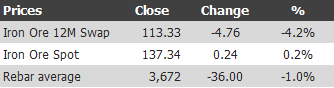

Find below the iron ore price table for April 1, 2013:

Some of these rates of change will be over four days. Nonetheless, news that China is serious about squashing property prices again spooked markets.

One wonders why it’s a surprise that China is stomping on property, but there you have it. From Xinhua over the weekend:

BEIJING, March 30 (Xinhua) — The municipal governments of Chinese capital Beijing and business hub Shanghai on Saturday spelled out detailed rules aimed at cooling the property market following the central government’s fresh regulatory plan earlier this month.

Single adults with a permanent Beijing residence registration, who have not made purchases in the city before, are allowed to buy only one apartment, according to the announcement.

Shanghai said banks will be banned from giving loans to local residents who are buying a third apartment or more, according to a government announcement.

Meanwhile, the two cities will raise down payments for second-home buyers.

The two mega-cities both vow to strictly implement the 20-percent tax on capital gains from property sales.

In fact, a whole raft of mega-cities announced similar measures over the weekend: Chongqing, Guangzhou and Shenzhen also confirmed various iterations of the crackdown.

One more time for the dummies. China is not entering a new cycle of tearaway growth. It is embarking on a stimulus supported shift to consumption led growth. It’s going to slow in the second half and keep slowing further out. The collapse of Indian supply has saved iron ore from already struggling to stay above $100.

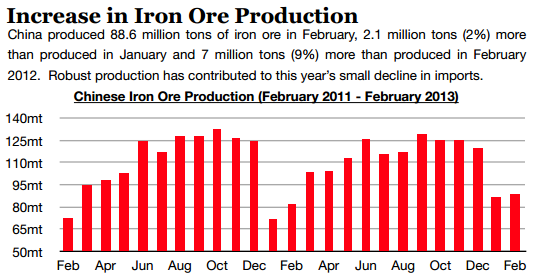

I also received a new iron ore report from “Commodities Research” (who I do not know) which had the following chart of Chinese ore production:

I can’t vouch for its credibility but looks right enough. Note the seasonality factor at work. Recent falls in Chinese iron ore production look largely to be the result of winter weather not price effects. A little more evidence that the $120 price floor theory is bunkum.

Which is something those funding new projects like Gina Reinhart’s Roy Hill might want to consider, which is also in the news:

Roy Hill Holdings revealed it would pay Korean company Samsung C&T $5.9 billion to build the company’s iron ore project in Western Australia’s Pilbara region. Aside from the giant open cut mine, Samsung will build an ore processing plant, a 340-kilometre railway line and port infrastructure at Port Hedland.

Samsung’s involvement increases the Korean influence on Roy Hill, 12.5 per cent owned by Korean steel giant POSCO and 2.5 per cent owned by Korean shipbuilding and trading company STX. Japanese and Chinese companies also hold minority stakes, leaving Ms Rinehart with control over about 70 per cent of the project, which is tipped to cost close to $10 billion.

Anyone funding this project needs to make sure that:

a) it produces at a materially lower cost than FMG, and if the first is true then,

b) they don’t have any loans to FMG.

To be honest, I’m not sure any private capital will be so bold. Which leaves government sources. Export credit agencies in Japan, Korea and China are thought to be already funding up to half the deal. The Samsung appointment looks rather like a part of that.

Hmmm, government-linked export credit agencies from steel-making nations want to fund Roy Hill into a widely expected glut. What does that tell you?