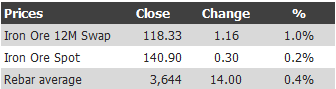

Find below the iron ore price table for APRIL 11, 2013:

In news, from the World Steel Association via Fox, the iron ore glut is official:

Excess supply will arise as 250 million metric tons of new iron-ore capacity is due on stream over the next few years, Edwin Basson, World Steel’s director general, told reporters. The new capacity in iron ore, coming into production at a time of slow growth in global steel markets and which could accentuate current iron ore price volatility, is the subject of “deep” analysis by the association, he said.

“Once you start a mine it’s difficult to stop,” Mr. Basson said.

The association foresees a small oversupply of iron ore this year, a surplus of 100 million tons in 2014 and of about 200 million tons in 2017, Mr. Basson said. However, the world’s major miners “will do what they can” to prevent a market flooding, he said.

The iron-ore market will stabilize after 2017, the World Steel director general said.

Just more than 1 billion tons of iron ore were traded last year on global markets, with China consuming around 70% of the total supplies of the steelmaking ingredient. Most of the new capacity coming on stream is in Australia and Brazil, where companies including Vale SA (VALE), BHP Billiton PLC (BHP) and Rio Tinto PLC (RIO) are investing in mines designed to meet Chinese demand and substitute some older sites where ore qualities have declined. On average, it takes between 5-to-10 years for new iron-ore-mine capacity to be planned, built and start production.

However, growth in China’s steelmaking and in its steel-consumption levels has slowed significantly in recent years, which means its demand for iron ore is also growing more slowly.

“We believe China has reached an inflection point in its economic growth path: it will continue to grow but at a slower rate than in the past,” Mr. Basson said. China’s steel consumption will show annual growth of “2-4% going forward, rather than 7-12% as in the past.”

These figures are much worse than those published by Morgan Stanley and closer to my own view of the timing of new supply.