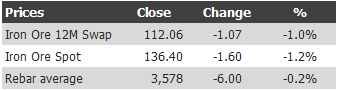

Find below the iron ore price table for April 23, 2013:

Basically the support cast to iron ore prices are signalling further weakness but I wouldn’t conclude yet that a bigger move is on unless swaps breaks to new lows.

Last week’s Chinese port inventory data is also out and was more supportive as it continues to fall gently. And there is no sign yet of a return of Indian sourced supplies.

Meanwhile, Morgan Stanley has slightly upped its numbers for the year:

According to Morgan Stanley analysts Peter Richardson and Joel Crane the price of ore with 62 percent iron content delivered to China may average $128 a tonne in the third quarter, up from $125 a tonne estimated in January. The analysts lowered their price forecast for the final three months of the year to $125 a tonne from $130 and reduced their forecast for 2014 by three percent to $117 a tonne, but kept their prediction for 2013 at $133 a tonne.

According to specialised consultancy services provider Shanghai Steelhome Information, steel reinforcement-bar inventory fell in the week ended April 12 to 9.99 million tonnes, which is the first time it dropped below 10 million tonnes in six weeks. Bloomberg quoted Morgan Stanley analysts as commenting: “The latest steel inventory data suggests that finally optimism about improving demand might be rewarded as both mill and distributor inventories have started declining in absolute terms and in days of consumption for the first time in several months.”

The investment bank has also forecast a delay in the expected global surplus of iron ore initially projected for 2014. While in January Morgan Stanley estimated 3.3 million tonnes of excess iron ore for next year, now the bank expects the seaborne iron ore market to be in deficit of 16.2 million tonnes in 2014. The analysts have also raised their projection for iron ore surplus in 2015 to 49.8 million tonnes from the previous forecast of 40.1 million tonnes. Bloomberg quoted them as saying: “Our assessment of the seaborne market balance and price outlook in the light of the supply side issues and the improved prospects for Chinese demand is that 2013 and 2014 will be years in which the seaborne market remains in deficit.”

OK, so a deficit in 2014 has become a surplus. Goodo. But the actual swing is small, from a four million tonne surplus to 16 million tonne deficit. Not sure why, I don’t see improving prospects for Chinese demand.

As for falling steel inventories, that happens every this time every year and if anything is behind the usual pace, hence tumbling rebar rates.

These changes are cosmetic.