15% on non-permanent Hong Kong residents… In February 2013, it raised the stamp duty. For properties buyers who already own property, the stamp duty for property under HKD2m became 1.5% of the transaction value, compared with HKD100 previously. For all other properties, the rates of stamp duty was doubled, to as high as 8.5%. The government also amended the law on stamp duty, so that it also applied to hotels, commercial properties, car parks and the like, in addition to residential properties.

Mortgage tightening: The HKMA has raised the stress test level for mortgage applications by 300bps for the interest rate increase assumption. In addition, a risk weighting floor of 15% for all residential mortgages is required in computing the capital requirement. Mortgages for car park and commercial properties were also tightened.

Land supply: In the Policy Address, CY Leung said more land would be rezoned for housing and new areas opened up for development, with 67,000 private units expected to come on to the market over the next 3 to 4 years. A target of some 100,000 subsidised public housing units would be built in the five years from 2018, in addition to the 75,000 already planned for the coming five years.

On 28 February 2013, the government announced it will sell 46 residential sites (of which 28 are new sites), expecting to provide about 13,600 flats, nine commercial/business sites which could provide approximately 330,00m2 gross floor area, and one hotel site which could provide 300 hotel rooms. More importantly, the Government has decided to abolish the Application Mechanism from 2013-14 and resume regular land sales. Combining the supply from other sources such as MTR Corporation Ltd (MTRCL) and the Urban Development Authority, total supply of flats could reach 25,800 in FY2013-14…

With the US economy recovering at a faster pace than expected, we believe the low mortgage rate regime may end earlier. A wrong timing of over-supply may risk Hong Kong suffering a ‘perfect storm’ that will potentially result in a significant impact on local real estate and on the overall domestic economy.

Advertisement

The second warning on Hong Kong property comes from Puru Saxena, who runs Puru Saxena Wealth Management, an established money management firm based in Hong Kong. Saxena produces the monthlyMoney Matters report, which follows economic, historical and geo-political trends, and explores investment opportunities in unpopular and distressed markets.

In his March 2011 report, Saxena described the Chinese and Hong Kong housing markets as a “severe and gigantic bubble that is going to end very badly”. At that time,Saxena also noted that China’s housing value to GDP was around 350% of GDP, which was only slightly below the peak value reached by Japanese real estate (370%) just prior to its collapse in 1990, whereas Hong Kong’s housing value to GDP ratio was around 330%, which was above its peak level reached just prior the Asian Financial Crisis in the mid-1990s.

Two years on, and Saxena has repeated his warnings about the Chinese and Hong Kong housing markets, this time noting that “this bubble is even bigger than the bubble we saw in the US”, whilst claiming that home affordability “is off the charts” taking some “13.5 years of income to purchase an apartment here in Hong Kong” and around “25 or 30 years of income” in some Chinese cities. Like the ANZ, Saxena attributes much of the problem to “the Fed’s zero interest-rate policy”, which have been “near zero for almost four years”.

Advertisement

Saxena notes that Hong Kong real estate has a history of boom/bust cycles (a classic symptom of unresponsive supply), which makes a US-style crash inevitable this time around for similar reasons enunciated by the ANZ:

“I think it’s going to be really bad here because if you look Hong Kong, Jim, this is a very volatile market. Between 1980 and now we had two instances where property prices fell by 50-60%. In 1980, property prices topped out and bottomed four years later. That bust saw a 50% reduction in prices. Then, in 1997, prices peaked and they fell by 65% over a period of 4 or 5 years. And, now, we are due for another big fall and if you look at the affordability index that I keep coming back to, in 1980 and 1987, at the previous peaks, the home affordability ratio was also around 12.5-13.5…We are now at 13.5 and, historically, we’ve never been higher; and I don’t care what people say, at the end of the day, what determines the value of an asset on a sustainable basis is affordability; and if people can’t afford to purchase while the government keeps clamping down with various duties and taxes, then, in my view at least, it’s only a matter of time before prices come down. And when interest rates in the U.S. go up, then we will see a big bust in property in Hong Kong.”

Finally, Saxena also sees similar problems ahead for Chinese housing which, if came true, would obviously be bad news for the Australia’s commodity-intensive economy:

Advertisement

“I believe it will be worse [in China], because if you look at the shadow banking system in China and the amount of credit that was unleashed on this relatively small economy—and I mean relatively in comparison to the U.S.—as a percentage of GDP the amount of debt unleashed was massive and much bigger than the debt that was unleashed in the U.S. bubble. So, I know a lot of people here that say the Chinese are very rich and they’ve got cash buyers and everything else, but if you look at the raw data—the Hong Kong monetary authority’s data, which they publish on their site through their semi-annual report—anyone can see that it is a classic debt-fueled asset bubble; because if you look at Hong Kong, for example, over the last three years or so since the Fed started its QE program, outstanding mortgage debt has appreciated by almost 50% in 3.5 years; and that is a mind-boggling number. And if you also look at China, the debt that has been issued by the banks, by all the shadow banking institutions, the numbers are mind-boggling and, to my knowledge at least, you don’t have a soft landing…”

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.