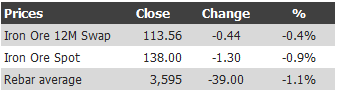

Find below the iron ore price table for Friday April 19, 2013:

Obviously the rebar charts are not signalling a healthy Chinese steel market, at all. Not that that stopped FMG CEO Nev Power from spruiking like mad on the weekend with the help of Alan Kohler:

ALAN KOHLER: And the iron ore spot price hasn’t been falling as much as the other commodities. What sort of average price have you been getting and how do you see that going forward?

NEV POWER: Well our net realised price for the last quarter was $131 a tonne, off an index price of $148 a tonne, which is a very strong price compared to the previous quarter and we see that staying the same going forward, Alan. It’s probably going to trade in that range of $120 to $130 a tonne for the foreseeable future, but we will have some fluctuations around that. And in the short term, I see this sort of price level at $139, $140 a tonne continuing because there are very low iron ore stocks.

ALAN KOHLER: And what’s that view based on?

NEV POWER: Well, steel demand and production is balanced at about 2.1, 2.2 million tonnes per day in China. The steel stocks are relatively high, but they’re not increasing significantly and iron ore stocks are quite low. So, while there is some potential for correction in steel production, I think it would only be minor and supply/demand balance is there in iron ore. So, there aren’t the same factors there that would create any significant drop in the iron ore price.

ALAN KOHLER: You mentioned that iron ore stocks are low. Do you think that the steel mills in China are overproducing at the moment in order to maintain their market share and squeeze out the competition?

NEV POWER: Well I certainly believe that the steel mills, none of them want to lose their position and lose their market share, so I’m sure there’s an element of continuing to produce even while the iron ore stocks are reasonably high. I think the big driver of that is the expectation of increased demand and continued growth in the steel demand market, so I think steel mills are looking for that demand to come through and therefore the steel price’ll increase as a result.

Basically a bunch motherhood statements and fluff questions. How about some questions about what the deluge of new supply will do to the price:

Pretty obvious, no? A simple question like “why do you think iron ore futures are pricing the commodity at $97 in 2016, Mr Power?” would have injected a bit of journalism into the interview.

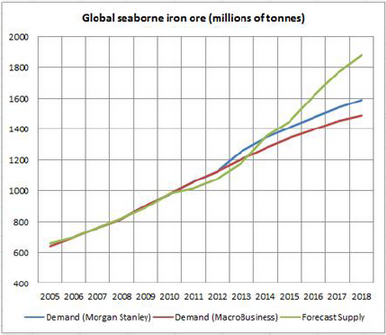

Even taking Kohler’s short term approach this is flaccid stuff. Are the conditions there for a repeat of last year’s crash? Quite possibly, yes. Although Power is right that China’s big port stockpile has been drawn down from 100 million tonnes to around 75 million tonnes today, which would mean any tightening in demand has less local stock to rely upon, it’s not a huge difference and will be more than made up for by the big supply expansions coming on stream in the third and fourth quarter by RIO and FMG.

China is clearly growing more restive about property price growth and there is every chance that it will have to stomp harder still to bring prices to heal, risking exactly the kind of repeat performance we saw last year when they suddenly overdid it. Lurching from overly loose to overly tight is a real risk again.

Doesn’t mean it will happen, and in the long term is irrelevant anyway given the supply issue, but the conditions are there all right. Kohler fail.