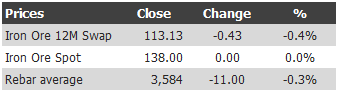

Below find the iron ore price table for April 22, 2103:

A mixed day then but worth noting that the spreads between spot and swap is now at least $10 wider than historic relationships suggest it should be. And the spread to rebar is still at unprecedented levels.

It is perhaps no wonder then that China is ramping up its efforts to overcome price manipulation. From Clyde Russel at Reuters:

Advertisement

The Chinese have launched another attempt to wrest some control of the global iron ore market from the dominant big three miners, but it’s likely this latest salvo will fall short of the target.

Beijing is planning new rules to force importers to use a domestic trading platform for the steel-making ingredient rather than one backed by the miners.

China, which buys about two-thirds of the world’s seaborne iron ore, will refuse to grant new licences to importers unless they use the China Beijing International Mining Exchange (CBMX) platform, according to a Reuters exclusive story .

This physical trading platform operates in competition to the globalORE system, based in Singapore and backed by the top three producers,Brazil‘s Vale, and the Australian pair of Rio Tinto and BHP Billiton. The three are also members of the CBMX platform.

Under new rules, traders and steel mills seeking a new licence to import will now have to trade at least 500,000 tonnes of iron ore on the CBMX, a document on the regulations obtained by Reuters showed. Only Chinese firms are eligible for import licences.

If the Chinese platform can grab most of the volume in the market, it will become the benchmark and squeeze the globalORE system, perhaps forcing it to close.

The benefit to the Chinese would presumably be that a platform under their jurisdiction would be where the global miners were forced to come to trade.

Given the Chinese have in the past expressed concern about the market power of the big three, the view would appear to be that if the miners didn’t control the physical trade then the pricing would be fairer and more transparent.

…The question is whether it will work, and here the answer is more than likely not in the way the Chinese might hope.

Yes, they may well be able to force more transactions onto the CBMX platform, and that in turn may well increase the transparency of pricing, at least for those party to the transactions if not the market as a whole.

But for as long as the big three miners’ output is roughly equal to China’s annual imports, the producers are always going to have the power to reduce supply if they feel prices are too low.

It would also appear that since the iron ore platforms don’t require actual delivery of contracts, the system is open to manipulation by creating “paper” deals that are cancelled before actual shipment.

It’s also likely that the miners will insist on keeping prices tied to existing benchmarks like the Platts index, in which case it could be argued that the platform for executing the trades is irrelevant.

Another key element is confidence in the system, and if any of the parties feel the CBMX platform is being manipulated, they will be extremely reluctant to use it.

This is why the best exchanges and trading systems are ones owned and operated by independent parties whose main interest is ensuring the integrity of the system, as this is the way they attract business.

I, and others, have argued that the best system for iron ore would be a deep and liquid futuresmarkets with deliverable contracts.

Maybe, though that doesn’t prevent gaming in the oil market. I suspect China’s target here is Ruiganglian and CBMIE, the big ore trading houses that the miners hide behind when “managing” volumes at market.

The real answer is a better demand/supply balance, which is coming, in part owing to weak steel demand, which is apparent in the World Steel Association’s new March production report:

Brussels, 22 April 2013 – World crude steel production for the 63 countries reporting to the World Steel Association (worldsteel) was 135 million tonnes (Mt) in March 2013, an increase of 1.0% compared to March 2012.

In the first three months of 2013, Asia produced 259.8 Mt of crude steel, an increase of 6.4% over the first quarter of 2012. The EU produced 41.5 Mt of crude steel in the first quarter of 2013, down by -5.4% compared to the same quarter of 2012. North America’s crude steel production in the first three months of 2013 was 29.7 Mt, a decrease of -5.7% compared to the first quarter of 2012.

China’s crude steel production for March 2013 was 66.3 Mt, up by 6.6% compared to March 2012. Elsewhere in Asia, Japan produced 9.4 Mt of crude steel in March 2013, up by 1.3% compared to the same month last year. In March 2013, South Korea’s crude steel production was 5.7 Mt, down by -7.0% over March 2012.

In the EU, Germany produced 3.8 Mt of crude steel in March 2013, a decrease of -2.2% on March 2012. Italy’s crude steel production was 2.2 Mt, down by -18.4% compared to March 2012. Spain produced 1.3 Mt of crude steel, -2.3% lower than March 2012. France’s crude steel production was 1.3 Mt, a decrease of -9.6% on March 2012.

Turkey’s crude steel production for March 2013 was 3.0 Mt, down by -4.6% compared to March 2012.

The US produced 7.3 Mt of crude steel in March 2013, down by -8.4% on March 2012.

In March 2013, Russia produced 6.0 Mt of crude steel, a decrease of -2.8% compared to the same month last year. Ukraine’s crude steel production for March 2013 was 2.9 Mt, -2.9% less than March 2012.

Brazil produced 2.9 Mt of crude steel production in March 2013, a decrease of -7.6% compared to the same month last year.

The crude steel capacity utilisation ratio for the 63 countries in March 2013 slid to 79.4% from 80.5% in February 2013. Compared to March 2012, it is -2.1 percentage points lower.

So, still good year on year growth in China but nowhere else for a disappointing total.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

exchanges and trading systems are ones owned and operated by independent parties whose main interest is ensuring the integrity of the system, as this is the way they attract business.