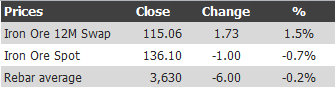

Find below the iron ore price table for April 2, 2013:

To the charts. For spot:

For swaps:

Rebar average:

And rebar futures:

Rumours are that the market is slow ahead of public holidays in China on Thursday and Friday. My guess is that ore will keep bleeding in the short term as Chinese steel prices remain weak.

That’s a guess of course, which is just what we find in the news today in conflicting opinions about the efficacy of Chinese property price curbs. From South China Morning Post comes a dire prediction:

Home sales across mainland cities this month are expected to drop as much as 50 per cent from last month, after local authorities announced detailed measures to cool the property market.

Whether or not there will be an accompanying drop in home prices will depend on how municipal governments implement the measures, according to analysts.

As of the end of last month, mainland cities such as Beijing, Shanghai, Chongqing, Xiamen, Hefei, Tianjin, Guangzhou and Shenzhen had met a central government deadline on issuing detailed property-cooling measures.

Beijing, Shanghai and Chongqing announced tougher measures while other cities’ policies are relatively loose, said Zhang Dawei, research director at property agent Centaline Property Agency’s mainland division.

“No matter whether they unveiled very tough or relatively loose measures, it will hit buying sentiment,” said Zhang. He expects sales transactions to drop as much as 50 per cent from those of last month.

But from Caixin comes a very different tone:

As the property market waited anxiously, over the last weekend in March big cities like Beijing, Shanghai and Shenzhen released implementation details for the central government’s housing curbs.

In March alone, more than 40,000 pre-owned homes were sold in the capital, up 300 percent from February. Meanwhile, average sales prices rose more than 2 percent from February.

Home prices rose 6.05 percent in ten large cities in March compared to the same month last year, a report by China Index Academy shows. Prices have risen five months in a row.

Media reports say the boom in March was because people were worried a 20 percent capital gains tax would be strictly implemented nationwide. Meanwhile, government officials and industry experts have said the tax, which is supposed to be levied on home sellers, would not be passed on to buyers.

Let us assume that the 20 percent tax helped to slow housing prices from rising too fast in some major cities. This would explain why sellers rushed to complete transactions over the last month; they did not want to shoulder a tax burden. Why, then, are buyers not waiting to make purchases?

Some have said that Beijing’s policy putting ownership limits on single adults prompted people to hurry to buy homes. However, there is no evidence that buyers in Beijing in March were single adults. Also, how would rising prices in cities such as Guangzhou and Shenzhen be explained?

I think all of this illustrates that the 20 percent tax will do little to keep home prices from rising. Officials and industry experts insist the capital gains tax will not be passed on to the home buyers, but they cannot explain the increase in transactions and prices in March. The fact is people are worried home prices will jump after the levy is implemented.

I have no idea the truth of the matter and don’t care. What matters and is indisputable is that Chinese authorities are clearly concerned about property prices and appear determined to prevent further rises. For anyone with an horizon beyond their nose this means just one thing: Chinese Feds are not on the long iron ore side.